’s Outlook for the Year Ahead

Profiting from Politics, Key Themes & Stock Ideas for 2017

The late-year rally fuelled by the U.S. election has pushed stocks to peaks, which has seen more investors

expressing caution that the market could be primed for a spill to start 2017. While we would be hesitant in broadly buying stocks at the current juncture and would not be surprised to see some consolidation in

markets in the near term, we believe stock markets will once again generate positive returns in 2017.

Key themes for the year ahead include:

- The continued rise of interest rates, and an increase in inflation, with the pace of rate hikes (from

the US Fed) to be watched closely. While rising bond yields/interest rates are usually a negative for

earnings growth and company profitability, we believe this will be offset by stronger global

economic growth in 2017. - Politics featured heavily in 2016, and 2017 will see more of the same. There has been a shift

towards the right in recent times, as populist politics have taken advantage of disgruntled voters.

There are due to be national elections in France and Germany in 2017 which stand out as potential

threats to the future of the Eurozone. - At the same time, US politics will also be on the radar. Details on the timing and scope of planned

policies alluded to by Donald Trump, from infrastructure spending to trade pacts, are likely to be

one of the driving factors which set the tone in financial markets in 2017.

In terms of the local markets, forecast that Australia is set to grow at circa 3% in 2017, helped by a

rebound in the mining sector. We expect New Zealand to keep expanding at a growth rate of approximately 2.5% for the year ahead and expect the key growth driver of Tourism to remain solid.

Overall, we continue to recommend investors hold a “normal” allocation to stocks, although we are

selective in what we own. We discuss below our key portfolio thematic views and stock ideas for 2017 in light of our outlook for the year ahead.

2016 Wrap

2016 kicked off with panic across financial markets, which was then followed by a remarkably calm period. Towards the back-end of 2016 there was heightened uncertainty and volatility in anticipation of the actions of the US Federal Reserve, and the US political election.

Political trends saw knee jerk market reactions to surprise outcomes in the UK as it voted to leave the European Union (“Brexit”), and the election of President Trump in the US.

Despite the volatility, the Australian share market delivered overcame major global

shocks to rise 7% in 2016. Despite a poor start to the year, and massive fluctuations

caused by unprecedented political uncertainty, ASX index put in its best performance

since a 15% gain in 2013.

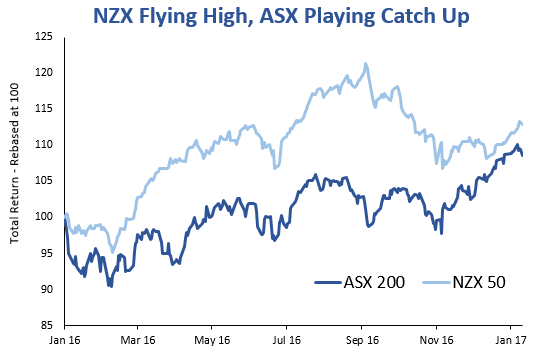

Meanwhile, the NZ benchmark market index ended 9% higher for 2016, breaking a

four-year streak of double-digit gains. The NZ index had rallied by as much as 20.6% in

the year, reaching a record index level of 7571 on September 7, but fell back as rising

global interest rates made NZ yield stocks less attractive.

The late-year rally fuelled by the U.S. election has pushed stock markets to peaks,

which has seen more investors expressing caution that the market could be primed for

a spill to start 2017.

The question looking forward – what does 2017 hold for markets?

2017 Outlook – Big Picture:

Our general view is that markets will generate positive returns once again in 2017,

although we are not overly bullish or bearish.

As such, we recommend investors hold a “normal” allocation to stocks, although we

are very selective in what we own – making sure the stocks we own are supported by

solid investment themes.

While interest rates are expected to continue to rise, growth around the globe is

recovering, and inflation expectations are also picking up.

We expect global economic growth (GDP) to return to around the 3% level, which

should feed into higher company earnings figures. While rising bond yields/interest

rates are usually a negative for earnings growth and company profitability, we believe

this will be offset by stronger economic growth.

As such we see the outlook for shares as remaining sound for 2017. In contrast, the

forecast for bond markets is becoming even bleaker in 2017, in our view.

So far in 2017, markets have been calm, in stark contrast to the start of 2016. However,

given dynamics we expect to play out, as well as the quiet holiday trading period, we

would not be surprised to see a pick-up in volatility as we move through 2017.

2017 Investment Themes

What to watch in 2017:

As mentioned above, we believe interest rates will continue to rise in 2017. It will be

the pace of rate hikes, and inflation measures, which we will be watching closely.

Politics featured heavily in 2016, and 2017 will see more of the same. There has been

a shift towards the right in recent times, as populist politics have taken advantage of

disgruntled voters when it comes to issues like immigration. The key vote to watch will

be in Italy, given the potential for a mix of a banking crisis with political instability.

There are also due to be national elections in France and Germany in 2017 which stand

out as potential threats to the future of the Eurozone.

US politics will also be on the radar. As we have discussed previously, details on the

timing and scope of planned policies from infrastructure spending to trade pacts are

likely to be one of the driving factors which set the tone in financial markets in 2017.

As this news flow is released markets will react positively/negatively and we expect

volatility will likely to remain elevated for some time. So far, Trump provided few

details on policy prescriptions that investors expect will jumpstart growth in the

world’s largest economy, which has disappointed some in the market.

As touched on above, we expect a return of inflation in 2017, particularly given higher

growth rates expected in several parts of the world compared to last year. While we

expect Chinese growth will continue to moderate (to about 6%), the difference will be

made up by the US, in our view. As a caveat, it should be kept in mind that a substantial

portion of US growth is expected to be derived by higher fiscal spend from the new

Trump led Republican government, although as mentioned above details remain

unclear.

Commodity prices have also stopped their fall, and notably the oil price has rallied

strongly over 2016 on plans for a reduction in global output. The recovery in

commodity markets (particularly oil) is also supporting higher inflation levels.

If our inflation forecasts prove correct, this could see interest rate hikes by the US

Federal Reserve positively surprise the market in 2017. The pace of Fed hikes will be

another factor which could drive equity markets over the coming year, and we will be

watching developments closely.

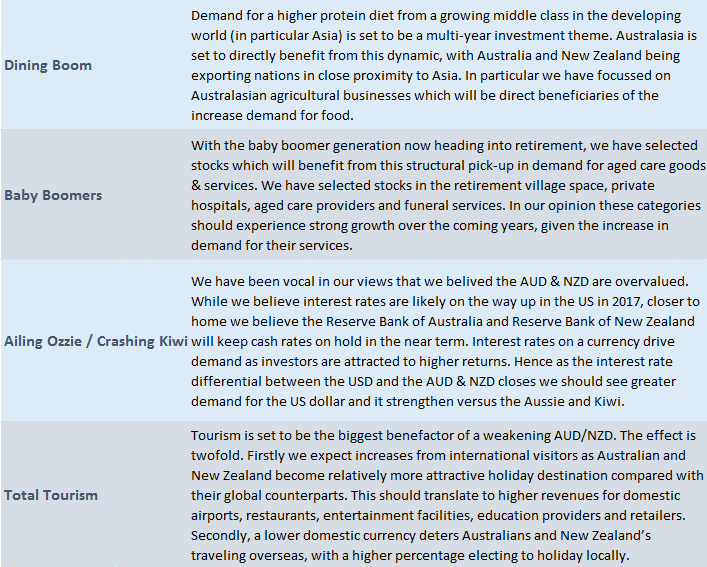

Outlook for Australia & New Zealand

forecast that Australia is set to grow at circa 3% in 2017, helped by a rebound

in the mining sector. While we have noted that commodity prices such as iron ore may

have rallied too far, too fast, the recovery in the mining sector is clearly a positive for the broader economy.

We expect New Zealand to keep expanding at a growth rate of approximately 2.5%

for the year ahead. In 2017 we expect the key driver of Tourism to remain strong,

especially given our forecast for NZD depreciation. At the same time, dairy, NZ’s key

export, has shown prices look to have troughed and are in recovery mode.

Central banks will become less accommodating in both economies in our view, and

believe interest rate easing cycles by the RBA/RBNZ have likely ended.

Australia & New Zealand are largely insulated from politics further abroad, although

one area where the pivot right could have significant implications for investors is

trade.

Trump’s election campaign was filled with anti-globalisation rhetoric, which he has

since softened upon becoming President elect. The key concern would be potential

dismantling of existing agreements, given Australasia’s heavy reliance on trade.

We would note that higher rates across the globe will dampen the “search for yield”

and are likely to weigh on investor demand for high dividend yield paying stocks. Given

the high proportion of “dividend” stocks in the NZ market, we would not be surprised

to see the NZ stock market lag the rest of the world in 2017.

In terms of the majority of our portfolio thematic views we remain comfortable, and

believe the case for several of our portfolio views has strengthened of late. In

particular, the recent US dollar strength and AUD & NZD weakness should help our

offshore earners, while the Tourism sector remains very solid across Australasia

Recap of our existing key Investment Thematics:

New Investment Themes:

Global Reflation and Higher Rates: the global economy already showed momentum

heading into the US election, and the prospect of some of Trumps proposals being

legislated have raised expectations for even faster growth ahead. At the same time

bond yield are on the way up.

A profit Recovery in Australia: we expect profits to rise for the first time in 3 years

across the ASX 200, which usually implies less emphasis will be placed on profit growth

given more companies will be expecting higher growth rates. In this environment, we

would expect cheaply valued stocks to outperform.

Keeping these ideas in mind, we highlight below Australasian stocks which we believe

will benefit from the dynamics discussed above.