Dividend Ideas – Current Portfolio Opportunities

Dividend season is upon us and this means shareholders will be receiving hefty cash payments from their

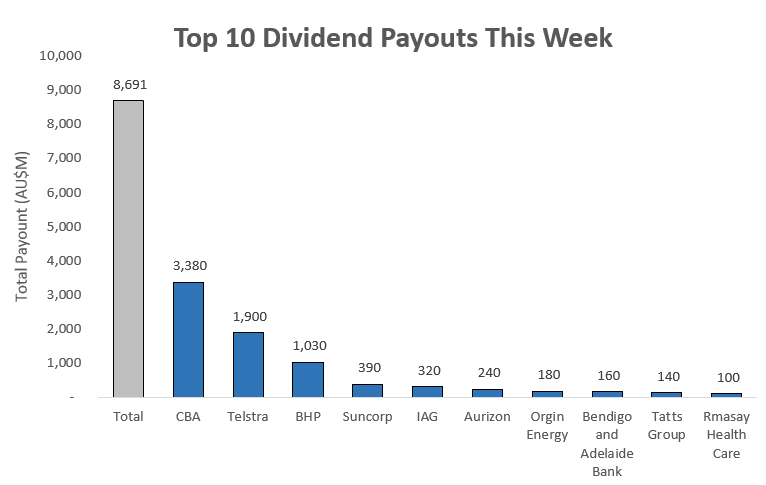

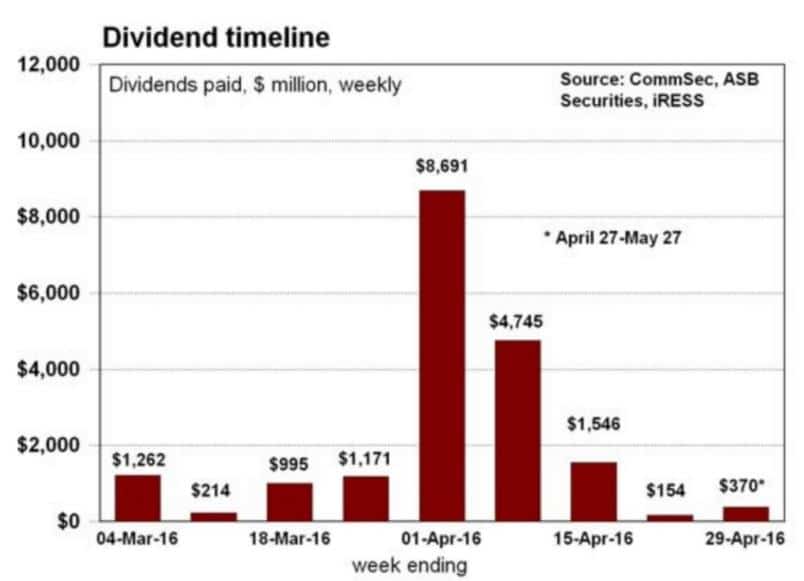

investments over the course of the next month. Almost $9 billion in dividends will be paid to investors this week alone. Australian companies are due to pay out more than $19 billion to shareholders throughout March and April. Much of this cash will end up back in the sharemarket and reviews 5 companies that we think present attractive opportunities for dividends to be put to use. These investments may or may not be in our long term portfolios, but rather they are investment ideas that we think maybe useful for investors looking to put their cash to use over the short to medium term.

ASX Dividend Ideas

The current dividend yield of the ASX 200 is 4.94%, just below the highest levels

recorded since the global financial crisis in 2009. Australian companies are due to pay

out more than $19 billion to shareholders throughout March and April. Below

outlines some investment ideas to put these dividends to use.

Westpac Banking Group (WBC.AX)

- Relatively low risk profile in terms of loan book positioning and low

reliance financial markets income (trading). - Strong dividend yield at 6.3%, consensus P/E of 12x is relatively low

assuming further profits are achieved. - Relatively low risk of dividend cut as a result of strong regulatory

capital position and good organic capital generation capacity. - Appear to be the safest of the big 4 banks

- Mining boom and NZ Diary slowdown remian major concerns

Caltex Australia Limited (CTX.AX)

- Caltex shares have been very weak in recent weeks and may now

provide an opportunity for investors - We believe this is on fear and concerns of weaker refinery margins

- However, Jan/Feb margins averaging US$11.14 a barrel is actually a reasonably solid a relatively soft patch in oil demand at present

- We expect seasonal strength in refiner margins in the near term as

gasoline demand picks up (US driving season) and regional refineries

enter maintenance. - believes there could be strong opportunities for the business to

acquire “cheap” assets as multi-national fuel majors in Australia &

New Zealand seek to exit

Fletcher Building Limited (FBU.NZ, FBU.AX)

- Management remain upbeat on the macroeconomic environment:

- NZ – residential activity to remain strong, commercial construction to

increase, government infrastructure to remain at or above current

levels. - Australia – residential to remain “buoyant” in FY16, with apartments

continuing to drive the market; government infrastructure pipeline

significant but subject to government fiscal position. - Very little growth prospects priced in at current share price. If

Managements core thesis is correct, shares are likely to be materially

undervaluing future growth - In our opinion, the building and construction cycle in New Zealand

should continue to lift further in the three years. - Residential building is booming in New Zealand, with new dwelling

consents hitting their highest point in 12 years - The NZ Government is continuing to free up more land faster through

the Auckland Housing Accord initiative. Auckland dwelling consents

were up 49%

MG Unit Trust – Murray Goulburn (MGC.AX)

- Murray Goulburn is Australia’s largest dairy foods company

- Is a vocal believer in the agricultural boom. We believe demand for food will increase materially in the coming years as population growth outstrips current food supply

- Murray Goulburn is uniquely positioned to participate in the growth of dairy products in Asia, with demand expected to increase 9.7 billion litres by 2020.

- Positively positioned to benefit from a fall in the AUD

- Share price will benefit from a bounce in dairy prices

BHP Billiton Limited (BHP.AX)

- Commodity prices appear to be staging a revovery, both oil and iron ore

- Market appears overly pessimistic over BHP prospects and failing to price the prospect of any recovery in materials space

- As mulit-national miners leave Australia there will be attractive

opporunities for BHP to accuquire “cheap” assets - Already seening large minners cutting production in iron ore, major

positive for BHP - BHP has a strong balance sheet and means it is one of the best

positioned to take advantage of future M&A mining deals