INVESTOR EDUCATION – Nationwide LVR Restrictions

Yesterday the RBNZ released a consultation paper proposing changes to loan-to-value restrictions (LVRs)

and also discussed the possibilities of introducing restrictions on the debt-to-income (DTI) lending ratio for home buyers over the coming months. Despite a number of attempts by both the Reserve Bank and the government to cool the red hot Auckland housing market, the trend has to spread to other parts of the country and the Reserve Bank are now concerned about the financial stability of the economy arising from the current boom in house prices. Accordingly, the Bank feels much more decisive action needs to be taken now in order to avoid a full blown bubble collapse.

Tighter Credit Restrictions to Cool Property Bubble

The Reserve Bank has released a consultation paper proposing changes to loan-to- value restrictions (LVRs) to further mitigate risks to financial stability arising from the current boom in house prices. “The banking system is heavily exposed to the property market with residential mortgages making up 55 percent of banking system assets. Investor lending has been increasing rapidly and is a significant contributing factor to the current market strength. The proposed restrictions recognise the higher risks associated with such lending,” Governor Graeme Wheeler said.

The key changes proposed regarding the LVR rules are:

- Applying a nationwide speed limit for all investor lending, permitting no more than 5% of lending at an LVR greater than 60% (from an LVR of 70% previously confined to the Auckland region). Essentially stopping lending to home buyers that don’t have a 40% deposit.

- Applying a nationwide speed limit for all owner-occupier lending, permitting

no more than 10% of commitments with an LVR of greater than 80% (from an

LVR of 80% previously confined to the Auckland region). So owner occupiers

now require 20% deposit nation wide - All LVR rules that differentiate between lending in Auckland and rest of New

Zealand have been removed. - The new rules are proposed to take effect on 1 September 2016.

- The RBNZ indicated that it will continue to explore additional macro-prudential

measures, including DTI ratios and additional capital overlays. These still

appear to be some months away however

The new LVR policy removes the present distinction between lending in Auckland and

rest of New Zealand. This amounts to a large tightening in credit availability for investor

lending. The RBNZ estimates that the new nationwide investor speed limit could

potentially affect around 70% of investor lending (which has constituted around 35-

36% of all lending in recent months). The new policy also represents a small tightening

for owner-occupiers in the rest of New Zealand where previously up to 15% of lending

could be to high LVR customers (in this case defined as a LVR above 80%).

What is a property investor, how do we define it?

It is largely unclear what the exact definition is. It is loosely defined as: a property is

considered to be an investment property and is not an ‘owner-occupied’ property.

Essentially it encompasses houses that are not lived by the owner, rather it is rented

out for investment purposes.

Does the 40 per cent deposit have to be cash? Or can it be cash/equity or just equity?

It can be either or a combination of the two. The only restrictions is that there is ample

capital available to absorb any loss or fall in house prices. In this way it will help to

cushion bank losses and prevent default when the housing market does correct.

Property market effect

Whilst it is still very early to know the full impact, past LVR restrictions did moderate

house price inflation. The proposed regulation in essence is attempting to cool demand

for housing. It is restricting the availability of capital to those that are speculating on

the continuation of the housing bubble. It still makes allowances for those that buy and

chose to live in their house.

It should deter foreign buyers as they will find it hardest to comply with the new

regulations. Given that they are unlikely to be owner-occupiers, they will now require

40% of the property value as a despite. Consequently, New Zealand property as an

investment class is now relatively less attractive.

Post the RBNZ first restricting LVR’s in October 2013, house prices corrected -5% (AKL

-8%) over a two month period, while 6-month rolling building consents decreased -2%

(AKL -5%). This quickly reversed and three months later both were above pre-

restriction highs. At the time the RBNZ was increasing the OCR.

Cash Rate implications

The new macro prudential tools outlined above should open the way for the RBNZ to

cut the cash rate further in response to low domestic and imported inflation. While segments of the economy remain fairly robust (tourism, immigration, Auckland construction, housing market) the effect of low dairy prices and the threat of global deflation appear to be outweighing the cost of further monetary policy stimulation. We see a 0.25bp cut to the cash rate in August to take the cash rate to 2.00%. From here there remains a district chance of one more cut before the end of the year if the data allows it. Further weakening of key inflation numbers or expectations along

with the level of the NZD on a Trade-Weighted basis (TWI) would be the most

important factors in determining the outcome.

Impact on listed related housing construction stocks – FBU, MPG

There is a positive relationship between house price inflation and residential activity.

Historically when housing inflation has slowed or turned negative activity has slowed

which is ultimately a negative for the housing and construction industry.

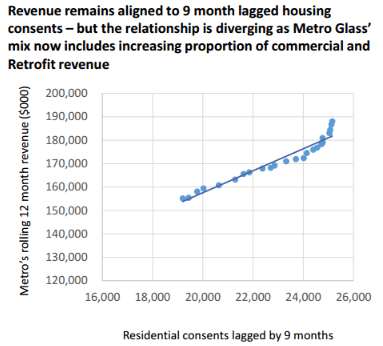

Fletcher’s Building has roughly 49% revenue exposure to residential construction

levels, while Metro Glass revenue performance has a very strong correlation with the

New Zealand housing consent numbers (see chart below). Clearly any material

slowdown in housing construction would lead to a dip in the performance of FBU and

MPG.

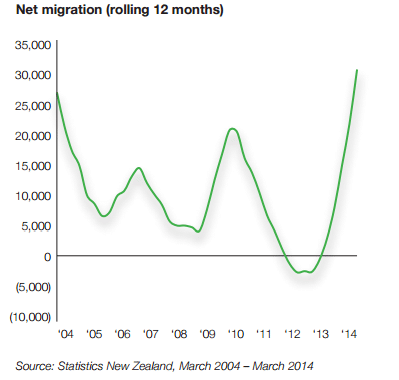

However, due to record high immigration numbers there remains an unsatisfied

demand for additional housing supply. Hence, whilst house prices can moderate we

believe the new housing construction will continue as planned. In Auckland alone, it is

estimated that an additional 25,000 houses are required to meet the medium term

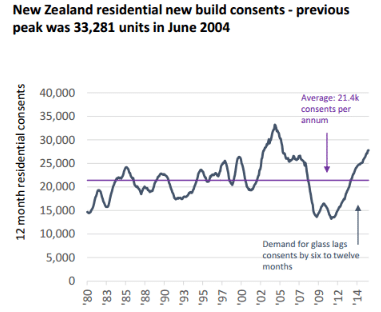

demand. Indicated in the charts above, New Zealand residential housing consents are

nearing the all-time high as developments struggle to keep pace with new demand.

We expect the high level of demand to continue over the medium term.

Furthermore, the government continues to pressure both the housing industry and

local councils to increase total supply in order to address the current shortage. Large

periods of underinvestment and lock up land banks have prevented previous growth.

Consequently, while both FBU and MPG are closely tied to the performance of

house prices, believe they will largely be unaffected by the new LVR resections

as housing construction will continue as planned.