Top 10 Stock Picks in a Covid-19 Recovery

4 April 2020

We are taking the current market volatility as an opportunity to buy quality companies which are trading at more attractive valuations compared to recent history, while remaining cautious on markets generally given the extent of the corona-virus pandemic is still very uncertain.

We think it is time to start “averaging into” stocks (i.e. buying portions of shares, over a set period of time such as 6 months) selectively on a medium term (1 – 3 year) view.

It does appear the market is starting to now differentiate between the stocks and sectors which will face

major problems for an extended period (e.g. retail/ tourism / airlines / property trusts), and those which

are relatively immune and / or benefit e.g. healthcare. We have highlighted the reasons why we think these stocks will perform well once the world gets through corona-virus, and catalysts for stock outperformance. Generally, we have chosen stocks as they:

– Are companies which can continue to make good profit margins.

– Have a solid balance sheet to weather an unprecedented economic shutdown period.

– Stable revenues during the lockdown period and/or low costs so there is manageable cash-burn.

Our top stock list is:

– EBOS

– Pushpay

– BHP Billiton

– Infratil

– Macquarie

– Delegat Wines

– Aristocrat

– Kiwi Property Group

– Auckland Airport

– Woodside Petroleum

Spark & Telstra also were close to making the list, and look like attractive options for investors seeking

dividend income given the defensive nature of both telecommunication businesses during this period.

We are avoiding the most “at risk” industries – and think it is too early to buy the likes of airlines like

Qantas & Air New Zealand, retailers, pure retirement villages, and casinos.

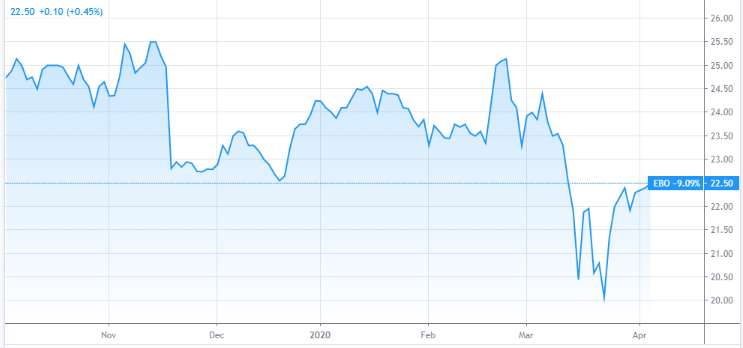

EBOS Group (EBO:NZX / EBO:ASX)

Shares have sold-off in the market wide panic and have regained some ground as a diversified healthcare

business, with limited downside risk, even in a weaker economy. EBOS shares still trade comfortably below its highs of $25.50. Given the nature of EBOS core business we believe there is limited concerns around earnings as part of its business (pharmacy wholesale) is likely to directly benefit from the pandemic.

Illustrating this, Aussie counter-part Sigma reported March year to date volumes were up +80% and

revenues were up +50% from the same corresponding period last year. Australian Pharmaceutical Industries also highlighted demand is up more than +50% from last year for their pharmacy distribution network.

At the current level of ~22x price to earnings looks attractively priced as a defensive healthcare play,

providing a better value and entry point opportunity than our other two healthcare picks (Fisher & Paykel Healthcare and CSL Limited). Overall, we continue to remain positive given our healthcare investment thematic and EBOS’s track record of delivering earnings growth year on year, with a solid balance sheet and adequate headroom of funding to pursue more bolt-on acquisitions over the medium-term.

• EBOS shares have dipped during the covid-19 pandemic and provides an attractive entry point in our view

• EBOS earnings are relatively immune, and the pharmacy part of its business is likely benefiting from the covid-19 pandemic

• We remain positive on EBOS as a diversified defensive holding, backing management’s ability to make further attractive bolt-on acquisitions and deliver solid shareholder return

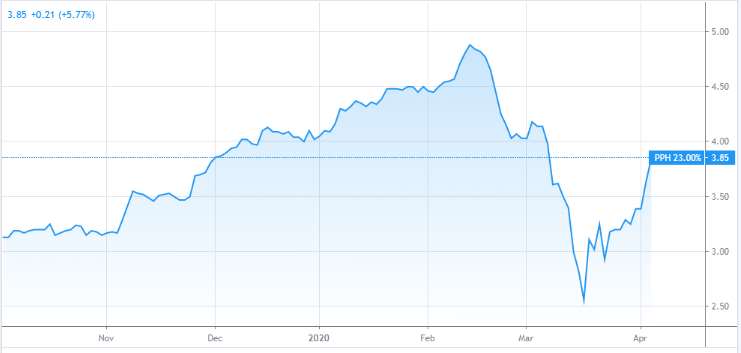

Pushpay (PPH:NZX / PPH:ASX)

shares have fallen -29% from a high of $4.88 in February 2020, as the covid-19 pandemic wreaks havoc

across the market. However, PPH shares have partially recovered after upgrading guidance for the 2020

financial year.

Although a number of organisations are temporarily closing their physical premises in response to the

spread of COVID-19, Pushpay is seeing a shift to digital whereby customers are utilising its mobile first

technology solutions to communicate with their congregations. Arguably PPH is one of the few tech stocks benefitting in some ways from forced social distancing, with revenues likely to be relatively unphased so far by lock downs. It also gives PPH the opportunity to show the value of its product to new and existing customers, as they can use the Pushpay app wherever they are.

While traditionally the middle part of the year is generally slower for PPH, this could see a ramp customer

numbers to deliver a better end of year period. A clear risk however is the large spike in unemployment

levels which could impact people’s ability to donate over the near-term. Given the US government’s massive

stimulus package it should be enough to support modest economic activity and return to reasonable

employment levels by the important fourth quarter.

We continue to maintain our BUY rating on Pushpay, as the underlying business continues to present an attractive investment opportunity – as we move more towards a cashless society with more adoption of digital payments.

• Pushpay revenue and earnings appear to be largely unphased by the lockdown so far

•Pushpay upgraded its guidance as it benefits from increased mobile usage as large social gatherings are cancelled

• Pushpay provides an attractive investment opportunity into the church giving space – with medium to long-term upside potential at the current share price, in our view

BHP Billiton (BHP:ASX)

shares have taken a hit due to the economic slowdown and uncertainty caused by the coronavirus

impacting commodity demand, but have regained some ground as China shows signs of ramping up

economic activity, which has seen iron ore prices rebound. The sector could continue to perform well

underpinned by continual demand from China, whilst BHP’s solid balance sheet can handle near-term risks such as weak demand and pricing shocks.

We believe earnings are should remain relatively robust, with negative sentiment underpinned by record

low oil prices. Oil is arguably unstainable low price levels, and there are signs that the US, Saudi Arabi, and

Russia are moving towards an oil price agreement. Given the diversified and crucial nature of their

commodities and being an efficient low-cost operator, BHP should continue to deliver strong cash flow

within this challenging environment.

The current valuation represents attractive upside potential once the global economy returns back to

normal activity.

• BHP shares are down -25% since Covid-19 was announced in China, and there is upside potential from here once the global returns back to normal activity Forward

• BHP earnings should be supported by revival in economic activity in China creating iron ore demand

• BHP has a solid balance sheet and is a low-cost operator, so should withstand any further pricing shocks and shortfall in demand over the near-term

Technical Summary – The Chart touched the $25 mark from its peak of $42.50 due to the global emotional selloff. Chart also shows $25 will serve as a good support in the near future. We predict more price fluctuations in the coming weeks and Chart depicts $28 as a good entry support point and this will reduce downside risk. Averaging in is going to be a good buying strategy for our investors. $31 will be soft resistance if things move in a positive direction and once broken the stock is going to first test the $33 mark and if touched the stock can go towards the recovery target of $35.30 over the medium

term.

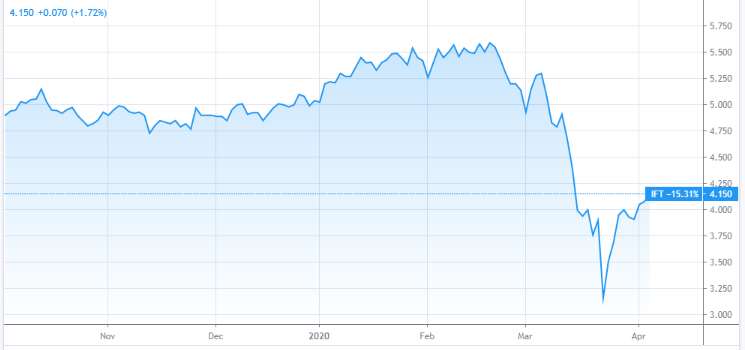

Infratil (IFT:NZX / IFT:ASX)

shares are down -26% from highs reached in February. We believe most of IFT’s defensive businesses should be resilient in a world of covid-19 risks, especially Vodafone NZ, Canberra Data centre, and Tilt Renewables.

However, Wellington International Airport and Retire Australia, are both facing direct risks due to covid-19, with a challenging 2020 expected. Both businesses account for approximately 18% of IFT’s earnings, and some risks appear to be priced into the share price – although there could be upside or downside, depending on how coronavirus spreads. For Wellington Airport we anticipate local domestic travel should return to near normal levels 6-months from now, which should support the airport over the near-term (with less concerns around cash burn like other tourism related exposures). There is a large cloud of uncertainty regarding international travel and tourism – but this could provide upside potential when taking a longer-term view for when travel eventually recovers.

We believe there are strong tailwinds and growth potential for many of IFT’s businesses over the medium-

term – with the Vodafone acquisition boosting overall group earnings and supplementing cashflow in this

challenging period, alleviating balance sheet concerns.

• Most of IFT earnings appears resilient over the near- term cvoid-19 risk

• Wellington Airport and Retire Aus face some covid-19 risk over the medium but they represent -18% of IFT’s business and the near-term risks are priced in

• IFT is our preferred defensive infrastructure given growth opportunity from most of its businesses

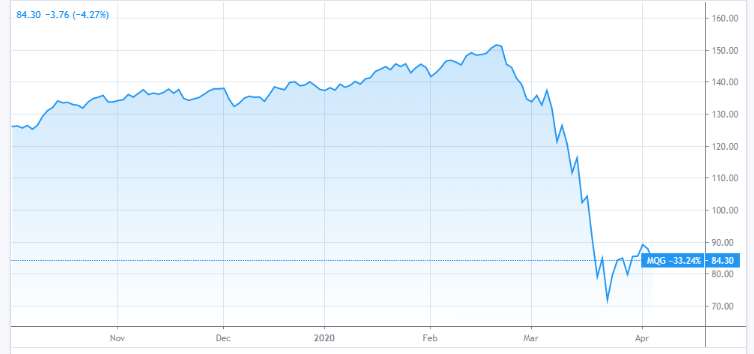

Macquarie (MQG:ASX)

shares are down -44% from its all-time highs reached in February this year, largely due to the economic

uncertainty created by covid-19 pandemic. Unlike the big 4 Aussie banks Macquarie has a more diversified revenue stream, not solely reliant on loans which are under pressure due to lower interest rates with tighter margins.

There is earnings pressure over the near-term, with lower fees from MQG’s annuity style business and

increased impairments. Given high levels of government stimulus we expect economic activity should

rebound to subdued levels. We continue to see Macquarie as a top-quality business which should rebound relatively quickly/early in a recovery given their asset base and maintaining an adequate amount of tier 1 equity.

Macquarie offers a more diversified income stream and we believe Macquarie offers a more attractive

risk/return proposition at its current valuation and better upside potential over the big 4 Aussie Banks

given the current environment.

• Macquarie shares are down -43% in the last 6-weeks

• Economic activity should recover given heavy amounts of government surplus

• Macquarie provides a better risk return proposition compared to the big 4 Aussie banks which may struggle in a lower interest rate environment

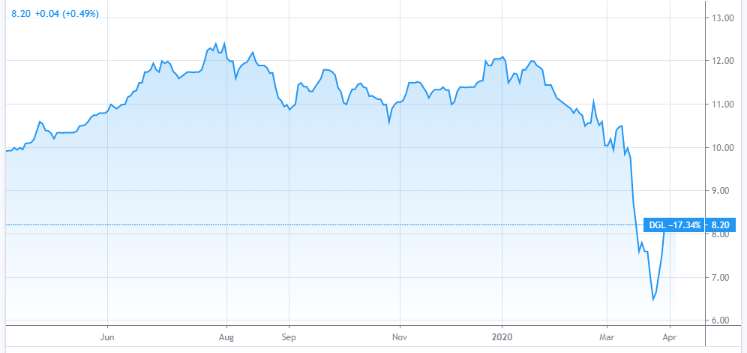

Delegat Group (DGL)

Shares are down -32% from its recent high in December. We believe the covid-19 related lock downs could cause minor sales and distribution disruptions, but given strong demand for their brands in the global market demand should return back to normal relatively quickly. DGL will also benefit from a significantly weaker NZ dollar as is trades below US$0.60.

The wine industry has been cleared to operate as an essential service in New Zealand, and therefore Delegats will not see any distribution or unnecessary cash burn like many other businesses which have been forced to close.

We continue to maintain a solid medium to long-term view on Delegats as it benefits from strong demand for its premium range Wines especially in the US. While covid-19 could have a short-term impact on export sales, it comes at a time when vintage yields are relatively low, making the losses not as significant.

DGL now trades an attractive valuation given it has always traded at a premium due to its solid track record of delivering growth.

• DGL is allowed to operate as an essential service allowing limited disruption to its operations

• DGL appear to be attractively priced when taking a medium to long term view due to strong demand for its premium wine brands

• Covid-19 related risks appear to be temporary for DGL, and will impact them during a year with lower vintage yield

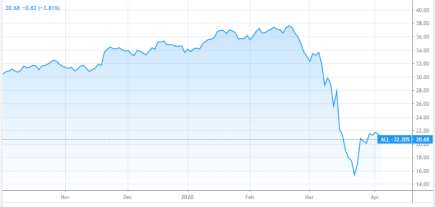

Aristocrat (ALL:ASX)

shares are -45% lower than its all-time high reached in February this year. ALL has been hit hard as a large

component of its revenue comes from gaming machines and is under threat as casino’s around the world

are required to close during covid-19 lockdowns.

While there is near-term risk to Aristocrats major source of revenue and earnings, we believe the market

could be over-playing this as Aristocrat generates just over 40% of its earnings from Digital gaming, which could offset much of negativity priced in over the near-term, in our view. We anticipate public spaces like casinos to open within 4-6 months globally, with local gaming providing most of the support to casinos over the near-term, while there is a large uncertainty as to when international tourism will return and boost casino gaming levels back to more normal levels. In the meantime, ALL have a conservative balance sheet

with significant financial flexibility. Aristocrat provides a better exposure to a casino turnaround as it avoids heavy cash burn over directly investing into casinos (like Crown and SkyCity), due to the nature of its business and cashflow continuing from its digital gaming business.

We believe there is upside potential for investors once public spaces like casinos are open, the question is when this will happen, and due to the uncertainty we would rather buy Aristocrat than a casino.

• Aristocrat slumped -45%, due to covid-19 forcing public places like casinos to close, hurting a major source of their revenue

• Aristocrat provides a better investment play for a rebound in casino activity once the covid-19 pandemic has passed through as it avoids the cash burn risk of casinos

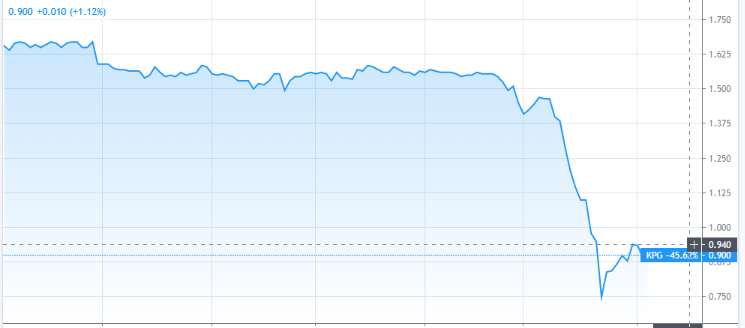

Kiwi Property Group (KPG:NZX)

Shares in one of New Zealand’s largest listed property vehicle Kiwi Property Group (KPG) slumped (down -43% prior to the pandemic) as retailers are one of biggest sectors hit by Covid-19, and there are concerns that landlords would not be in a position to collect rent, given the forced closure of malls.

We believe KPG provides a lower risk indirect exposure to the retail sector, and is trading well below its

previous Net tangible Asset (NTA) per share valuation of $1.43. We believe rental income could be lower

for the current year creating earnings pressure, but this also provides an attractive rebound opportunity.

KPG’s $200m capital raise late last year puts them in a sound financial position, which was used to pay down debt and allow comfortable headroom to proceed with further development at their mixed-use site or even pursue acquisition opportunities, and now provides a buffer during this challenging period. Given the quality of their properties, we believe KPG has a lower risk of experiencing a significant rise in vacancy rate, as retails chains like Kathmandu for example are unlikely to close their store at Sylvia Park given its premium retail location.

• KPG’s offers a lower risk exposure to a retail rebound given their quality assets, sound balance sheet and are less likely to experience heavy cash burn

• KPG provides a rebound opportunity assuming government stimulus package is enough to mitigate a significant rise in unemployment

• Upgrade to High-Risk BUY due to Attractive Valuation

Auckland International Airport (AIA:NZX / AIA:ASX)

Shares have slumped -45% since the covid-19 pandemic as NZ government urged people to stop

unnecessary travel and blocked the borders in an attempt to contain the virus. We believe these measures

restricting foreign visitors could be in place for 6-12 months, or even more. At the same time, we anticipate local domestic travel could return to more normal levels within 6 months.

AIA have a robust balance sheet and given the nature of their business would not experience a heavy cash-burn like Air NZ (or other tourism facing stocks) as total operating expenses are around $190m per annum (Versus Air NZ of $450m per month). We expect to see a significant drop in revenue over the near term, but a return in normal local domestic travel should support the airport, as well as rental income from local businesses for the remainder of the year.

We believe there is significant upside potential available, once we return to more normalised levels of

international tourism, but it is still too early to determine when that could occur. We continue to rate AIA

as an important infrastructure asset with long-term growth, and the current share price represents an

attractive entry point for medium-to long-term investors. While there is some near-term downside risk we

believe it offers a better risk adjusted exposure to a tourism turnaround than an airline such as Air NZ.

• AIA shares are down -45% and appears attractively priced, given their robust balance sheet ability to possibly avoid cash burn from domestic activity over the near-term

• We believe AIA is attractively priced based on a medium to long term view as a key piece of infrastructure

• We believe international tourism could return close to normal levels within a year, which would see significant upside potential

Technical Summary – The stock was at its peak @ $9.88 in August 2019. Technical

Analysis shows that AIA has seen its bottom @ 4.30 and this level should serve as a

strong support for the ongoing volatile period. Chart shows an attractive entry point at

the $4.90 to $5.00 mark. We recommend investors to ‘averaging in to’ stock buying

strategy to manage volatility and price fluctuations. Chart presents a good opportunity

for a short term target (3 to 6 months) @ $6.00 that it has already tested on march

27th and retraced back to $5.00 and found support. Once this resistance level of $6.00

is broken the stock will move onto test the $7.00 mark that depicts a Medium Term

Target (12 – 18 month). If this resistance is also broken then AIA will get into full

recovery mode towards @9.00 target.

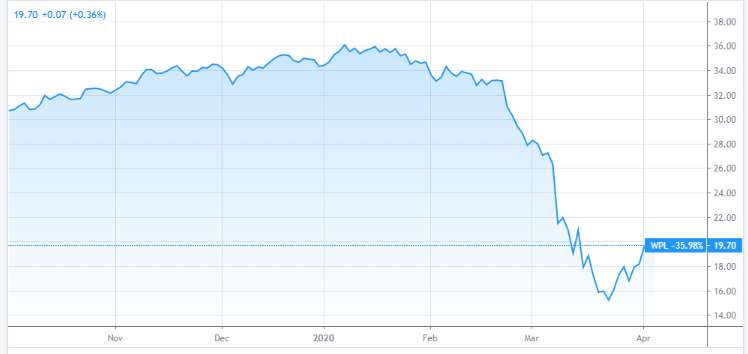

Woodside Petroleum Limited (WPL:ASX)

shares have been under heavy selling pressure, down -45% since the start of the year due to the covid-19

outbreak. China is a major consumer of LNG, as well as heavy crash in oil price seeing it hit 18-year lows. As the world almost shuts down, demand has come down significantly and coupled with the oil price war

sparked by the Russians and Saudi’s it is putting downward pressure on oil prices. We believe these prices

are unsustainable and should rebound once we return to more normal activity.

We continue to rate WPL as our top energy pick due to its low cost operations, with production costs down at around $4.5/per barrel. In response to this challenging situation WPL have hedged ~14% of its expected production volumes for 2020 (above the current prices). WPL has also cut costs significantly, delaying capital expenditure to lower their breakeven requirement, making them the most resilient amongst Aussie peers in a low oil market. They have also spent the last two years strengthening their balance for further capital expenditure, with $4.9 billion cash in hand and $7.9 billion in liquidity, placing them in a comfortable position to weather near-term weakness, and possibly make some attractive acquisitions which may arise.

We don’t expect oil prices to remain at these deflated levels forever and it is promising the President Donald Trump may have negotiated with both Russia and Saudi Arabia to cut output, which has seen oil prices lift recently.

• WPL shares are down -45%

• WPL are a low cost operater with adequate cash and strong balance sheet to weather near-term challenges

• WPL provides significant upside opportunity when oil prices return to more normalised levels as well as benefiting from projected growing demand for LNG over the medium to long term