Global equity markets fell further overnight as the rout across energy and resources stocks continued. The

oil price remains at multi year lows, while yesterday’s weak Chinese trade data did little to inspire the

market.

At The Minute insights

RBNZ preview – To Cut or Not to Cut

Global equity markets fell further overnight as the rout across energy and resources stocks continued. The

oil price remains at multi year lows, while yesterday’s weak Chinese trade data did little to inspire the

market. While we remain cautious on the resource sector generally, we are starting to see value we cannot ignore in shares of mining giant BHP Billiton which was recently added to our Australian model portfolio.

Focussing closer to home, tomorrow is an imperative official cash rate (OCR) interest rate decision for the Reserve Bank of New Zealand (RBNZ). The decision appears to be evenly split between a 0.25% cut to the OCR staying on hold at 2.75%. is in favour of no change to the OCR, although we agree the decision is finally balanced (see factors for and against a rate cut below). In today’s daily we assess the current situation and if the RBNZ are to cut interest rates, the impact of an interest rate cut on the key sectors.

Interest and Mortgage Rates

If there is a 0.25% cut to the cash rate should lead to both lower interest rates on fixed income investments (bonds) and mortgage rates. believes that mortgage banks will pass the full rate cut on to borrowers. This should mean a 0.25% fall in the floating rate and should also lead to a decrease in fixed rate mortgages. believes that the cash rate will stay low for some time and therefore there should be no rush to fix your mortgage at this point.

NZD

A fall in interest rates generally corresponds to a fall in the currency given the change in the interest rate

differential. If the RBNZ does cut interest rates expects the NZD to continue its slide back below 65

cents and towards 60 cents over the longer term. Further, we believe that the US Federal Reserve will

increase its cash rate later this month, adding further pressure on the NZD to weaken versus the USD.

holds a number of stocks in its NZ portfolio at we believe will benefit greatly from further declines in the

currency.

Equities

A lower interest rate is generally good for equity markets, as it provides confidence to the market creates

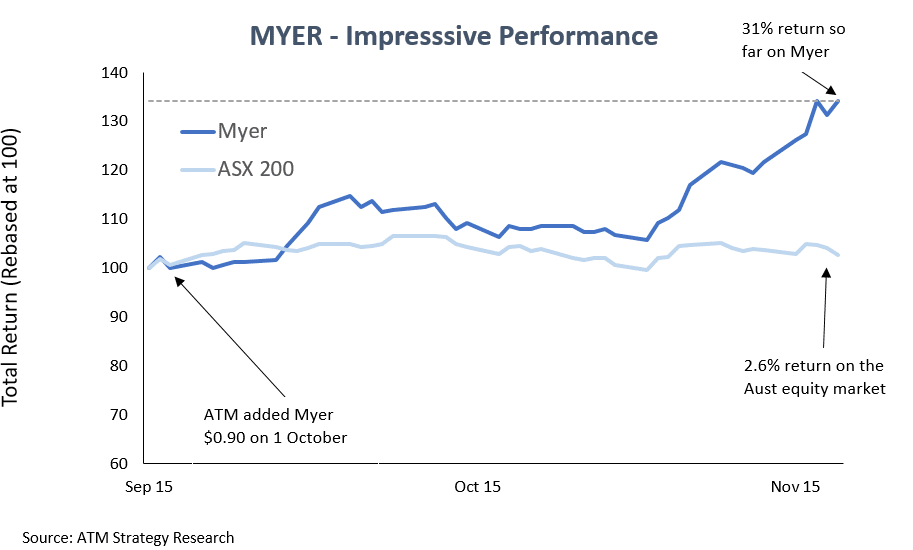

conditions that are generally stimulatory for businesses. Consumer facing stocks, such as Myer (see below)

are also large benefactors of lower interest rates, and we have a number of top retail picks in our

portfolios. Lower rates tends to allow save money on their mortgages and instead spend it on discretionary items. Myer is a solid performer in the portfolio and is returned 31% thus far.

House Prices

Lower mortgage rates should continue to fuel the housing market. Lower interest rates generally means

cheaper mortgage rates and therefore allows home buyers to pay more for property as an investment.

However, feels that the property may have met its equilibrium for now. Prices have been moderating

recently and although structural factors (such as positive migration) support the demand for residential

dwellings, we feel that this is already very much incorporated into the current prices. We are cautious of

aggressively buying property at current prices.

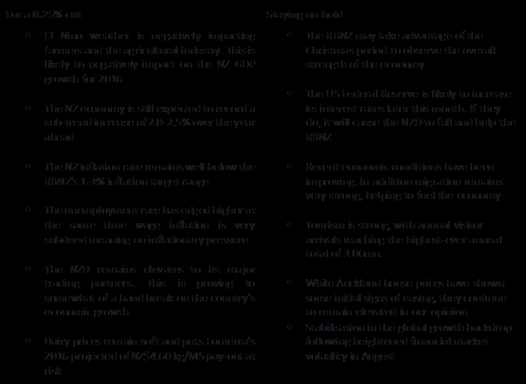

Arguments for & Against a RBNZ rate cut:

Chart of the Moment – RBNZ preview to Fuel Retailers?

A “Spending Spree” is a key thematic of the portfolio Australasian portfolios. Myer is one retailer holds. Since adding it to our portfolio at the start of October, it is up over 30%. It appears that the interest rate cuts from the Reserve Bank are finally starting to take effect on the wider economy. This bodes well for the retail space which should benefit from consumers having more discretionary income from lower interest rates. Christmas is a key time for retailers, and initial indications point to a merry Christmas for retailers this year.

Five Things Markets Will be Watching this Week

1. Whether global markets can follow the US moves on Friday and reverse the sharp sell-off experienced by markets at the end of last week.

2. The Reserve Bank of NZ will make a monetary policy decision on Thursday. While we believe there is likely to be no change to the official cash rate (OCR) this month, and hints of the timing of further rate cuts in 2016 will be looked for.

3. European GDP numbers will be released on Tuesday, and the health of the European economies will be a key factor in determining whether the European Central bank needs to provide further stimulus.

4. The performance of the US dollar this week will be in focus, as to whether it gains strength on the back of a higher likelihood of a hike by the US Fed, in our view.

5. China export and import data is due to be released on Tuesday, and will be watched closely as investors assess the level of slowdown being experienced in China.