BOOM or BUST – Australian Property Under the Spotlight

Bank stocks suffered significant losses yesterday with the major four down between 2.8% to 3.9%. The

financial sector has been one of the worst performing sectors this year as fear of a property market crash

and bank regulation and scandals plague share prices. does not hold any of the major four banks and

are significantly underweight the sector as a whole. We have been deterred from investing in the banking

goliaths for the very reasons they are now selling off.

have been highlighted the risks to the housing market in the past. Particularly in

Australia and New Zealand given the material price appreciation in the past decade.

However we are not as bearish on the sector as many commentators have now

become. Although we believe some price correction is needed by no means do we

believe a full blown collapse is on the way.

House prices are largely determined by a combination of factors but the major five

influences are arguably; household income/unemployment, net migration, domestic

GDP growth, housing stocks (number for houses available on the market) and

availability of financing. In the past, these five factors in combination have been

supportive of house prices rising as the economy bubbled away, backed by the

strength of the mining boom. Since the abrupt decline of commodity prices and the

demand for hard commodities we have experienced a material weakening in the five

factors, but this has not been reflected in house prices to date. We believe that the

housing market may now reflect these fundamental changes.

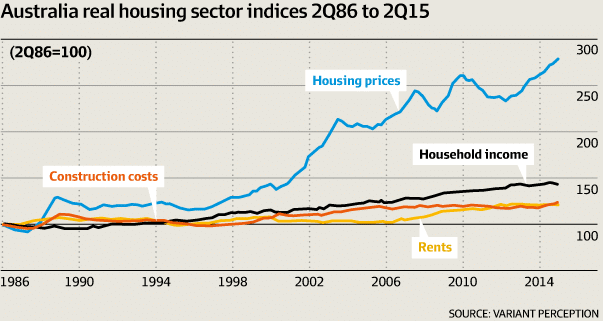

The graph above illustrates the continued rise of house prices while fundamental

factors rose only mildly. Given the recent decline in a number of core factors,

especially household income, we believe that house prices can correct to reflect

these changes. The magnitude of the correction is open for debate, but it would not

be surprising to see a decline in the order of 20-30% over the next 5-10 years if

conditions continue to weaken.

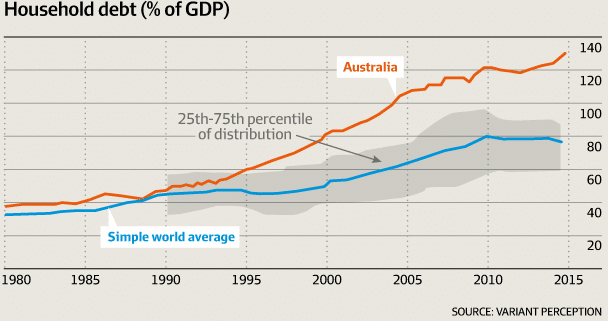

Australian household debt is relatively high compared to the rest of the world on a

%’age of GDP basis (see graph below). This has led to some commentators claiming

that a housing market collapse will eventuate as leverage investor’s panic and sell

their property investments. What has not been accounted for however is

Australian’s vast magnitude of accumulated wealth. Australia as a country, is

reasonably wealthy and has collection of diversified investments which will support

the housing market and can be used to pay down residential debt if need be. Debt

only becomes a problem when the borrower is no longer able to service the interest

or unable to repay the borrowings. In this instance neither is currently the case in our

opinion.

An article published in the AFR yesterday claimed that London based research firm

Variant Perception has labelled the Australian property the biggest housing bubble of

all time. The negative sentiment quickly spread to the sharemarket and banks, a

direct recipient of the health of the housing market.

Predatory leading and falsifying of loan documentations to secure mortgages from

the banks has bought to light the quality of the mortgages made by the banks.

Investors are concerned that many new buyers may not have the ability to repay

their mortgages, especially if the economy continues to slow.

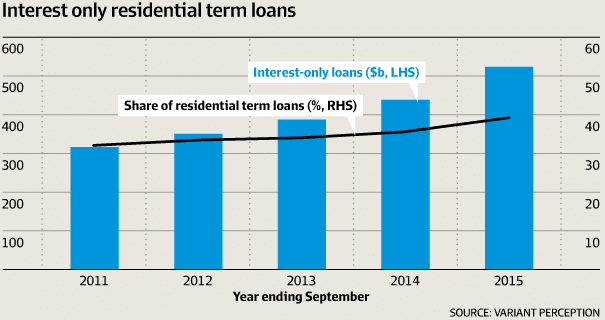

Jonathan Tepper, an economist and founder of Variant Perception, notes that over

the past few years over 40% of all new mortgages originated have been interest-only

mortgages. This can suggest a rather worrying sign that recent housing purchases

have been made on the premises that house prices would continue to rise and in

which case the investor’s equity in the house would increase. With interest only

mortgages, no capital repayment is repaid and they are generally used to capture

rises in prices before investors look to swiftly sell. If these claims are true, this is

rather concerning given the, albeit moderate decline in Australian house prices

recently. The reason being, these fast fickle investors are the ones that are forced to

sell first if house prices do fall. This could spark further price declines as they look to

find the exit.