KLARMAN on buying:

You must buy on the way down. There is far more volume on the way down than on the way back up, and far less competition among buyers. It is almost always better to be too early than too late, but you must be prepared for price markdowns on what you buy.

NZ

Lots to get through this morning. RAK tanked but as of writing order book filled up with buy orders — it’s not over until the fat lady sings. As I wrote to some clients last night corporate doublespeak press releases don’t help — these guys are a classic example of corporates who can’t explain the potential of their best new product (the AI chips) but can issue releases that leave the market scratching their head. On a fundamentals and comp basis RAK is trading at “good” value now, especially compared to peers.

As I keep saying — it ain’t over ‘til it’s over, ye of little faith.

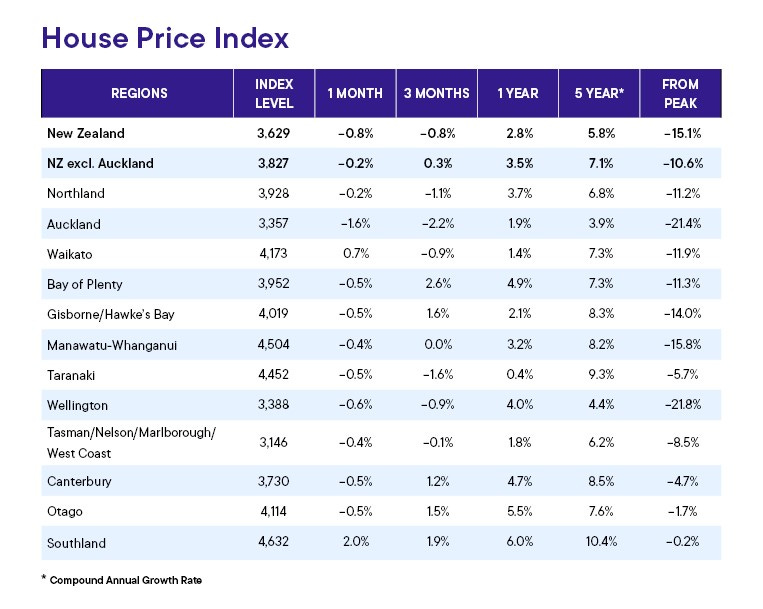

Fletchers — a bad guidance but the more important thing to note is the co cautioning on the housing market … read-through from recent REINZ figures say the same … “safe as houses” not so much … from peak Auckland is down -21.4% now… !

WAREHOUSE — Where shareholders don’t get a bargain?

Great piece by Brian Gaynor Rebecca Stevenson in BD today on The Warehouse’s gnarly adventure in attempting to ape Amazon, TheMarket dot com. You may have come across TheMarket when you were looking for Mighty Ape, or TradeMe, or Amazon. It was essentially an ill-conceived Frankenstein’s monster of a website, with slow shipping an oft-reported complaint by users and a disorientating user interface which is remarkable for offering exactly no impulse purchases (a tinny looking heater? A security camera? Mr. Bezos, we have a problem).

By the numbers — it cost $12mn to set up with total reported capex and outlay of $27mn, and The Warehouse has absorbed about $90mn in operating losses since setting it up. Consider it another way — that’s $117mn of misallocated capital and its associated cash flows. Remember I am a die-hard Munger fundamentalist — the main job of a CEO is capital allocation.

The costs! They keep stacking up – since 2018 the co bought on the corporate stormtroopers McKinsey and spent $75mn in total on restructuring costs — $45mn alone to two evangelical-sounding programmes, “Rise and Agile”. As per Munger —

I’ve never seen a management consultant’s report in my long life that didn’t end with ‘What this situation really needs is more management consulting

So — that’s a total of $192mn in misallocated capital so far. Add to that Torpedo7, which The Warehouse paid $53mn for and sold for $1.00 — so far our misallocated capital total is $245mn. Torpedo7 has racked up about $50mn in operating losses over the years, so adding on that we get $295mn.

Since 2018 The Warehouse has made an accumulated $837.3mn in operating income. If you account for the misallocated capital (i.e. spending on consulting frivolity and fripperies, acquiring businesses that lose money, spending on capex and total losses) and add them to the operating income, shareholders could have made a total $1.132bn in operating income, had capital not been allocated so foolishly.

Accounting for Allocation

TheMarket capital outlay — $27mn

Losses from TheMarket — $90mn

Restructuring, incl. McKinsey – $75mn

Cost of buying Torpedo7 — $53mn

Revenue from selling Torpedo7 — $1.00

Losses from Torpedo7 — $50mn

TOTAL LOSSES (both absorbed losses and capital outlay): $249,999,999.00

At any normal company this would be cause for shareholder outrage. The Warehouse is not a normal company. It is primarily controlled by the Tindall family, via various trusts and so on. The other major shareholder is the Normans, another NZ retailing dynasty. So this misallocated of capital is almost a moot point — CEO Nick Grayston has led The Warehouse throughout this time and he appears to remain on a good wicket. Grayston was previously at Sears Holdings — long time value heads will remember that Sears was taken over by one-time Buffett-worshiper Eddie Lampert and run into the ground via a bizarre Ayn Rand-style leadership philosophy1. Before that he worked for Foot Locker. It’s unclear if Grayston has created value for shareholders based on the facts provided.

There and back again — Warehouse stock price, Net income margin and EBITDA from 2018 – 2024

Foolish ventures can be forgiven when the core business is solid (i.e. Meta — Reality Labs is a cash pit, but the core business of selling ads is great. But the Warehouse’s core “Red Shed” business has lagged peers — you only need to look at the dominance of Kmart in Facebook groups and the cultish devotion it inspires:

Nobody is doing this with The Warehouse. There is no cultish devotion. The Warehouse, to put it bluntly, does not know what it is anymore.

One question I pose is what is Nick Grayston doing in the job? To put it another way — what do the controlling shareholders, the Tindalls and the Normans, see in Grayston and this convoluted “plan” that has resulted in hundreds of millions of dollars of foregone profit? (If either party would like to email me — my email is research at blackbull dot com).

The Warehouse has underperformed peers. Kmart NZ limited reported revenue from customers of $919mn for FY23 (+28%) YoY, and a NPAT margin of 7%. The core Warehouse “Red Shed” operation made $1.8bn with an operating margin (before tax) of 3.8%. This is concerning — the Red Shed business is what made the Tindall fortune that allows him to do all the good work he does (not TheMarket, Torpedo7, or other such distractions).

Anyway — staying well clear of The Warehouse. When I was a smol child I remember going to “red light” specials and buying parallel imported tat and seeing red crates full of CDs for $1.00 and so on. This was the genius of The Warehouse — like TJ Maxx and Walmart, it served as a bastion of a “bargain”. New Zealanders like a bargain. I’m not clear if anybody needs The Warehouse in its current stage.

I am struck by an early NZ Herald interview with Grayston — it notes he ditched the red polo of former CEO Mark Powell in favour of a sleek suit and shiny shoes:

A Nespresso machine sits on his desk next to neatly ordered notes. Written on the whiteboard is the message: “The future is now!”

The future is now, indeed.

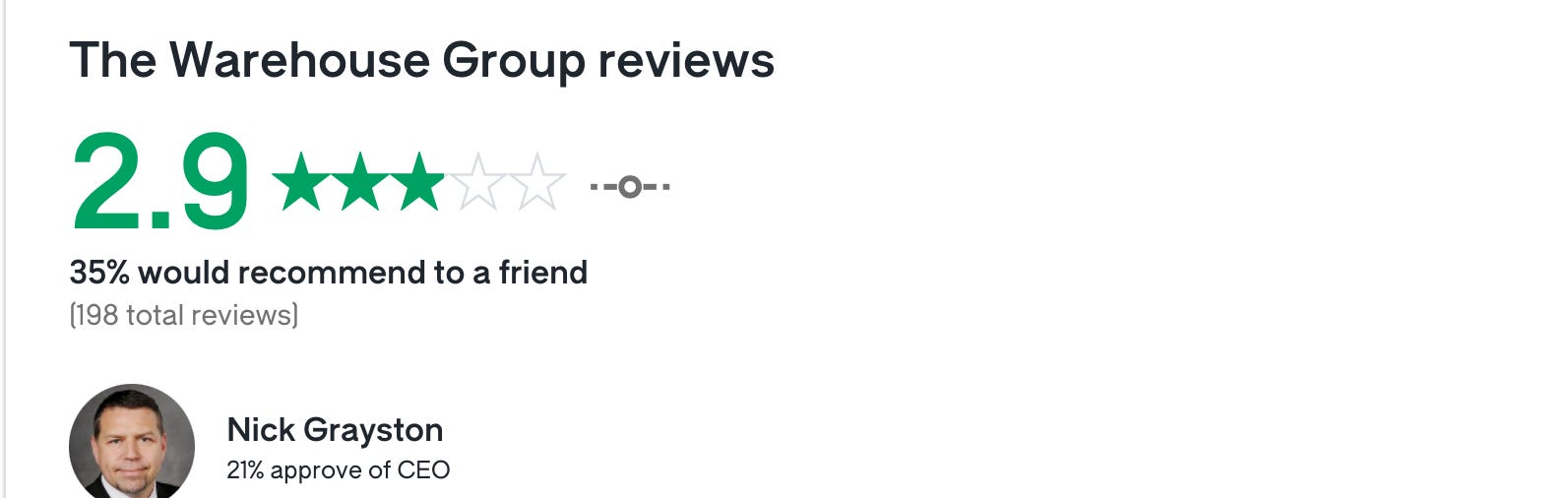

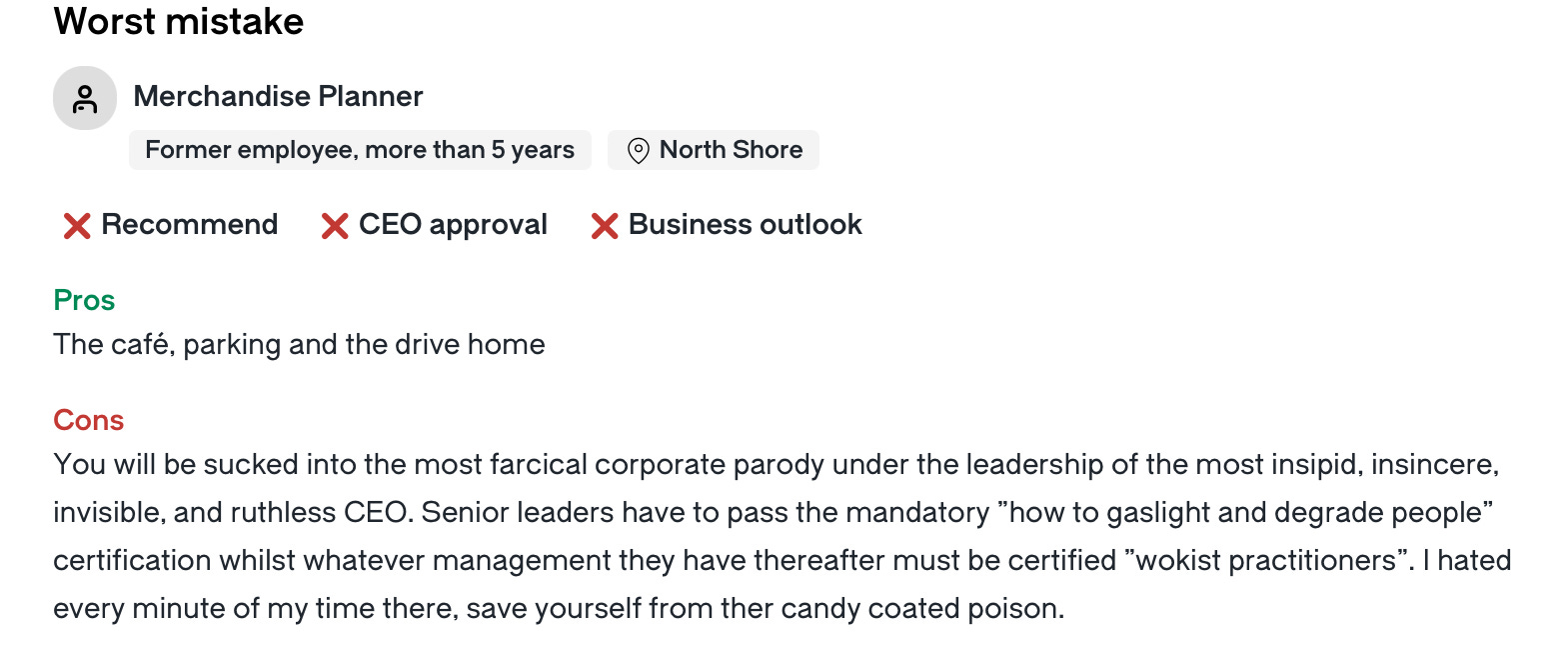

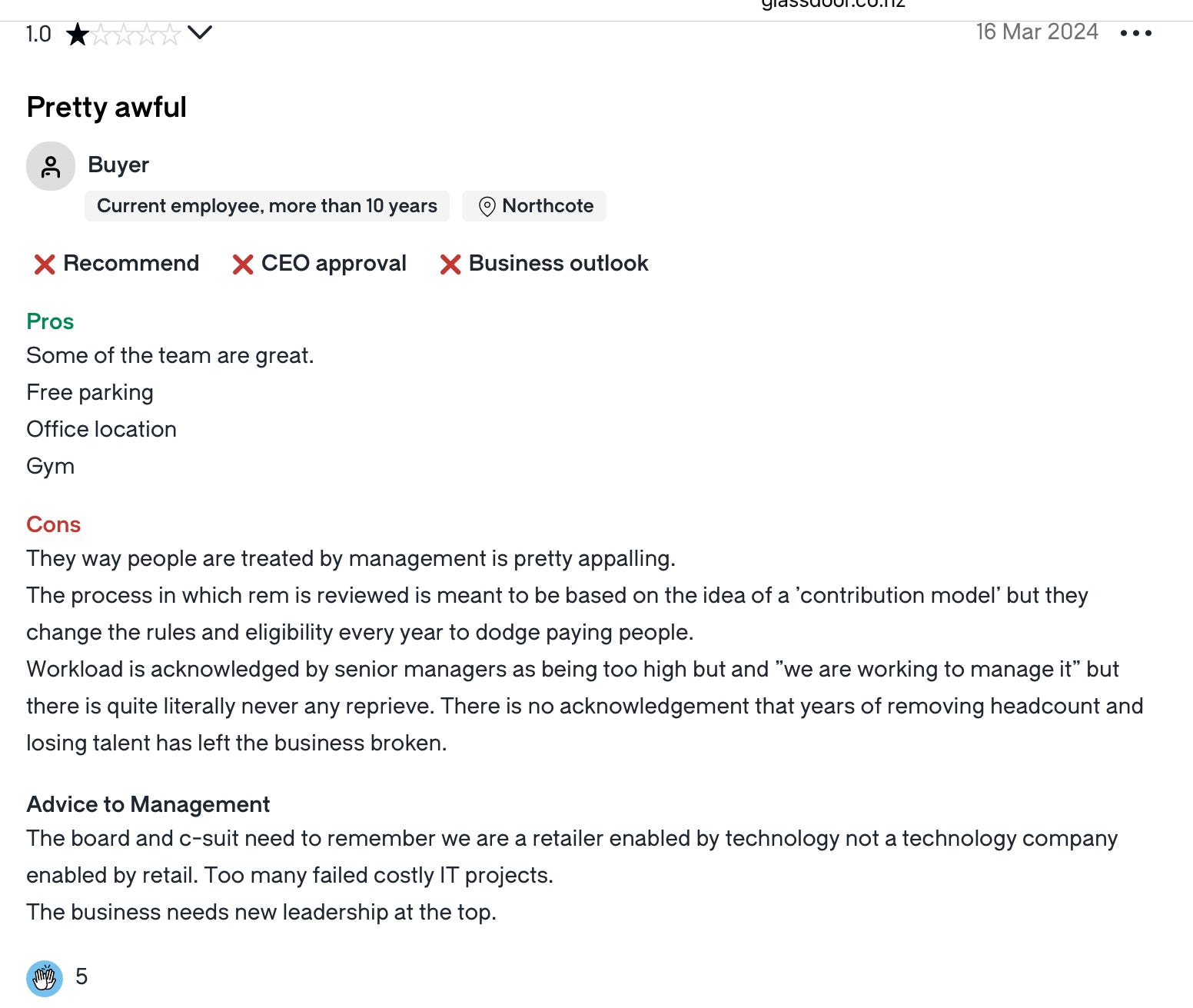

Some recent Glassdoor reviews of The Warehouse

Stuff happens

Kraft might sell its iconic hot dog brand. GameStop is back, baby? “They know about my frustration” — JustLife group CEO on delisting from the NZX. Seth Klarman — The Forgotten Lessons from 2008. The Package King of Miami.

It split its real estate assets into Seritage Growth Properties, which was a popular value trap for some time — the thesis was, Sears had all this real estate; it could lease it out to others and make bank. It’s down +80% all time.