Global markets were lower overnight, with the US market (S&P 500 index) down -0.7%, as investors weighed surging energy prices amid an intensifying debate on whether inflation pressures will be transitory or derail the economic recovery, and look towards an important third-quarter earnings results ahead.

The economic outlook continues to become more uncertain, and Goldman on Monday cut its US economic growth forecast, lowering its 2022 growth estimate to 4% from 4.4% and took its 2021 estimate down a tick from 5.7% down to 5.6%. The firm cited the expiration of fiscal support from Congress and a slower-than-expected recovery in consumer spending, specifically services.

Most sectors were lower, as the US oil benchmark (WTI crude oil) topped $82 a barrel at its session highs, added to looming concerns about inflation. Freight availability and delays also remain an issue for supply chains globally, though prices are starting to show signs of a peak.

This week, major banks will kick off their third-quarter earnings reports, as well as Delta Airlines and Walgreens Boots Alliance. Analysts estimate an earnings growth rate of 27.6% for the US market (S&P 500) in the third quarter, which would be the third-highest growth rate since 2010.

European Markets (Stoxx 600 index +0.05%) were flat overnight, as travel and leisure stocks gave back recent gains which were offset by rise in basic resources.

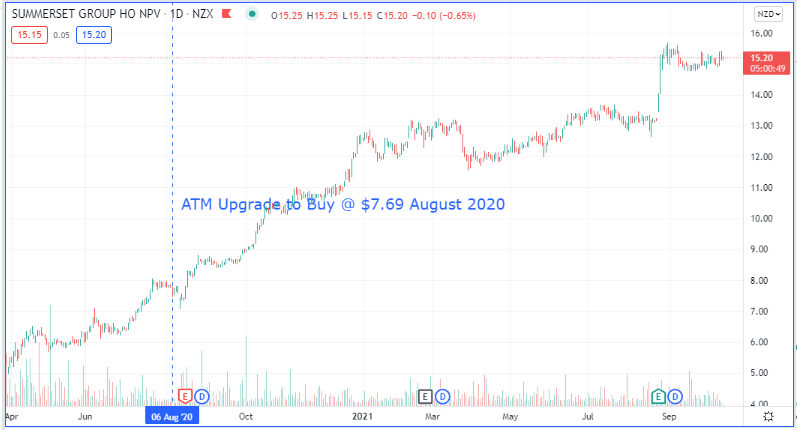

Summerset Group (SUM:NZX / SNZ:ASX)

Retirement village operator Summerset released another solid sales update for the third quarter given lockdown restrictions with 117 new sales and 82 resales – even more impressive is that quarterly sales are up +17% from the same corresponding quarter last year. The number of sales year to date equates to 95% of the full year sales in 2020 – helped by SUM's diversification with its sales footprint across the country, with 83% of sales coming from outside the Auckland region.

We remain BUY rated on Summerset as our favoured large cap NZ retirement village with strong growth potential, while also remaining reasonably priced compared to Ryman even after its recent run.

Australia & New Zealand Market Movers

The Australian market was down yesterday (ASX 200 index -0.3%) following a soft lead from wall Street.

Rising bond yields caused tech shares to lead losses, with most sectors in the red. Star Entertainment shares slumped -22.9% following reports the company has enabled suspected money laundering, foreign interference and organised crime at its casinos.

Commodity stocks made gains with both the Materials and Energy sectors trading higher, as teh iron ore price leapt +5.4% recovering from its recent slump, while oil trades at 7-year highs. The major banks also ended the day marginally higher avoiding the broad based self off.

Ampol shares rose +2.9%, following Z Energy’s board approval of its takeover bid, with shareholder and regulatory approval now required.

The New Zealand market solf-off Monday (NZX 50 index -0.5%) following a weak lead from global markets on Friday.

Understandably Auckland’s lockdown restrictions remained unchanged with daily cases remaining stubbornly high. SkyCity shares were hardest hit falling –4.2% as its key Auckland property remains closed. Other covid-affected stocks including Kathmandu Holdings (-1.9%), Air New Zealand (-1.8%) Auckland International Airport (-1.4%), and Kiwi Property Group (-1.3%) were weaker.

A handful of gentailers were stronger as investors seek security with their profitability not hugely impacted by remaining in level 3.

Z Energy was the best former of the day, up +6.8% after its board of directors endorsed the takeover offer from Ampol which would allow Z Energy to pay out a dividend for the 2022 financial year – effectively sweetening the deal.

3 Things Markets will be Watching this Week

- Key events this week include CPI (inflation) data from the US and China.

- US Third quarter earnings season commences, with the major US Banks set to report this week

- Locally, Employment data in Australia is due and Business Confidence in New Zealand