Fletchers — Where to start? $700mn equity raise — handing out the begging bowl to long-suffering investors on the back of management’s incompetency (and director incompetency). Raising at $2.40 — this looks like a particularly genius and big-brain move when you consider they bought back shares in 2022 at around $5.90 or so.

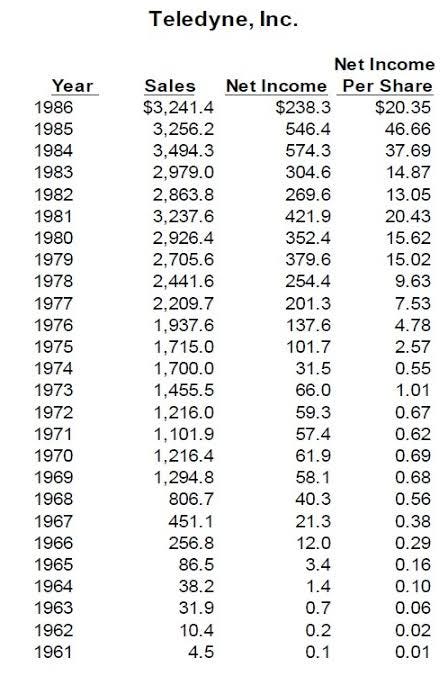

Perhaps Fletchers management took the Wall Street Bets approach — buy high, sell low? You know, if you are a CEO you main job is to allocate capital. You can do this by buying back shares (generally if you think the shares are undervalued). The king of this, by the way, was Harry Singleton, who controlled a company called Teledyne. When he felt the stock was worth more, he issued more shares. When he felt it was undervalued, he moved heaven and earth to buy it back. You can see how this did very well for his fellow shareholders:

Anyway, look — Fletchers did not do this — they allocated capital poorly! They bought stock back when the company was overvalued and now they are hand-in-hat to the street today, offering stock for 50% less than they paid some two years ago! They did not go the Teledyne way!

If you consider that over 20 years they have raised about $3.5bn of equity while returning capital to shareholders of around $4bn — well — the numbers don’t look good, guv (I’m not adjusting for inflation, added debt, etc). In other words, management made the genius decision to give back about $200mn to shareholders per year, while raising an additional $175mn. A toddler (or myself) can do the sums: 200 piles of gold minus 175 piles of gold equals a paltry $25mn per year, for 20 years. This is pretty bad — it gets even worse if you consider the total return (sans those divvys) of Fletchers since 2000 (cast your mind back) is just under 14.00%. In total. That’s not annualised. That’s in total.

If you consider that after ten years, a CEO whose company retains earnings equal to 10% of net worth, will have been responsible for the deployment of more than 60% of all capital at work in the business.

In other words — Fletchers (multiple) CEOs over the years have allocated capital in such a way that buybacks/divvys minus capital raises equals very little, while the stock price has also been underwhelming — to put it politely. The blame should not rest solely on the CEO, though — directors are where the buck stops — the share price of a company, in the long run, is reflective of the failure or success of the directors and management.

I.e Directors who have been on the board for some time — Peter Crowley, acting chair Barbara Chapman and Cathy Quinn — have some responsibility for the sheer value destruction of the company over the years. Their performance at the company, I believe, is adequately measured by the stock’s lackluster performance.

Barbara Chapman is also currently Chair of Genesis and NZME, and serves on the board as a director of BNZ and The NZ Initiative1. I wonder how she gets all her work done! Cathy Quinn is similarly busy — she chairs Tourism Holdings Ltd and sits on the board of Fonterra. Again, I think you can judge for yourself for their relative performance given the respective stock prices of each company.

I got a bit of stick for criticising Ross Taylor earlier on in the Fletchers saga — I make no apologies for this (there’s an “old boys club” in NZ business and well, you can see how well it has worked for Fletcher! Or Fonterra… or, you know, NZ capital markets in general…). It’s all capital allocation, and Taylor wasn’t very good at that, in my opinion. You can see the record in the numbers. There’s no hiding if you are naked when the tide goes out.

Where are the activists?

I have seen a lot of talking heads on LinkedIn decrying the state of Fletchers — poor corporate governance (duh) and so on. But how many of those people (fund managers) have holdings in Fletchers and are going activist on Fletchers? After all, that’s the most effective way to enact change. Earlier this year Simplicity (Sam Stubbs), Myself and the NZSA sent a letter to Fletchers asking for changes at governance level. Some of this was enacted, but I hardly feel it was enough — I have signalled my preference for the company to be broken up before and I stand by that.

A cautionary tale

One thing NZ is good at is useless monopolies. Our supermarkets are virtual monopolies, however they are not very good at being one. Ditto Fletchers — they essentially had a virtual monopoly on many aspects of the market and still failed, basically, to exhibit the characteristics of a powerful monopoly (i.e, high margins, roic, etc). Fletchers is a tale of arrogance and hubris.

Not so Smart (shares)

In brief — SmartShares is rebranding to Smart. I have emailed John and co at the NZX and haven’t heard back yet (here’s hoping) — they also told NBR that the cost is ‘commercially sensitive’. This tells me (and I hope I am wrong) that they have spent a bomb on some genius saying “why don’t we just take off the ‘Shares’ and call it “SMART”. You don’t get Mainfreight rebranding and calling it “MAIN”. It’s just silly. It’s also, from an SEO perspective, kind of dumb? I mean — if you Google “SmartShares” you get a whole lot of options for, unsurprisingly, SmartShares. If you Google “Smart” you get, uh, well, this:

Look, I don’t know anything, but I don’t know if that’s very SMART!

What the Spark?

Spark is a very boring telco. I don’t like them very much, but the other options are just as bad. For a long time Spark was a fine bet — you could put it in a retiree’s portfolio and it would be just fine. It’s Spark! It’s not that interesting, but you know, it ticks along.

Now, they did miss earnings a little. But in the last month, the stock is down around 25% on heavy selling and volume. I don’t think that’s just a few retail shareholders selling their stock in disappointment. It’s a large move. Especially in such a short amount of time for a stock which could regularly be described as “moribund” or “as exciting as a convention for Andre Rieu fans”).

Do we have any theories? research@blackbull.com if you do…

Source post: Blackbull Research - Substack