URNM (Uranium) – from those boffins at G&R:

Hermes once again defied the luxury slowdown, reporting sales growth of +17% for the quarter (you might be going — oh no, not again; another fashion post — don’t worry, we’ll get back to talking about the exciting gentailers and utility companies that NZ market offers tomorrow). For now, Hermes.

A question I get asked often is “why would you want to invest in a handbag company”. The question is always from a man, and I suspect if I said “why is Rolex or ___” so good they wouldn’t question it. I mean, +17% growth is pretty good when you consider rivals like Kering are being smashed by waning consumer tastes. Or +39,000% growth since 1993 — that’s not bad either. The secret sauce that makes Hermes so good couldn’t be simpler, though it is ignored by many companies — share in the wealth created. This is the most important part the the recent press release:

Listen — this is how you do it. St Munger was always saying show me the incentive and I will show you the outcome and I go on (and on) about this because it is one of the few golden truths you can analyse any business with. I spent the weekend reading some of the excellent articles “Finding Compounders” posts on Twitter (sorry, X). Here’s Buffett on Phil Fisher —

Here, here. The multiple Hermes trades for would give you a heart attack — 55x earnings, give or take (you might think it’s a tech company!) But, you know, the company is the best and it has the best management. Why sweat the numbers too much? Here’s a number that’s better — 42% — that’s their 2023 operating profitability. We like numbers like that.

I do wonder if Hermes has reached saturation point. I don’t know the answer. When I say, has Hermes reached saturation point, I am really asking — has the Birkin reached saturation point. It’s everywhere — TikTok; the popular consciousness; Pookie has got hers…and it’s fire…

BECAUSE IT’S SERIOUS, POOKIE.

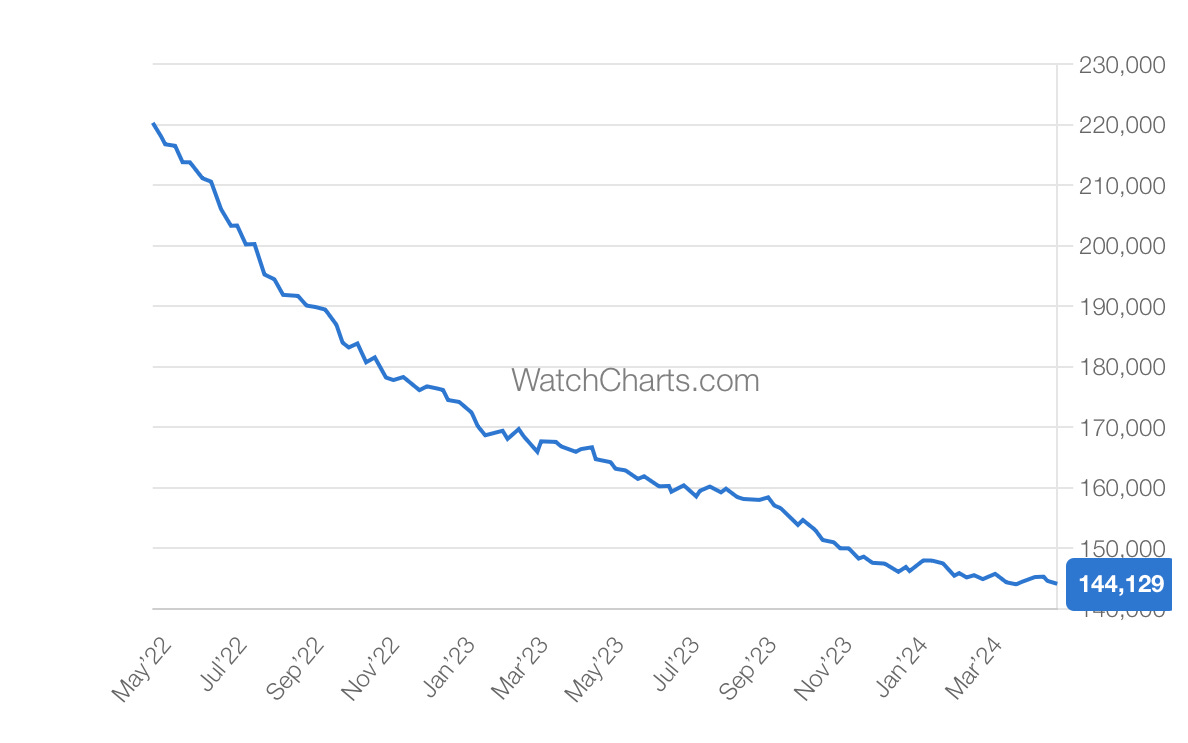

The economics of desire and scarcity are delicate. If something is perceived to be had by everyone, your scarcity value goes down (even if not everyone can get a Birkin). Ubiquity is the enemy. I don’t have any solid numbers of Birkin demand — the indexes that track them are inaccurate and not often updated. What I do know is my TikTok feed is filled to the brim with Birkins. If I go on any half-decent instagram Influencer’s page, they also have a Birkin (maybe it’s fake – idk). My worry is that the ubiquity of the Birkin eventually dilutes it as an object of desire. The same happened with Patek and other watches (Rolexes, APs) — look at the below chart, which charts the “Patek” index:

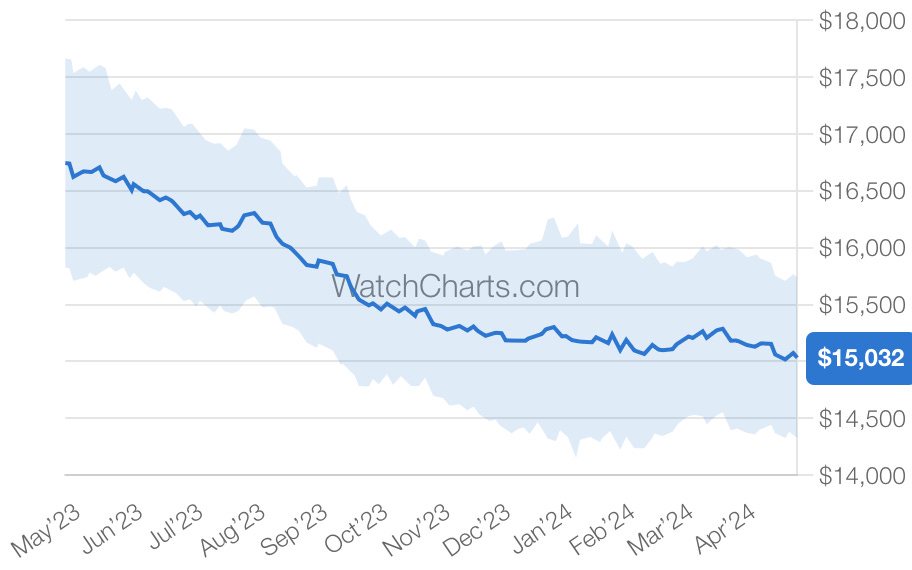

Or, below, the chart for the Rolex Submariner:

Here is my theory of “objects of desire”. I made an extremely professional graph in Canva — you can see why I excel at graphic design:

I mean — this cycle can go on and on forever (it sometimes loops back!). But the question I have here is: are we at peak hype? As Lana says, it’s a question for the culture. Obviously — based on Hermes’ sales — we are not at peak Birkin yet.

I want to talk about my preferred alternative to Hermes: Brunello Cucinelli, which grew revenues by +16.5% for the quarter (about the same as Hermes — not bad). +19.5% growth in America, +16% in Asia, and +13.9% in Europe. Expects +10% growth for the year (I wouldn’t be surprised if they surpassed this). When I was in Paris I discovered a predilection with Brunello, and my scuttlebutt in the stores left me with a favourable impression — high quality but unpretentious (!) customer service, and clients were dropping thousands on everyday basics like jerseys and so on (it’s a recession — but not for the 1%). The goods are high quality and Brunello truly believes in what he preaches — staff are treated incredibly well, fed wine and good food at lunch, and given opportunities to grow in a humanistic sense. Much like Hermes. The company is a lot smaller (€309.1mn in revs for Q1), and it hasn’t yet approached “peak hype”. It doesn’t have a star product with which to do so. It merely has an ethos of good products, good staff, “slow” fashion. In many ways it is a mini-Hermes — with similar values — but much more scope to grow. It’s compounded revenues from 355mn in 2014 to north of 1.13bn last year. It did all this ethically, remarkably (there was a good article in the weekend issue of the AFR about Lush’s founder — he still lives in the same house and has grown the Lush empire into a global giant. Compare this to the implosion of The Body Shop after L’Oreal and then PE’s acquisition of it).

N.b — I don’t think Hermes is going anywhere. I just suspect they will need to find another “star” product past the Birkin (it may not be this year, it may not be in five years — but you can be sure that it will be needed at some point).

We like Brunello. We like Hermes. But I have started to wonder if the Birkin has had its day. Maybe I’m wrong!

Aus + NZ

You will note that Rakon is trading at $1.05. First Sentier in Australia announced it is liquidating some of its funds, including its small cap fund. Maybe (not fin advice — this is speculation!) RAK is trading down (as it has been all week) as part of small cap blowback — (a sinking ship lowers all boats, etc) — no idea if RAK was a holding — or it is trading down because we have heard nada from the board in ages.

Duratec (DUR) is also trading down. It’s more likely than not that DUR is a holding of First Sentier’s that is being sold off (small co, not much liquidity, you gotta take what you can price-wise). Duratec is down +16% in the last five days. This strikes me as very oversold — DUR’s underlying business hasn’t changed. Get in while you can; we all like a bargain.

The problem with Rakon is the board has not released anything — it’s a third of the year since we have heard from them. If the stock closes at 1.03 today that’s a loss of 10.3% in five days (!!) — not sure if this is in the service of shareholders particularly. Under NZX listing and disclosure rules, we assume the NBIO is still ongoing. On the other hand — how on earth are mum and dad shareholders supposed to know anything when the board has said nada? I mean — this is a $252mn (NZD) company. It’s not a multi-billion dollar company. It’s not Google. It’s not Anglo American. It is, maybe, Waiting for Godot1 (or SpongeBob — 140 days later…)

Vladimir: “He didn’t say for sure he’d come.”

Estragon: “And if he doesn’t come?”

Vladimir: “We’ll come back tomorrow.”

Estragon: “And then the day after tomorrow.”

Vladimir: “Possibly.” Estragon: “And so on.”

Vladimir: “The point is—”

Estragon: “Until he comes.”

Vladimir: “You’re merciless.”

Estragon: “We came here yesterday.”

Vladimir: “Ah no, there you’re mistaken.”

Who says I’m not highbrow? This is an intellectual publication, I’ll have you know. We like books and things. We are here for the culture!