NZ

BAI, but I’m pretty sick of this nonsense business now. They own schools, a filing company and a mailing company. Where’s the AI??? I don’t know! Nobody knows! It’s in a trading halt as there is a challenge to the sale of Being Consultancy back to Being AI CEO David McDonald. Look: all my jokes about this are used up, and I don’t know anymore.

Aus

Noting tiny micro-cap whisky-maker Top Shelf International is courting buyers for its business … sad to see, another one bites the dust (following Waterford in liquidation…). Could be a net-net if you’re brave.

Duratec still in the $1.40 zone or so…boring but good (in my opinion, of course)

Ex Farfetch exec Judy Liu joining Treasury Wine Estates — Farfetch, famously, went bust.

Droneshield — Less wars, lower stock. Hype train over.

Another day, Another Mike Ashley Story

Regular readers will recall how Mike Ashley is one of this newsletter’s fixations. He’s the perfect British supervillain. He took Morgan Stanley to court over margin calling him. He took Newcastle United to court over their new kit. He vomited into a fireplace after a meeting with an executive. And, of course, he has running war to buy handbag maker Mulberry, but the controlling shareholders just won’t let him have it! It is a hard life being Mike Ashley.

Now Ashley is taking action against the HMRC for “stonewalling” him over releasing personal tax data. HMRC alleges that Ashley sold multiple properties at an inflated value to special purpose vehicles owned by Sports Direct (an Ashley-owned company) for about £88.6mn. They then wanted Ashley to pay more tax, claiming he underreported the values; they subsequently withdrew the request.

The only reason I find this interesting is because it’s Mike Ashley. No other retailer in the world is perhaps as litigious or outspoken. Just look at this, from the Morgan Stanley lawsuit (later dropped):

Giving evidence on Thursday, Ashley was asked by Morgan Stanley’s barrister, Camilla Bingham KC, whether he agreed with his lawyers in suggesting he was a victim of “snobbery”.

She asked: “Your lawyers suggest that Morgan Stanley maintained the margin call at least in part as a result of snobbery. You don’t believe that.”

Ashley replied: “I do believe that there is an element of that, yes.” Bingham then asked: “So are you a victim?” The businessman said: “I am a victim of Morgan Stanley’s abuse.”

He’s a victim of Morgan Stanley’s abuse! Oh, Mike Ashley!

But…Mulberry…

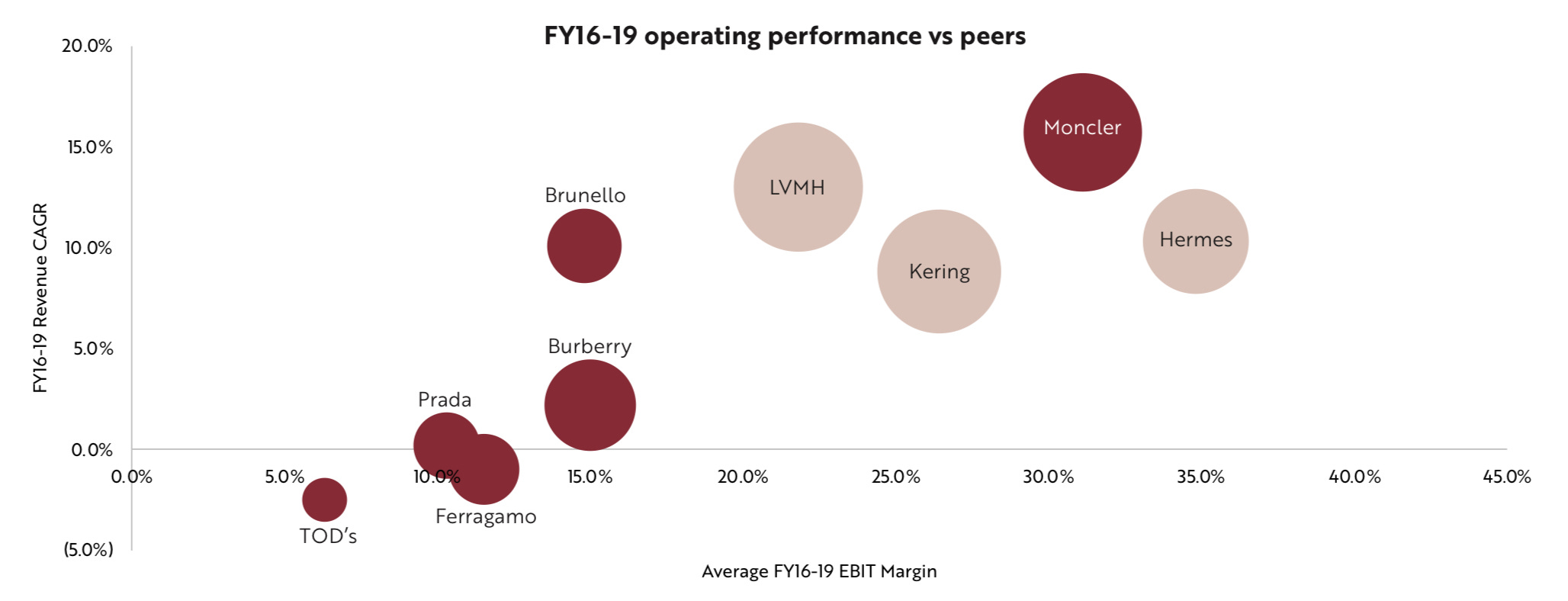

More interestingly, Ashley has offered – repeatedly – to buy Mulberry at a premium. Mgmt & the board are stubborn and a bit silly for not accepting it — FY24 results were down ~19% to 56.1mn quid and the stk price languishes around 101 pence. Ashley offered a premium of 40mn for the company. The company undertook a 10mn cap raise in Sept, which is another case of a company making a single brand trying to go it alone, against a tide of multi-brand efficiency. Single fashion brands rarely work anymore — you just don’t have those economies of scale. See below, from Elevation Capital’s research on Ferragamo — single “houses” tend to have lower margins:

The exception is Hermes, of course. Hermes is sui generis.

Last night I was reading Bloomberg’s wonderful profile of Arnault (in our household, the best work is done by candlelight), and I was struck by the vastness of LVMH’s acquisitions. It’s exponential. Competing with that, whether you are Mulberry, Burberry or Ferragamo, is a hard task.

I don’t think Mulberry is that interesting of a stock — it’s an interesting speccy arb perhaps but emphasis on the “speccy” part. I think Burberry is more compelling — because there’s brand value there on a recognisable and global scale. Likewise, I think single high performing brands like Moncler are compelling, though they trade at a relative premium. With interest rates beginning to fall and patriarchs getting older, I expect fashion M&A activity to increase. As such, I present to you —

The 2025 Fashion M&A Sweepstakes

Burberry — Moncler is said to have mulled a bid for the English house, and could have the cash via new backer Arnault. Odds: 1:5

Pinault at Kering could be looking for a new acquisition (remember how well smaller houses of Kering are doing, like Bottega, versus Gucci). Odds: 1:20

I wouldn’t put it past LVMH taking a look at it (Odds: 1:45) but I expect they’ll be reserving firepower for…

Richemont — We already know Arnault has a personal stake in the company, and that he’s committed “…to supporting [Richemont owner] Rupert’s independence”. More importantly, Richemont has Cartier and Van Cleef — two hard luxury brands Arnault would v much like. I wouldn’t be surprised if brands like Alaia have interest to Arnault, too — it feels in keeping with Loro Piana/Dior. But we’re missing something here — Arnault buys brands, not conglomerates.

Cartier itself commands +10bn eur of revenue. LVMH paid $16bn for Tiffany (roughly a 3.5x revenue multiple). I expect Cartier would sell from a premium above 30bn euro (around half of Richemont’s market cap). LVMH could digest this, but it’s a hefty price to pay. Odds for LVMH buying Cartier: 1:6

Then there’s the question of the “lesser” brands Richemont owns. Conceivable that a player like Puig or Renzo Rosso’s OTB group could pick up some — Dunhill, Chloe, etc. Rupert is getting older; Arnault is not getting any younger, and he has said many times he wants that crown jewel of Cartier. Odds: ???

Finally, let’s not forget about Estée Lauder. It’s at a price (~27bn) where the beauty empire may attract bids (L’Oreal??). Doubtful it gets done, though. Odds: 1:80

Source post: Blackbull Research - Substack