Global markets were lower on Friday, US markets (S&P500, down -2.3%) tumbled lower amid fears of a new variant of COVID (likey to be named "Nu"). European Markets (Stoxx 600 index, down -3.7%) slumped with travel and leisure stocks falling sharply to lead losses as all sectors and major bourses slid sharply into negative territory.

The selloff was broad based resulting in the largest single day fall for the Dow Jones in 2021. Travel and energy stocks were hit hardest over concerns over more restrictions in travel, while bank shares retreated on fears of the slowdown in economic activity and a retracement lower in rates. To put things in context however, the US market is back at end of October levels. On the flip side, investors flocked towards vaccine makers Moderna who’s shares surged +20.6% and Pfizer shares adding +6.1%.

The new variant named omicron, is believed to be more contagious than the delta variant, and scientists fear it could have increased resistance to vaccines, though the WHO said further investigation is needed. In saying that, its is not all bad news as the Nu variant. BioNTech expects the first data from laboratory tests about how it interacts with its vaccine within two weeks. This is long enough to keep markets on edge for now – given markets like certainty rather than uncertainty.

What we do know, however, is that the market has a playbook for new Covid variants, having gone through the beta (first from South Africa), delta (Kent) and gamma (Brazil) variants relatively unscathed. If we follow the same path here, the initial negative reaction may prove to be temporary.

As travel restrictions have already started to be imposed, Travel, Leisure & Hospitality sectors will remain under pressure in the immediate term, with the new variant exacerbating the worries that were already present due to the lockdowns in Europe. We know that the US is very unlikely to impose travel and other kinds of restrictions, at least not to the same degree as Europe and many EMs, so US stocks should outperform.

The longer this persists, we could see the current tightening in monetary policy ease again, which could help tech stocks outperform given their sensitivity to interest rates and given their earnings unphased by lockdowns. Yield plays would likely to benefit such as utilities and real estate. On the other side of the spectrum Financials and Energy stocks will under-perform with lower lower economic activity from restrictions.

How long this sell off will continue remains to be seen, but ample liquidity in the market should result in a supportive “buy the dip” attitude by investors, and we do not foresee a market crash.

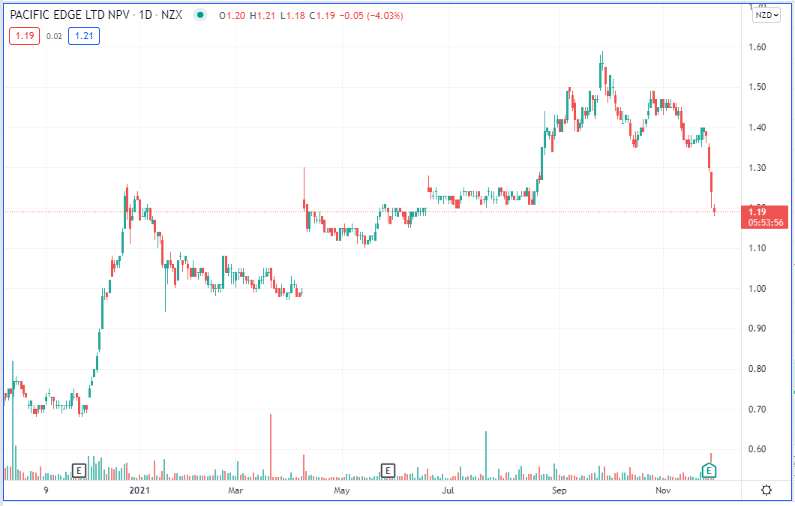

Pacific Edge (PEB:NZX / PEB:ASX)

Pacific Edge shares have been under pressure since reporting their result last week which missed market expectations, while the recent sell-off on Friday has worsened the blow.

For the first half of 2022 PEB experienced softer than expected test throughput resulting in only a +66% increase revenue. With weaker revenue – covid restrictions creating a lingering speedbump to PEB’s growth, and higher expenses to invest in sales growth, shorter sighted investors were disappointed.

We remain BUY rated on PEB, given their strong growth potential and ample funds from the recent capital raise to help accelerate growth. We continue to watch for catalysts in terms of US insurance company uptake.

Australia & New Zealand Market Movers

The Australian market was down on Friday (ASX 200 index -1.3%), with all sectors trading lower.

Like many markets around the world, travel and reopening plays were hardest hit as well as stocks sensitive to general economic activity Financials an Energy leading losses.

Wealth manager AMP fell -4.3% after announcing an increase in impairment charges.

The New Zealand market was down on Friday (NZX 50 index, -1.3%), with almost broad-based selling across the board.

Like overseas NZ travel stocks were weaker but to a lessor degree given tight travel restrictions currently in play. Stride Property Group led the market lower, falling almost 5% after completing a capital raise to reduce debt.

Fisher and Paykel fell -3.5% following their strong result, as investors question their post-covid path.

3 Things Markets will be Watching this Week

- Key events this week US nonfarm payroll, the latest CPI data in the Eurozone and PMI data in China.

- Developments around the Nu variant of covid will be dominating headlines.

- Locally, Australia’s third quarter GPD numbers and ANZ’s latest Business Confidence reading in NZ. Earnings release from Oceania Healthcare and AGM”s from Lynas, Orocobre, Synlait and Premier Investments.