Starting the day thinking about A2 Milk and Synlait — 4% EBITDA upgrade for FY25…was interested to note that English label growth beat Chinese label growth…!

Also, carpet maker Bremworth — settlement of its +$100mn in flood insurance claims is nice, but the board announcing a “strategic review” (code: let’s sell the thing) is better. Noted has had a few approaches. It’s a tiny ~$41mn co (and that’s on the +18% share price surge today), small fish for a bigger co to buy up. I maintain my view that if you threw a dart at most NZ mid caps (and some small caps) you’d find something undervalued and likely to be in the sights of M&A…

Thinking about other results this week — Fletchers, in my view, is now a break-it-up-and-sell-what-you-can type story. Interested in perennial fav EBOS — think the Sigma/Chemist Warehouse contract loss largely priced in, so more interested in how the business is doing in the whole — I always remember that they have a holding in MedAdvisor, the “online pharmacist” which is trading on the ASX at 16c…68% down on the last six months…again, I think a “strategic review” is needed here — the board agrees, as they have indicated they are undertaking this.

Why I like MedAdvisor — the pharmacy industry is still in the dark ages — scripts on paper, having to call up for a repeat, etc. MedAdvisor allows you to order your medications on your phone. Over 3mn Australians use it. There is significant opportunity for growth in other markets (including NZ). This is a speccy stock — no buts or ifs — but strikes me as a niche software product that does one thing well (i.e. the sort of thing Constellation Software loves).

China

Feels a little bit overheated in China right now … note Tencent below.

Great companies, of course, but a wise man once advised me to “trim the rallies”. Food for thought…of course, not as overheated as US tech, but that’s in a class of its own…

Luxury corner

You know my favourite stocks are luxury stocks, and they’ve had a hard last year. Richemont and Moncler were the clear standouts from the most recent season (both grew sales), while Brunello did well too. Obviously, Kering did not do well. Here’s Hermes, which pretty much smashed everyone out of the park:

-

Revenue amounted to €15.2 billion

-

(+15% at constant exchange rates and +13% at current exchange rates)

-

Recurring operating income reached €6.2 billion, representing 40.5% of sales

-

Adjusted free cash flow amounted to €3.8 billion, up by 18%

Can we take a step back and please admire what smashing results those are — that’s a luxury business which does not cut corners operating on a 40.5% margin, with a free cash flow stream that is unheard of for the luxury industry. Let’s also consider that this is during what is nominally a recession.

Worth thinking about what makes Hermes special:

-

A hatred of meetings, corporate hogwash, and the associated.

-

They compete only with themselves — not others.

-

Human values. Hermes objects are made by people and bought by people. Corporate hogwash tends to see people as numbers, and then corporate hogwash forgets about the importance of psychology.

-

A fanatical obsession with product — product is the message.

-

No marketing team.

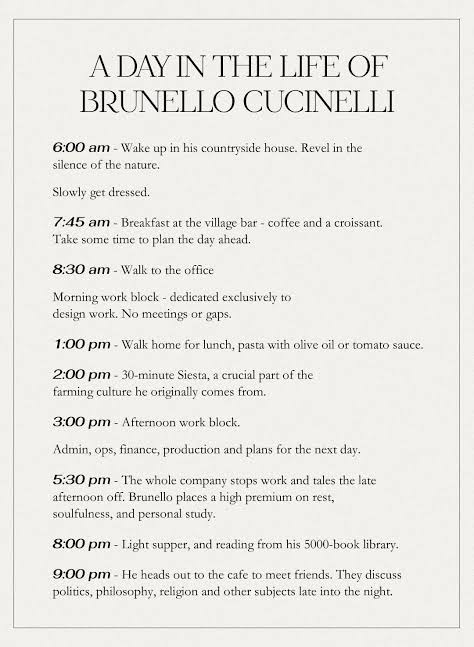

If your product is good enough, and the story you communicate is good enough, the people will come. The same can be said of Brunello, which I have always said is like a “mini-Hermes” — people buy Brunello for quality and the ethos it communicates. Worth re-reading Brunello’s daily routine, which does not look like the nonsense ice bath CEOs who you see on Instagram:

New grandpa Buffett holdings

Noting both Constellation — of Corona beer fame — and Pool Corp. Sold Ulta Beauty which everyone on twitter dot com was going crazy about a while back but always looked like a value trap. Constellation purchase interests me — Corona, Modelo, Fresca… it’s a messy one, because the portfolio encompasses everything from wine to beer to spirits — wine is in a particularly tricky place right now. Like it due to the beer skew (think of Heineken’s results last week) — only 11x earnings — if Buffett sees value, then…?

Source post: Blackbull Research - Substack