Thought for the day — incentives

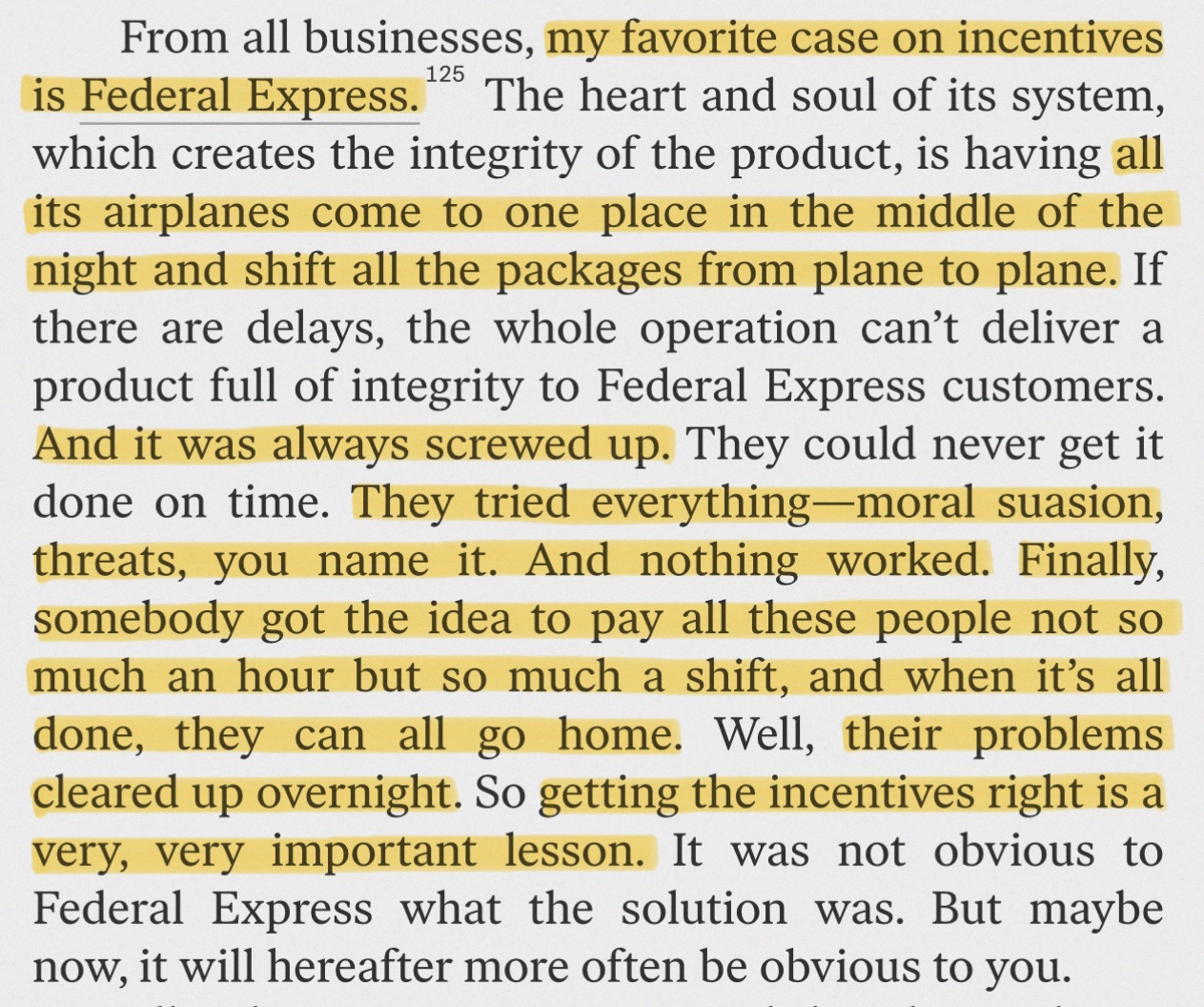

I still can’t get over the death of St. Munger of Assisi (yes, I know he was 991) — re-reading his writings I keep thinking about the power of incentive — the case study from FedEx is a masterclass in the power of incentives. Repeating what I’ve said before about Mainfreight — the incentives are aligned there — the P&L can be seen by all in their cafeterias. I recently also read Ready Fire Aim: The Mainfreight Story (it’s no Proust, but what is?) — here’s some quotes that stuck out to me as what makes a great company and what we try and look for when we invest:

On building culture, and tearing down mediocrity and hierarchy:

‘Plested and Graham preached the three pillars of Mainfreight. A culture built on under-promise and over service as Mainfreight kept on reinventing itself by taking chances and learning from mistakes. A culture based on constantly tearing down any sign of bureaucracy, hierarchy and mediocrity. And the all-empowering philosophy that Mainfreight was there for a hundred years, driven by margin, not revenue.’

On sharing profits with the team (i.e. incentives):

‘At the end of the year there would be a bonus, with ten percent of profits split equally amongst the team. The team, always the team. The remainder of the profits went back into the company for better buildings and carpet and later the lunch room where a canteen lady served storemen and drivers hot meals like their mums made. Meals they ate seated beside the managing director.

On Don Braid’s hatred of ties:

‘Braid’s management approach is reflected in his attitude toward ties, which follows the Don Rowlands path: “I used to be a fan of the tie, an office, a car park, but that just divides us from the others. If you isolate yourself, you may as well sit in that office with your tie and hang yourself with it”.’

Hear, hear. The proof is in the pudding, of course. Look at how MFT has outperformed peers. The culture created at Mainfreight is one that many herald but few adhere to — the ones that actually do always perform better in the long run (i.e. Costco).

I’ve drubbed Fetchers plenty — and so has Stubbs at Simplicity, Lister at Craig’s, etc…only so many times you can flog a dead horse. But the truth is a new CEO is not a solution for Fletchers — they need to instill a new culture — one more like Mainfreight. It’s not impossible, as evidenced by the turnaround at FedEx. It’s all about the long term. If you had the fortune of investing in Amazon in 1997 and having a strong stomach you might’ve had an inkling of where the company was going — quoting from his 1997 letter.

We believe that a fundamental measure of our success will be the shareholder value we create over the long term.

NZ Earnings Continue.

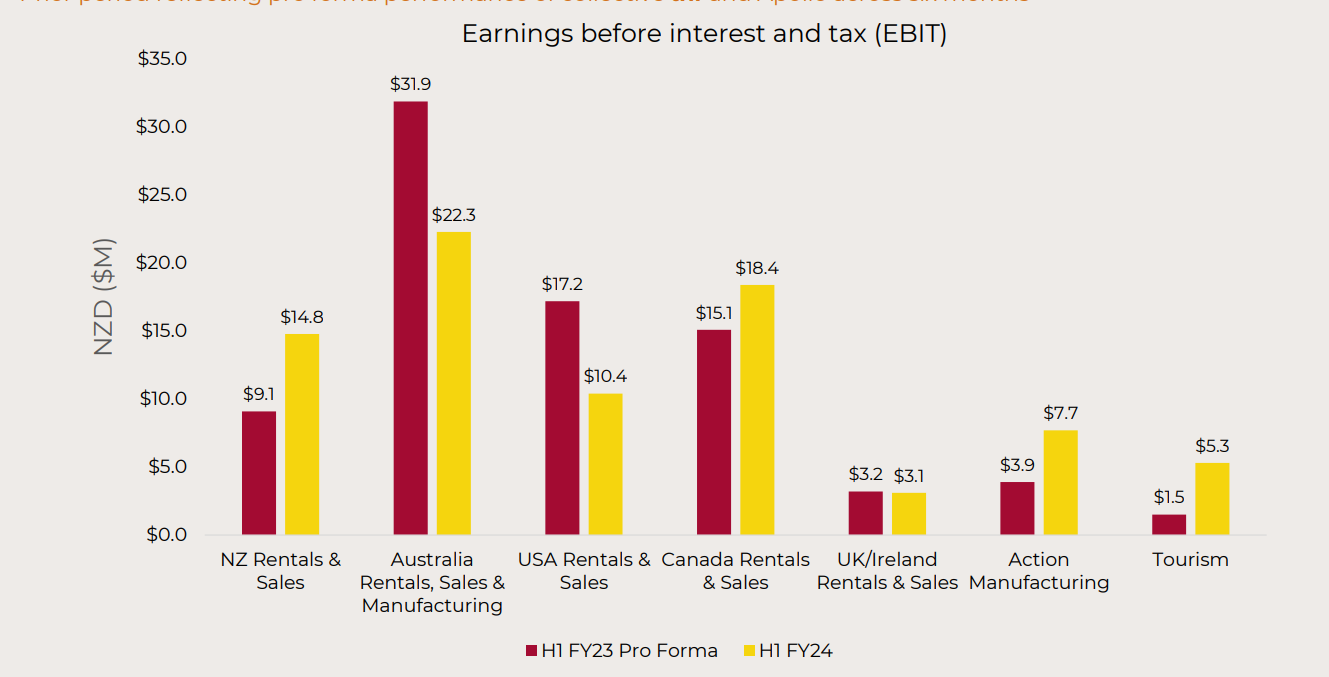

Weaker than expected guidance from THL — selling less vehicles — resulting in higher net debt + interest costs. Selling off after guidance. We continue to like the stock — we think the tourism market has plenty of steam in NZ but think it’s more one to “add to” than to bet your horse on for the year…it’s a two year story. Expecting NPAT for FY24 to be $75mn (previous guidance was ~$77mn). We note strong fleet growth — 7,366 up 15% on the pcp — and the co. reiterating NPAT of $100mn in NPAT for FY26. Average debt cost is 7.2% — doesn’t worry us though we expect vehicle sales market to continue to be weak (look at sales in North American peers, for example). We still like the stock, and note good EBIT growth — esp in NZ. Continue to think the stock is (eventually) deserving of a better multiple than what it currently trades at (~13x)

KMD – “Go woke go broke” — you have to be blind deaf and dumb to not realise how much the “culture wars” and id pol are affecting company results — on all sides of the aisle. You have a boycott pro-Israel companies campaign which has had material impact on blue chips like McDonald’s and Starbucks — and then you have Bud Light, Rip Curl, Disney etc which have been impacted by “anti-wokesters” (personally I think that identity politics is a way to sell newspapers, much like Hearst ran sensational headlines during the Spanish-American war2 (most of you are too young to remember that, but I was there3, on the frontlines).

Anyway — Revenues for 1H24 are now expected to be $469m, down 14.5% on pcp, and underlying EBITDA down a whopping 67% on the pcp. “Go woke go broke” indeed. No view — we don’t like retail and especially don’t like low-margin high street retail.

I don’t think the problem is entirely with “woke”, though — KMD is a company filled with mediocre brands (Kathmandu, Ripcurl, etc) and seemingly no strategy in place. Who, exactly, is buying Ripcurl?? Woke or no woke — obviously not many (if any).

KMD’s rollercoaster ride to the bottom — it’s a long way to the top if you wanna rock n’ roll

FRW — 1H Group EBITDA $119.5mn but weak Big Chill result (-6%) and weaker cash flow — $58.3mn vs $79.8mn. Given our above love letter to MFT we think it is obvious what we prefer — MFT all the way.

AOF — We are noticing the company hasn’t reported when results will be announced, nor have they given guidance — bad result on the horizon or an NBIO as we floated a while ago?? (this is not financial advice, but we do think the lack of guidance is odd). Co. trading down -5.56% today on very light volume as per.

Across the ditch

ANZ — My only Sun(shine) – just won its bid to overturn the regulator’s judgement on its proposed $4.9bn takeover of Suncorp. Should boost ANZ – another $67bn in loans to eat up. Yum! Preferences remain JPM and MQG.

Speaking of MQG — “don’t worry, darling” — their “Fresh face” of 2024 — link. The fairly unknown Verena Lim.

Born in South Korea, her family moved to Sydney. Lim went to Sydney Girls High and started in Macquarie’s Sydney HQ as an intern in 2004, while still studying commerce and law at the University of New South Wales. She moved to Singapore with Macquarie soon after and has worked on Macquarie’s Asian infrastructure deals and investments ever since.

She explained her job as part funds management, part management-management. Her day job is overseeing Asian infrastructure investments and the team that makes them, including red-hot data centres group AirTrunk, in Macquarie Asset Management.

Everybody has been worrying about rainmaker Nick O’Kane — MQG is a bigger machine than O’Kane and we don’t see any reason to worry.

Landlease — Has seen an awful run — down 48% over two years. NPAT for HY pcp was down 42% — a long, long way below the $210mn analysts expected. Guiding for a 7% return on equity. MD of Allan Gray (they own a bunch of Fletchers and Landlease) said

“I’m sure the second half will be better than the first half,” Mr Mawhinney said. “It’ll be hard for it to be worse.”

‘Struth.

Climb Every Paramout-tain

Good piece on Bloomie about the trials and tribulations of Shari Redstone’s Paramount. Paramount was always built to be an acquirer – not a seller — and this is the issue. Sumner Redstone was a builder — from cinemas that have very little value to them Viacom, Paramount, etc. The trouble is Shari is a seller. And the only thing anyone really wants (David Ellison) is Paramount, the studio. There’s a case that maybe Shari won’t sell anything because of the convoluted structure. National Amusements has debt + voting rights + a lot of ailing cinemas. Paramount is a grab-bag of good assets but also has a lot of debt. Best case now — gut feeling — is Ellison buys just the studio (Paramount) and stockholders are issued a special divvy. It’s all a bit of a mess due to the structuring of the controlling co. (NA).

Buffett sold out about a third, which has put more question marks over the entire thing — is it time to get out when the going’s good? Honestly, I don’t know: there’s a good collection of assets there (Yellowstone! Top Gun!) but how do you extract those without triggering debt covenants, etc, etc. It’s up to Byron Trott to work that one out. Paramount is quickly starting to look like a night on bald (Para)mountain…

No way, José

The trainwreck that has been Farfetch finally saw the departure of once-visionary José Neves. His departing note? “I will be celebrating every success that Farfetch achieves for many years to come!” Yeah, yeah…

Leaves the acquirer, Coupang, with a kind of shell of a company — what will they do with it? As we noted before, Kering’s brands have already exited the platform…what exactly did Coupang buy? Data?

I got 99 problems but…

https://www.history.com/news/spanish-american-war-yellow-journalism-hearst-pulitzer

I was there when Captain Beefheart started up his first band.

I told him, “Don’t do it that way. You’ll never make a dime.”

I was there.

I was the first guy playing Daft Punk to the rock kids.

I played it at CBGB’s.

Everybody thought I was crazy.

We all know.

I was there.