New Zealand

The New Zealand market (NZX50, +0.3%) fell yesterday as the 50-point hike by RBNZ caught most of the market off-guard, given the RBA’s decision to hold rates flat.

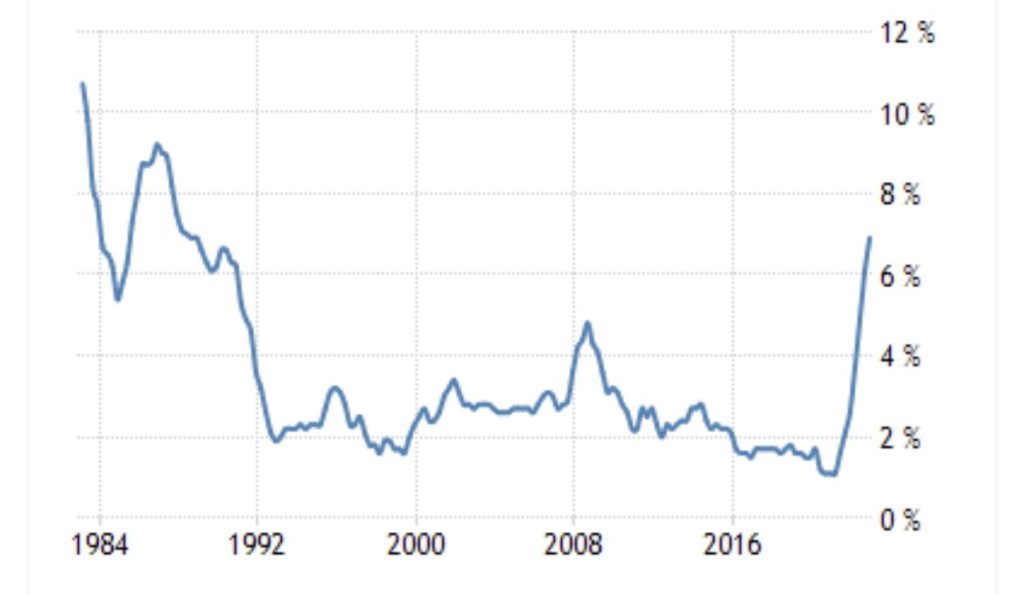

The 50 point hike brings the OCR to 5.25%, the highest since December 2008. It was the 11th straight hike (totalling 5.00% increase since October 2021), defying market expectations of a 25bps increase as consumer inflation remained persistently high and employment beyond its maximum sustainable level. The central bank noted economic activity over the fourth quarter of 2022 was lower than anticipated, but demand continues to outpace supply capacity, particularly following the recent weather events. Going forward, the RBNZ is expecting to see a continued easing in domestic demand and a slowdown in core inflation and inflation expectations. The extent of this moderation will determine the direction of future monetary policy. Gut feel is it looking like one more 25-point hike in May, then a pause for the remainder of 2023 – we remain defensive till we see the full effect of all these rate hikes pay out, most likely in the second half of this year.

Australia

The Australian market (ASX200, +0.02%) was a touch higher to mark its 8th consecutive day in the green. Communications and tech were the best performing sectors, while materials and energy gave back recent gains. Slow news day. It’s worth comparing the divergent policies of the RBNZ and RBA – with Australian inflation sitting close to 7% their pausing of interest rates feels like a risky move with inflation still so entrenched. A tale of two cities — the RBNZ a little too agressive in our view and the RBA a little too blasé.

US

Little to report for the US — the S&P fell 0.25% — mostly chop. The overall feel is the wheels of the economy are starting to slow, but we’re all waiting for a catalyst or data-driven event to move the needle. We published our full Johnson and Johnson report – read it here – applying a 7% discount rate the upside of JNJ looks to be about +20% or so, with our valuation on the high end valuing the seperate businesses at $496B. We like this as a defensive buy in a market where there’s “slim pickings”.