Report from the frontline —

I am back from the trenches, boys and girls — the NZX ASM, as I’ve been harping on about since time immemorial. Nobody ever can accuse me of black and white thinking — the good, as we have noted before, is within the funds management business (approx. 11bn FUM) — one gentleman asked when the funds management business would be listed; mgmt demurred. The same gentlemen noted that a lot of funds managers are moving more to investing outside New Zealand. If you value the funds biz at 2% of FUM, that’s a value of $220mn or so, ascribing around $144mn of value to the rest of the co. We love the funds management business, but we think there needs to be a catalyst; either a partial listing or a partial or full sale of the segment. It’s all very well for myself and other analysts writing that the stock is worth north of $1.25; it is another thing for that value to actually be reflected — as Jerry Maguire said, show me the money!

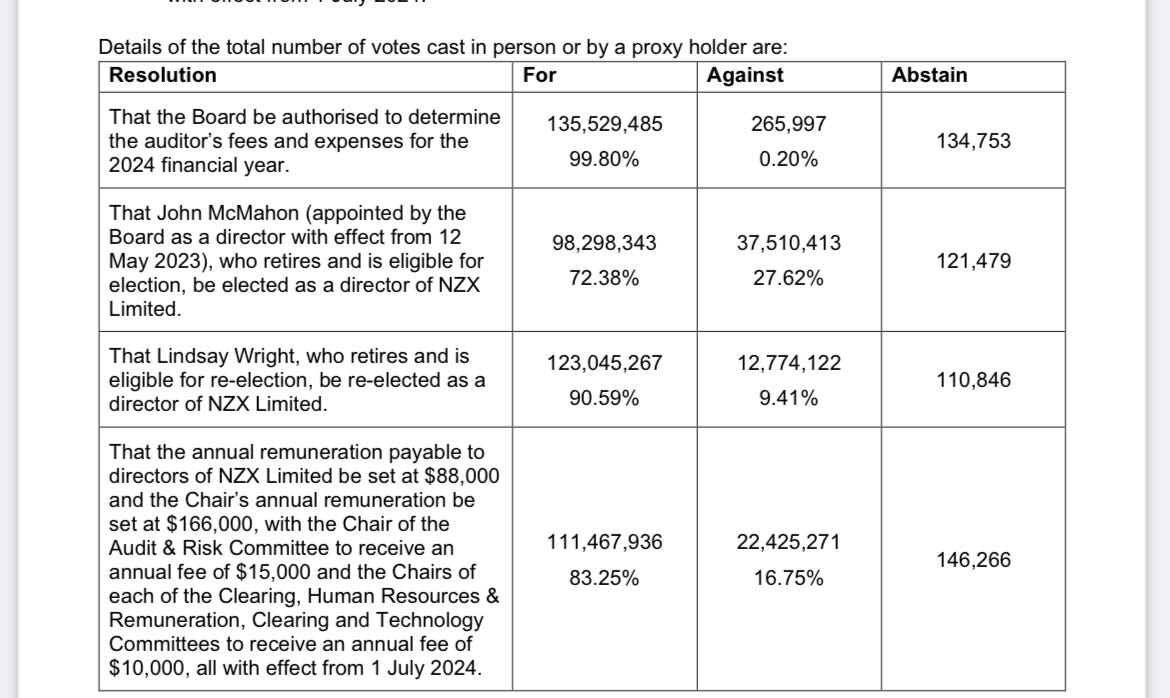

Now to the main event: resolution four.

I’ve been very vocal in my opposition to resolution four — resolution four attracted 16.75% of shareholders against the resolution. We don’t mind losing — we think the 16.75% represents a significant slice of shareholders who are clearly displeased with the egregious fee increase.

I note that this is a larger contingent against increasing remuneration than last year — last year’s only saw a 5.02% vote against. Despite the resolution passing, I think 16.75% of votes cast against the resolution casts quite a pall across it — directors will need to work especially hard to prove their mettle.

McMahon, in his capacity as chairman, highlighted that NZX has performed well when including dividends (the ASX has returned 34%, while the NZX has returned 49% , on a five year basis). This is true — however, the exchange has performed dismally exclusive of dividends — compare to the other exchanges below:

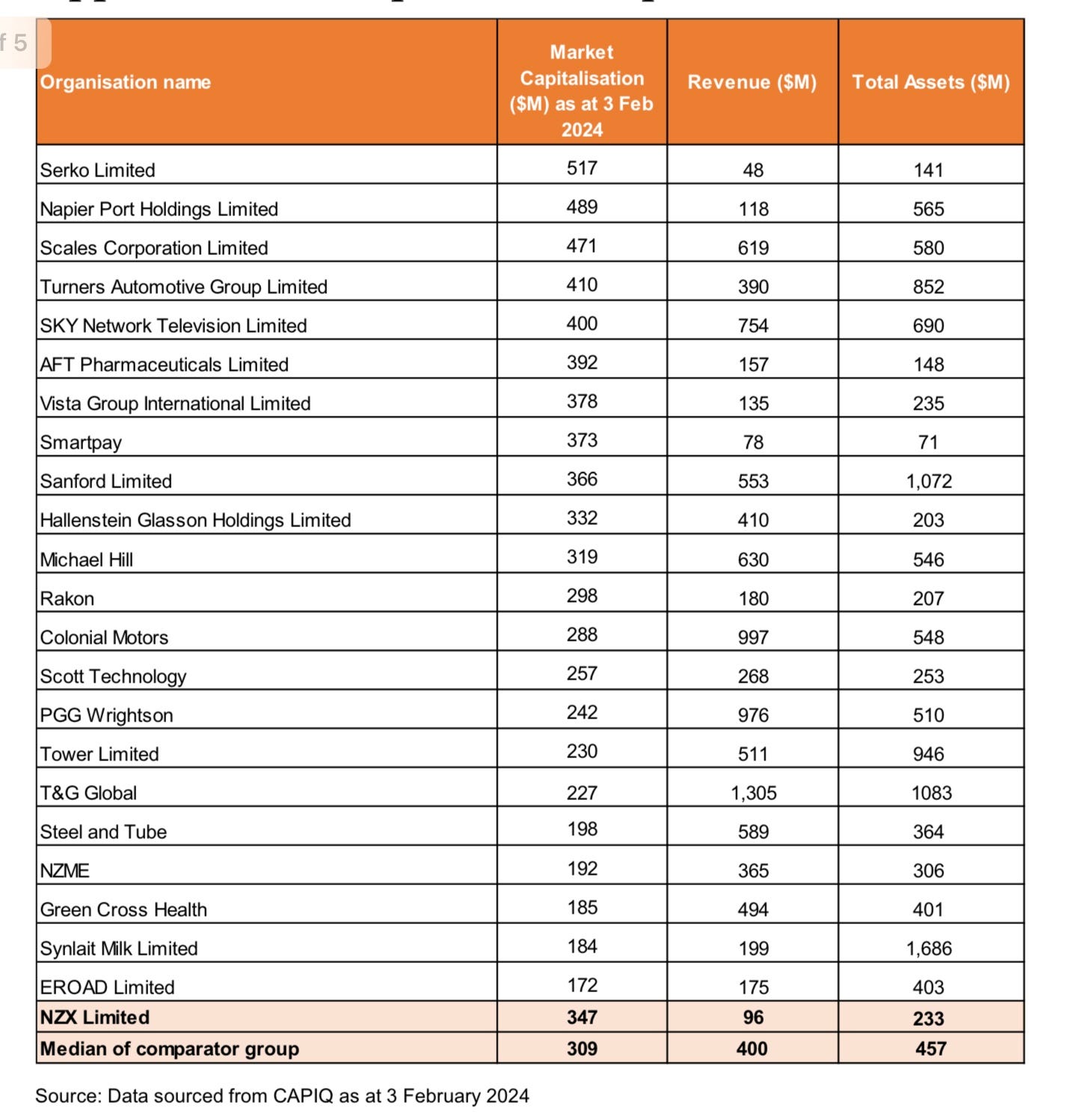

I said a better peer group to compare director’s pay to is the exchanges. PWC, who wrote the pay review report, used a hodge-podge of NZX mid-caps. McMahon rightly pointed out that NASDAQ is a different business (a superior one, in my opinion). But it’s kind of like — what else are you going to compare them to? Michael Hill?? I’m not joking — this is what PWC’s comparator report used:

I don’t know — this is a pretty whacky group to compare to. What does NZME do or EROAD do that has a resemblance to the NZX? Or Steel and Tube? I don’t know, you guys. A group of exchanges is not perfect data but it is better than Steel and Tube as a peer group.

Anyway — I think the way the vote skewed probably suggests growing shareholder discontent; I wasn’t the only one to speak up. One gentleman labeled the return (exclusive of dividends) “pathetic”, while one said “so, basically, it’s wrong time to ask for a pay rise”.

Ask they did! And they received. Meanwhile, Sharesies just was announced as the new vendor for Fonterra’s “Trading Among Farmers” scheme, which facilitates the trading of shares between co-op member farmers1. NZX previous held this contract2. That’s a small dint for the NZX, but surprising that the exchange can’t retain a simple platform contract for trading amongst farmers (BTW, I am becoming quite bullish on Sharesies — the acquisition of Orchestra was a smart one — I think the NZX has a challenger in terms of an exchange-like platform in Sharesies).

Finally, the most important thing.

Catering. I hear reports they got it from Coupland’s. They were saving shareholder money — so bravo. There were some sad looking savouries and there was some pizza bread cut in half. No scones! 5/10 for the catering efforts — report straight from our quants.

Other stuff

Lynas — remember when I said I would rather defer to Twiggy Forrest and Gina Rinehart on the subject of lithium and rare earths? Well, glad I did and glad we maintained our position in Lynas, because the Queen of Australia added +$49mn to her position in Lynas — her stake is now +5.82%. We prefer to be aligned with billionaires and think that this a clear offense against China’s dominance in the space. Watching closely.

Speaking of China — Aussie government spending another +$30bn to lift defence spending. Obvious beneficiary of this — Droneshield ($1.12 today). A lot of this is from a perceived threat from China. Which reminds me of this —

But I mean, by all means — spend away!

Oops, Princeton bet on Private Equity — link.

The endowment lost 1.7% last year, the worst return from the Ivy Leagues so far — the culprit is too much of a weighting towards private equity — 30% in theory, but 39% in practice. Private equity can drive returns in good times but the clue is in the name — private — if you can’t cash out or if things revalue to the downside the returns look less good. Putting private equity into an endowment comes from the late David Swensen — he created the so-called Yale Endowment Model, which advocates a mix of private equity, debt funds, absolute return equities and real estate. It works in moderation — the PE allocation is around 20%. But perhaps a 39% allocation doesn’t work — too much of a good thing, it turns out, is not always wonderful.

https://businessdesk.co.nz/article/primary-sector/fonterra-partners-with-sharesies

https://www.fonterra.com/content/dam/fonterra-public-website/phase-2/new-zealand/pdfs-docs-infographics/pdfs-and-documents/milk-prices/pdf-fsf-authorised-fund-contract.pdf