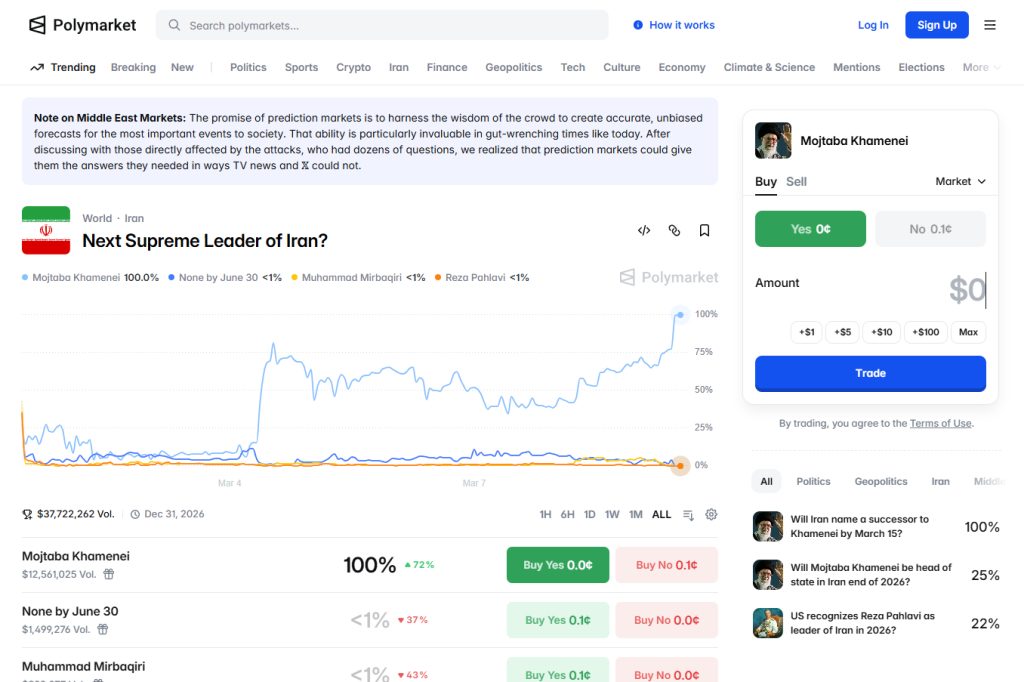

On February 28th, the United States and Israel launched coordinated strikes on Iran, killing Supreme Leader Khamenei, assassinating top military commanders, and hitting nuclear facilities across Tehran, Isfahan, and Qom.

The foreign policy establishment called it a shock.

On Polymarket, nobody was surprised. Traders had placed $529 million on the timing of a US strike on Iran, the largest geopolitical market the platform had ever hosted. The “February 28” contract paid out at 100 cents on the dollar.

Was it insider trading? Perhaps. But the crowd had priced a high probability of conflict for months while official commentators were still debating red lines and diplomatic offramps.

This keeps happening.

They only bet when they have an edge

The thing that makes prediction markets different from expert opinion isn’t just that bettors have money on the line. It’s that they have the option not to bet at all.

The economist at the major bank doesn’t have that luxury. They have a view because that’s their job. The incentive is to sound authoritative and stay close to consensus. Being wrong alone is a career risk. Being wrong with everyone else is just business as usual.

A prediction market participant only shows up when they believe they have an edge. Prediction markets aggregate the views of people who were willing to pay to express one. People with true skin in the game.

Your grandkids will own this stock

The same dynamic explains something in the equity data that the financial world has largely under-reacted to.

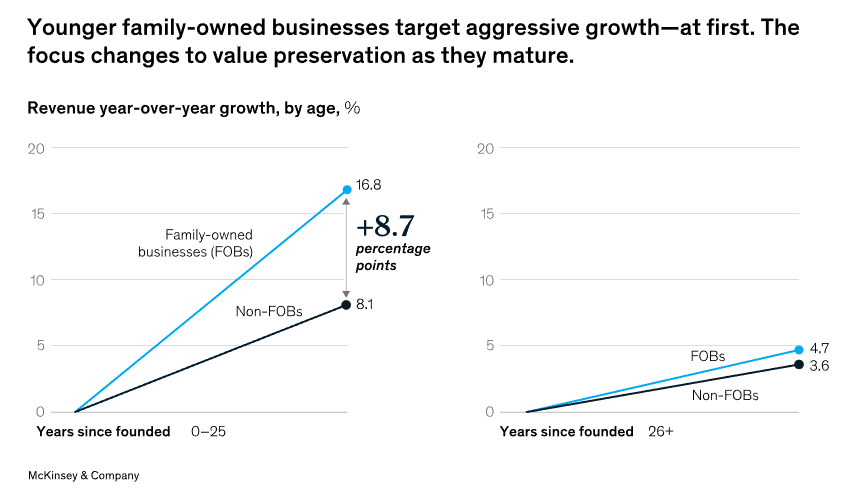

Credit Suisse tracked 1,000 globally listed companies where founders or family members hold more than 20% equity. Since 2006, these companies have generated 300 basis points of sector-adjusted excess return, every year.

A hired CEO is thinking about their next performance review. A founding family is thinking about what they hand to their children.

The family/founder led businesses often display superior top line growth. Despite their growth attributes, they have typically been more conservatively financed, reflected in lower financial leverage.

When you can’t sell and walk away, you tend to make less mistakes. No ‘transformative’ acquisitions that look great in a press release and catastrophic three years later. No over hiring to drive short-term growth.

They are patient. Because they answer to fewer stakeholders.

Consequence is the oldest alpha

Bettors and traders can be patient, sitting out until they have an edge. Then they take real risk. Institutional analysts and commentators don’t get that choice. They publish on schedule whether they’ve earned a view or not.

That same discipline is why family businesses have compounded well ahead of peers. Long-term decisions that they must own, with real risk. Avoiding short-term incentives driving dubious decisions by the hired CEO’s.

From the desk of IGB

Source post: Blackbull Research - Substack