I’ve got a bone to pick: this must be the least fun bull market in history. Markets are ripping and yet the whole thing feels strangely joyless. There’s no champagne-soaked euphoria, no dot-com-era mania, just a lot of cautious optimism. Hardly the stuff that gets you out of bed in the morning.

Yes, AI dominates the headlines, but there’s another force shaping this market: the relentless rise of passive capital. Sovereign wealth funds, pensions, and giant allocators are funneling extraordinary sums into passive vehicles that buy the index and its constituents with absolute indifference to fundamentals.

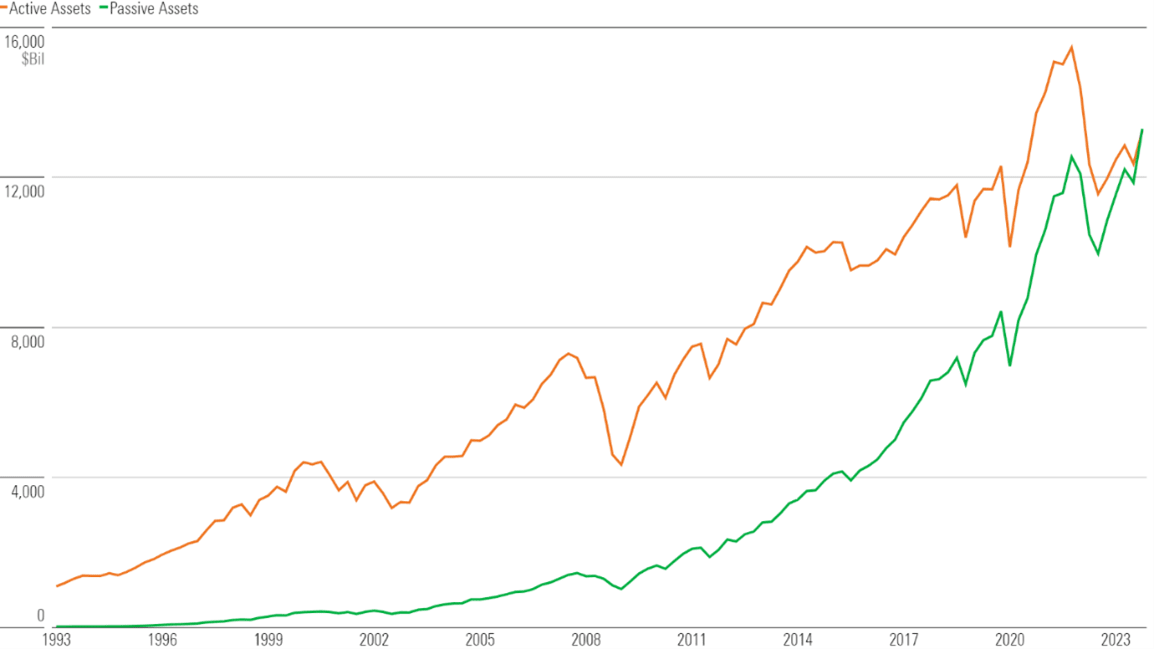

Passive investment funds now represent more than half of U.S. equity-fund assets, up from roughly 20% in 2005. And, with greater inflows than their active counterparts, this trend is expected to continue into the future.

Historical Fund Assets: Active vs. Passive

This creates a quiet structural bid under equities. A steady, rules-based drip-feed of capital that doesn’t read headlines, doesn’t panic, and doesn’t care about valuation.

Citi recently put out a note saying markets aren’t irrational, just more cautious than probably ever. UBS also recently held a conference and, unsurprisingly, the mood on the ground was jittery. Executives, strategists, and analysts all danced around the same theme: markets feel expensive, positioning feels crowded, and no one has been rewarded for taking the contrarian view. Among the most cautious, and the most burnt, are the institutional investors who have no choice but to participate in the exuberance. Every bull market climbs a wall of worry, and right now there are a lot of bears reluctantly squeezing into bull suits.

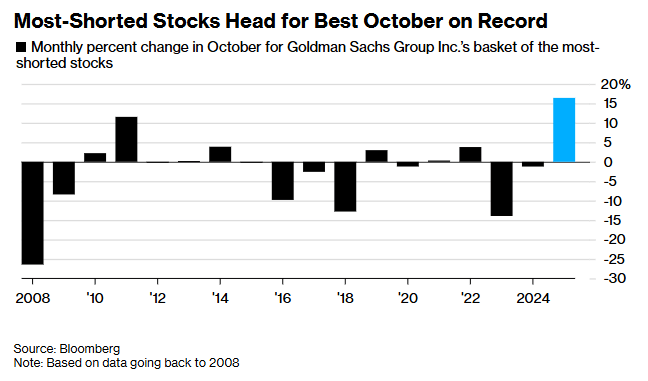

Which brings me to the most punished cohort of all: short sellers. GameStop set the tone back in 2021, a generational squeeze that turned hedge-fund shorts into cannon fodder for retail. The pain hasn’t gone away. Goldman’s basket of the most-shorted stocks rallied 16% in October, trouncing the S&P 500. It feels like the right time to be short. After all, the S&P 500 has just logged one of its strongest multi-quarter runs since the 1950s. But, every dip keeps getting treated as a fresh chance to BTFD*.

Michael Burry (played by a cross-eyed Christian Bale in The Big Short), the patron saint of the permabear, made headlines recently shorting Nvidia and Palantir (roughly US$1.1 billion in put-option notional across the two). Shortly after, he made headlines again… by shutting his fund. His parting message to investors: “My estimation of value in securities is not now, and has not been for some time, in sync with the Markets.”

Investors are searching for downside protection, but timing remains impossibly difficult. This market has displayed an extraordinary capacity to absorb bad news, recalibrate expectations, and continue rising. It may well continue to do so until something meaningful forces a repricing. But, identifying that catalyst remains the hardest part.

If there is one observation worth emphasising, it’s that bull markets are remarkably resilient. And the real F-word right now isn’t the one that rhymes with “duck”. It’s Fundamentals. No one is getting paid for pointing out that valuations are stretched. Instead, we’re all stuck in a slow-motion game of chicken (or Russian roulette), waiting to see what finally pulls the trigger.

Risk appetite, for now, appears robust. So, whether investors are buying every dip, shorting in frustration, or attempting the improbable task of doing both, the message is the same: this is a bull market that many do not believe in, but few can afford to sit out. And, for all the discomfort, the most dangerous position remains being left behind.

It is, after all, still a trader’s market – and someone, somewhere, should be enjoying it.

From the desk of IGB

Source post: Blackbull Research - Substack