Breaking — Paramount/Shari selling to David Ellison/Skydance — $1.75bn, per the WSJ. But also — no deal has been set in stone yet — it ain’t over ‘til it’s over…

I would love to tell you the deal is done — but this is Shari — we’ll see…

If you are a common stock holder of ‘peasant’ stock (i.e. Class B) then the situation still is unclear — had previously been mooted that Ellison would buy back some of that stock, in a concession to common stockholders. The person I will be watching the most here is Mario Gabelli — he owns the most common stock — and any deal that doesn’t give him upside will likely face a lot of scrutiny and potential torpedoing…I suspect any deal with Ellison will include clauses which preclude Shari and her advisers from being sued in the case of a shareholder lawsuit. For class A holders (also Gabelli, with the lion’s share going to Shari) it means a transaction price of ~$20 per share.

Breaking in France —

Looks like the leftie NFP leading, with 180 seats vs Le Pen’s 143. But look at the composition of all the seats — it’s a deadlock. Quoting from ye old Guardian:

“Deadlock” is the most likely outcome of the elections, with no “quick solution” likely in the coming days, according to economist and international law professor Armin Steinbach of HEC Paris business school. He says:

France has no political culture of making coalitions and compromises, like Germany or Italy. That is why it feels like a crisis for the French.

Mon dieu — USD appreciated a little against EUR in response but hard to know what will happen from here…French equities continue to be appealing… (I also note that both RNZ and the Herald had no news re the French elections on its website — and you wonder why we are a provincial country at the bottom of the world..!)

I tend to take the view that nothing will happen and it will be business as usual. I don’t know — maybe Bernard Arnault should just rule France like a modern day Napoleon.

NZ

WasteCo — Noting the departure of co-founder Carl Storm … stock is trading really down and dirty …about half of px when it listed. I took a small speccy position in my PA. Back in the day I used to love Republic Services, so… (not fin advice…)

SML/ATM — A2 still playing coy on which way it will vote (19.8% shareholder in Synlait)… oh dear…

RAK, ARV — Still a buyer.

Are we there yet?

From the depths of the consumer products industry —

General Mills, known for Cheerios and other breakfast cereals, is spending 20 per cent more on coupons in its new fiscal year, while “there are some price points we have to sharpen,” Jeff Harmening, chief executive, told analysts last month. Mondelez, the maker of Ritz crackers and Toblerone chocolate, is going to have a “challenging” year in the US, particularly with lower-income consumers, Luca Zaramella, chief financial officer, told an industry conference last month. As store-brand competition threatens its Chips Ahoy cookie brand, Mondelez is reducing prices back below $4 for certain larger sizes, Zaramella said.

And from Nike’s earnings call —

This quarter, we saw softer traffic in our factory stores, highlighting increasing pressure being felt by the value consumer

The consumer is weak! We knew this already, but during these last few years — which I think will be referred to a stagflation — like the 70s —when we look back at it, most consumer companies simply hiked prices to maintain margin. Eventually, you know, you are going to squeeze the consumer too far and they’re going to spit it back at you — this is what’s happened here.

The traditional business model in capitalism is i) make a good product ii) sell the product for less than it costs to make, market, and so on iii) allocate the excess capital to either reinvesting, dividends or share buybacks. If you repeat the model over and over you will probably have a good company. But this isn’t quite right — the real model with consumer products is i) make a product ii) use monopolistic practices to ensure your product is the main on on supermarket shelves, or have stores everywhere (Starbucks) or what-have-you iii) throw a lot of money behind the marketing for it, so people have a Palovian response to the product and iv), sell the product. There is a flaw here — often steps 2 and 3 cost a lot, so by the time you go to get the money for the product you are running at a loss — especially if you are operating in stagflationary times. The solution is, of course, simply hike the price! This works until it doesn’t, because at some point the consumer goes — nah, that’s enough. I have the sense many companies have been trying their luck these past few years — and have perhaps been surprised how much they could squeeze the consumer — the consumer got squouze!

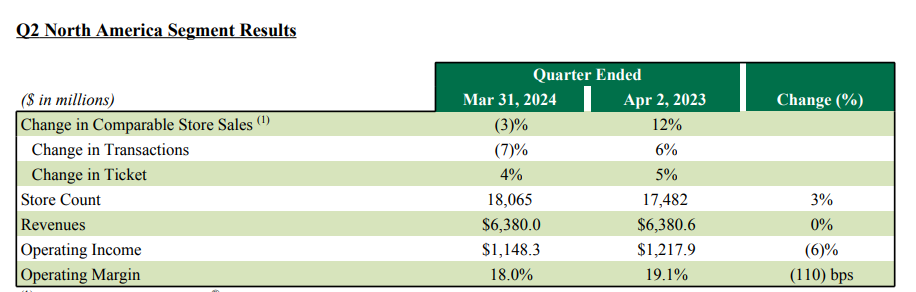

The best example of this — of consumer squeezing — is Starbucks. Transactions — that measure of organic growth — actually declined 7% — the chain responded by increasing ticket price, on average, by 4%. Even so — that’s a -3% change, in total. Consider the alchemy performed in the comparable quarter — organic sales grew 6% but the chain still hiked prices by 5% (!) — 12% growth total, but if you hike prices every quarter, by time you get to the year after (ie. Q2 2024) you see a result like what we just discussed — almost exactly the same revenues, hilariously, but a 110bps decline in operating margin. Oops!

All of this is to say — perhaps we are getting to the end of the tightening cycle. Consumer running out of juice. Consumer got squoze.

The other thing that seems to be happening here is the squeezing, in general, of the middle class middle consumer brand. Nike, Lululemon and Starbucks are all in the toilet. The “Becky” portfolio is rekt, at the moment. People are either trading down or trading up (i.e. if you are rich, then you can still afford your Brunello and your Golden Goose and your Ferraris. If you are part of the struggling middle class, you maybe are trading down to Dollar General or generic “no name” supermarket brands. Those torchbearer middle class brands are losing out.

Things I’ve read recently

The Fake Texas Oilman – NY’er

“Glen plaid sport coat at an evening event. Gradient aviator glasses. Spray tan. White pocket square. White. Not a Palm Beacher.”

RJF jr. is cray cray – VF

“On Monday morning he’s giving a speech saying, ‘Do not believe any scientists [on vaccines],’” recalls a person with close ties to Riverkeeper. “And on Tuesday, ‘You’ve gotta believe the scientists when it comes to climate change or what we’re doing to the river.

More people are buying stupid giant yachts (I think of them as floating prisons) — Airmail

Though the Russia-Ukraine war has disqualified oligarchs from buying super-yachts (at least legitimately), the market for floating pleasure palaces for the Über-wealthy is booming

How a London fund with a thorny history in Russia won global influence

Reminds me of my favourite reclusive billionaires, the Chandler brothers, who traversed Russia and Japan looking for opportunity…

To combat the abuses and release the company’s value, the Chandlers backed a campaign by Ryan’s partner, UFG chairman Boris Fyodorov, to gain a seat on Gazprom’s board and oust Vyakhirev. A former Finance minister and one of Russia’s most prominent reformers, Fyodorov asserted that the company was plundering corporate assets for the benefit of third parties.

Their stance wasn’t without risk. Fyodorov’s Siberian husky was killed by a rare form of cyanide, and Ryan was repeatedly questioned by tax authorities, according to people close to the two financiers. These sources say both men believed they were the targets of a Gazprom-inspired campaign of terror. Neither Fyodorov nor Ryan would comment on the alleged intimidation. To calm his nerves, Richard took up golf in 1998 and began to make annual two-month trips to Florence to learn Italian.