TOP TRADE IDEAS – Oil and Gas

The Tide is Turning

Nations representing almost 60% of the world’s oil production gathered in Doha last week to discuss

freezing their output at January levels in an effort to stabilize prices. Unfortunately, the meeting ended

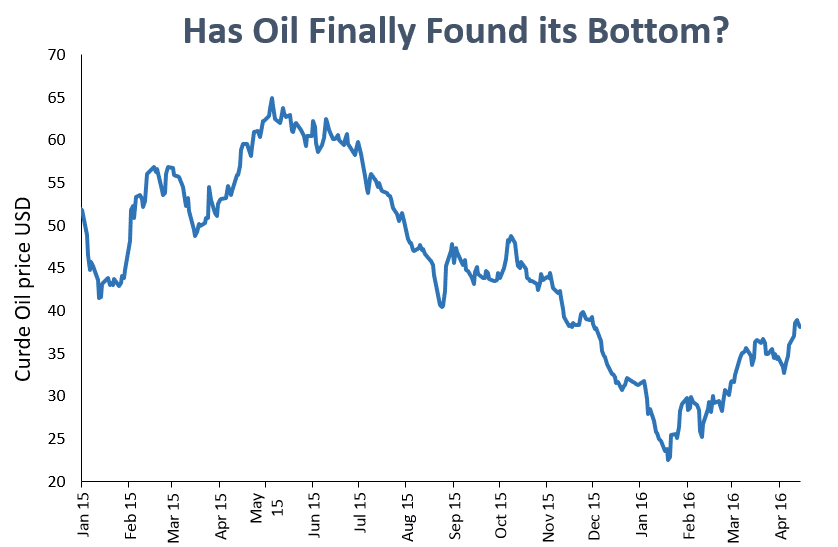

without any agreement on limiting supplies. However, somewhat surprisingly oil actually continued to rally despite the seemingly bad news. This is a very bullish sign for both markets and oil. The fact that bad news was unable to dent the current momentum suggest that there is underlying real demand. It appears investor sentiment has shifted somewhat to a more positive tone. Stark contracts to the period of turmoil at the start of the year. Oil has now bounced almost 40% from its January lows.

Accordingly, are of the opinion that oil may have found its low point. There are several indications that

the fundamentals for the commodity are continuing to improve.

US Shale Gas production continues to decline, easing current over supply issues. Further, the latest Chinese GDP numbers show encouraging signs for the Chinese economy. It indicated that the situation may stabilizing and that the loosening of monetary (lowering of interest rates) and fiscal policies that the

government implemented late in the first quarter is having a direct and material effect of the countries

growth. While the large boost may only be temporary at this stage (given that it is government policy driven, not consumer driven), it does provide a boost to sentiment and help to provide upward momentum for the economy.

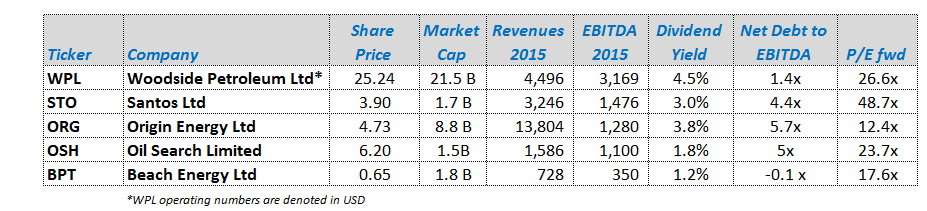

Given the change in the oil outlook and situation we have reviewed our top 5 large cap oil plays.

- Woodside Petroleum Limited – WPL.AX

- Santos Limited – STO.AX

- Origin Energy – ORG.AX

- Oil Search Limited- OSH.AX

- Beach Energy – BPT.AX

Oil Price Chart

Background and Statistics

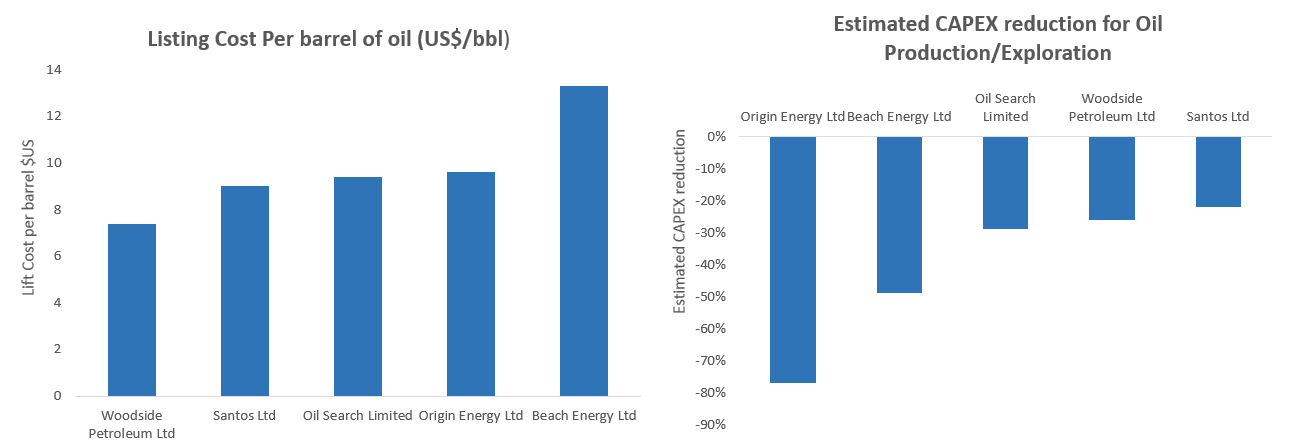

Lifting cost refers to the cost of producing oil and gas after drilling is complete. Lifting costs includes the

following: transportation costs; labour costs; repairs; depreciation etc.

Woodside Petroleum Limited – WPL.AX

Woodside Petroleum is an oil and gas company engaged in exploration, development

and production of hydrocarbons. Specifically, its major business function is producing

and selling.

- liquefied natural gas (LNG)

- pipeline natural gas

- liquefied petroleum gas

- crude oil

Presently the business is generating significant free cash flow from its mature oil

fields and LNG facilities.

However, the company has no material growth assets in the construction phase at

the moment and given its dividend policy of paying out the majority of its cash, it

appears that this may be the case for some time yet.

Given that the business has limited projects at present in its pipeline, it has moved to

paying out 80% of its underlying profits (NPAT).

At its most recent profit update, WPL beat the market expectations on its earnings,

although it was down material from 2014 (NPAT down 53% from 2014). Net debt was

also higher than the market anticipated as a result of weaker earnings.

We expect WPL to maintain its dividend policy of paying out approx. 80% of profits

(NPAT) over the near term.

believe that WPL is still well placed to acquisitions as the oil and gas industry

consolidates. Management have already expressed this desire when they attempted

to takeover Oil Search in Dec 2015. With a gearing ratio of below 20% we believe WPL

is in a reasonably strong position, especially compared with its peers, to take

advantage of motivated sellers.

Positives:

- Reasonably strong balance sheet

- Strong cash flow generation

- Good dividend payout to shareholders

- Oil price recovery

Negatives:

- Limited growth opportunities at present

- Weaker production

- Weaker LNG prices

- Earnings still falling, likely to recover in 2017

Santos Limited – STO.AX

Santos is a diversified oil and gas exploration and production company. Its principal

activity is the exploration for, and development, production, transportation and

marketing of, hydrocarbons. It specialises in

- Liquid natural gas

- Gas Liquids

- Crude Oil

It has an Asian portfolio, with a focus on three core countries: Indonesia, Vietnam and

Papua New Guinea.

It has interests in four liquid natural gas (LNG) projects, comprising GLNG, PNG LNG,

Darwin LNG and Bonaparte LNG.

It is a producer of natural gas, gas liquids and crude oil in eastern Australia and also operates in 3 core Asian countries (Indonesia, Vietnam and Papua New Guinea). It sells gas to domestic retailers and industry while gas liquids and crude oil are sold in the domestic and export markets.

Its key producing assets are:

- }Operated gas acreage and processing facilities in the Cooper Basin

- Domestic gas supplies in WA

- Minority interests in the Darwin and PNG

- Gladstone LNG project

Santos has successfully reduced its net debt to $6.2bn following a placement, equity

raising and asset sale following the slump in oil and gas prices.

We expect the company to begin generating positive free cash flow in 2016 assuming

oil prices can recover and maintain US$50/bbl.

Last periods financial results were rather bleak with the company reporting a loss of

A$2.7bn. This included impairments of $2.8bn. Underlying profit (NPAT) was $50m

and material below the markets expectations. The weak earnings are a direct consequence of the poor oil and gas prices during the period.

We expect STO to reduce its leverage further in 2016. This is likely to be achieved through divestments or additional equity. We believe it would be a negative sign to see the company cutting its capex further as it would have direct consequences on its production outlook and therefore its earnings and profits.

An oil price recovery would also take the pressure off STO to take further action to improve its credit metrics and prevent further asset sales or capital raisings. Although 2016 is likely to also be a difficult year for STO, we do see a recovery in revenues and earnings in 2017.

Santos is the most leveraged to a move in oil prices; a recovery in oil prices should

see the company outperforming its peers, in our view.

With oil prices remaining extremely volatile, investors have remained cautious on

Santos given its very high levels of debt. Santos should be considered a high risk play

Positives:

- Most levered to an oil price recovery

- New CEO – Kevin Gallagher

- Possible dividend cuts to maintain cash and pay down debt (we view this as a

- positive for the overall operations for the company as take pressure off the

- debt burden)

Negatives:

- S&P recently downgraded STO to BBB-/negative

- Flagged a further downgrade if coverage metrics remain stretched

- Debt levels remain a major concern

Origin Energy – ORG.AX

Origin Energy Limited (Origin) is engaged in the exploration and production of oil and

gas, electricity generation, and wholesale and retail sale of electricity and gas. ORG is

a vertically integrated energy company, via oil and gas production.

Origin’s major segments:

Energy Markets – an integrated provider of energy solutions to retail and wholesale

markets in Australia and in the Pacific.

Exploration and production – interests principally located in eastern and southern

Australia research and exploring oil and gas reserves.

Liquefied natural gas – segment contains its activities and transactions arising from its

operatorship of the Australia Pacific LNG upstream activities.

Origin’s most recent financial results were largely in line with market expectations.

One of the highlights was better than expected Energy Markets with higher volumes

and margins in natural gas in combination with stable electricity markets.

Origin is undertaking significant structural changes within its business to address it

large debt burden. At 5.7x debt to EBITDA (A$9.3B in net debt), Origin has one of the

highest leverage ratios and if not address while oil prices remain low, its credit rating

will come under further scrutiny.

In order to overcome this problem, it recently

- Raised A$2.5bn of equity via a rights issue – Sep 2015

- Selling down non-core asset – Sold Contact Energy for NZ$1.8 B in Aug 2015

- Has flagged up to A$800mn divestments including wind farms & other non-

- core infrastructure

- Signalled that if oil prices don’t recover it will cut its dividend

believe that management is taking the prudent steps now to help ensure the financial future of the company. Providing it doesn’t not reduce its capital expenditure and growth investment to far, ORG will be able to with stand the current slump in oil and energy prices.

If oil prices continue to recover through the course of 2016/2017 the earnings

outlook for Origin is likely to improve significantly, further reducing its debt burden. It

is also likely to result in a more efficient and lean business given the suite of capital preservation measures it has under taken.

Positives:

- Good diversification via its retail energy exposure

- Currently cutting CAPEX to preserve its balance sheet

- Cost cutting is improving the business efficacy

Negatives: - Still has a considerable debt burden that will prevent further growth

- Will be unable to acquire cheap assets given its funding and balance sheet constraints

Oil Search Limited- OSH.AX

Oil Search Limited is engaged in the exploration, development and production of oil

and gas fields. It is Papua New Guinea’s (PNG) largest exploration and production

company.

The Company’s main asset is its 29% interest in the PNG LNG Project, a liquefied natural gas (LNG) development operated by ExxonMobil PNG Limited.

Its segments include PNG oil and gas, PNG LNG Project, Middle East and North Africa (MENA) oil and gas, and Other.

In addition to the PNG LNG Project, the Company has interests in, and operates all of, PNG’s producing oil fields.

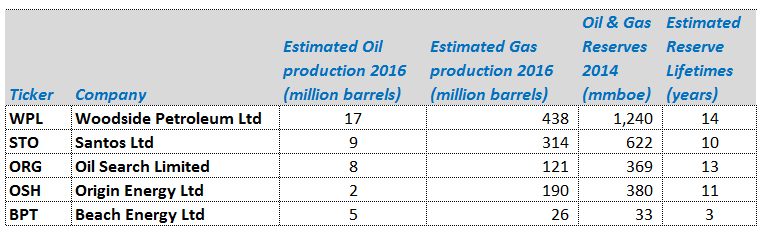

The Kutubu and Moran fields are key producers for the Company, contributing more

than 90% of the Company’s total oil production, as of December 31, 2014. The Company has drilled 59 wells.

OSH is now generating cash flow from its 29% stake in the 2- train PNG LNG project, which commenced operations in 2014.

Oil Search most recent financial reports were generally better than the market had anticipated. This was largely due to costs reductions. Underlying profits (NPAT) came in at US$360m but still down 25% compared with the previous period given current commodity prices. The decline in profit (NPAT) was driven by the 32% decline in gas/LNG prices. This is despite a 52% increase in production volumes and reflects the material fall in prices.

OSH remains committed to its aggressive growth timeline. At the current juncture OSH still has substantial flexibility in its capex programme going forward and the majority of its business expenditure is committed to exploration and appraisal rather than capital intensive and balance sheet constraining projects.

Despite the takeover bid from WPL last year, OSH is also looking to expand its businesses operations via bolt on acquisitions. However, given the relatively high levels of financial gearing (Net Debt to EBITDA 5x and Net debt: US$3.32B) would be apprehensive over any large or material purchases. At this stage in the cycle we would rather see further debt reductions than aggressive growth.

OSH has a prudent policy to pay out 35-50% of earnings, and this was maintained

and accordingly while its assets are high quality/strategic and low cost vs. peers, trading at a premium to its peers

Positives:

- High growth strategy

- Substantial flexibility in its capex programme

- Majority of expenditure is committed to exploration rather than capital

- intensive and balance sheet constraining projects.

- Prudent pay-out policy

Negatives:

- Debt remains at elevated levels

- Trades at a premium to its peers

Beach Energy – BPT.AX

Beach Energy Limited is an oil and gas exploration and production company, with

production operations in Australia in the Cooper Basin. Beach Energy (21% interest)

holds a JV with Santos Cooper Basin in which Santos is operators.

Beach is also very active in the Western Flank oil fairway in the Cooper Basin. Beach

has recently merged with fellow Cooper Basin player Drillsearch Energy. Together,

they now account for 100% interest in the key Bauer oil field. BPT and Drillsearch

have been very successful in exploiting the Western Flank oil play in the past and

should continue to do so over the medium term. While we expect BPT to begin

integrating and realising synergies from the transaction

Going forward, the Company seeks both domestic and international opportunities

while continuing its current exploration of gas domestically.

The future of the company largely relies upon the success of the Western Flank oil

successes and the merger with Drillsearch (DLS). Both BPT and DLS have been very

successful at exploiting the oil reserves in this region in the past, however, given the

reliance of the Western Flank acreage it does mean less asset diversification

compared with other companies.

Debt levels remain extremely low (A$78m representing 8% debt to equity) for the

company and therefore is the least likely to suffer from the financial stress of being

over levered in a low oil environment (providing management does not lever the

company up post the DLS merger).

Positives:

- We think Drillsearch was a logical and strategic target for Beach

- Greater synergies post-merger -Highly complementary acreage positions (in Western Flank oil, Western cooper wet gas)

- Low debt levels

Negatives:

- New CEO – greater strategic uncertainties post the Drillsearch merger

- Large exospore to the Western Flank- limited asset diversification