US Earnings

We’ll start the week with a quick summary of the big earnings coming out of the US. Long story short, tech reported “underwhelming” earnings which prompted a much needed sell-off. This was a classic Soros-style “reflexivity” trade – earlier in the week we saw a rally based upon the notion that i) The Fed would hike interest rates 25 bps and ii) the Fed might pause or pull make rates later in the year. The beaten-down “loss making companies” surged (CVNA, OPEN, etc) and acted like the tide that lifts all boats. Tech earnings acted as a much-needed antidote, with big players like Alphabet (GOOG) and Amazon (AMZN) falling anywhere from 400-1000 bps within the day. If anyone needed a reminder that the market is not rational, this was it.

Tech earnings were not that bad. AMZN increased revenues to +$145B and GOOG reported a mere 15c miss on EPS of $1.20, printing +$13B in operating earnings for the quarter in a year that’s seen advertising squeezed every-which-way-kingdom-come. Over at AMZN cloud revenue continued to grow +20% (+7.5% deceleration from last quarter). None of this is sign of the apocalypse; it’s a sign of normalisation. Apple (AAPL) reported a rare miss in iPhone revenue – sales fell +8.00% – while some of this is due to COVID-related factory issues in China, the larger issue is macro – as the consumer dollar continues to be pinched even further iPhone sales are hardly at the top of shopping lists. It’s almost important to take onboard that a lot of these earnings misses were due to Big Tech’s much-talked-about layoffs & their related impairments. Once you factor that in, tech’s earnings weren’t much of a boon for either bulls or bears: they demonstrated some resilience yet management across the board warned of worse to come.

Estee Lauder & The Skincare Cycle

It’s worth highlighting Estee Lauder’s (EL) latest earnings, because it offers a glimpse as to where we are in the cycle. Skincare sales fell +20% whilst makeup sales grew +3% (in constant currency). Skincare was a massive hero category during the pre-and-post COVID boom; now that glow has worn off and makeup, which has been declining for the best part of a decade, has shown signs of its ascendency. It’s not that far off from the “lipstick effect” of 1929 (lipstick sales grew in spite of the Great Depression). Does growing beauty product sales and declining skincare sales give us a clue to where we are in the cycle?

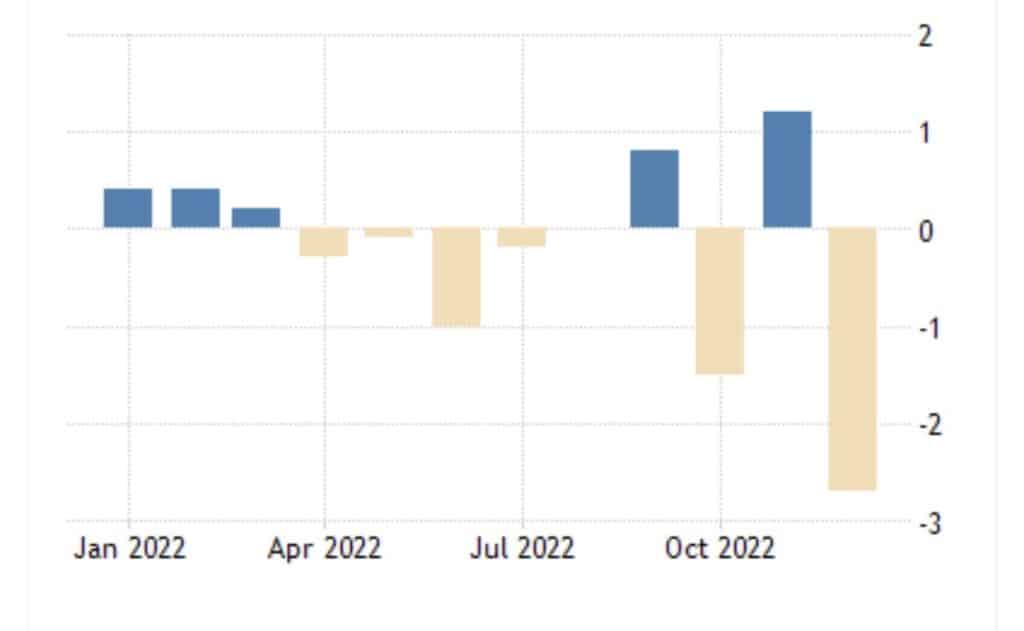

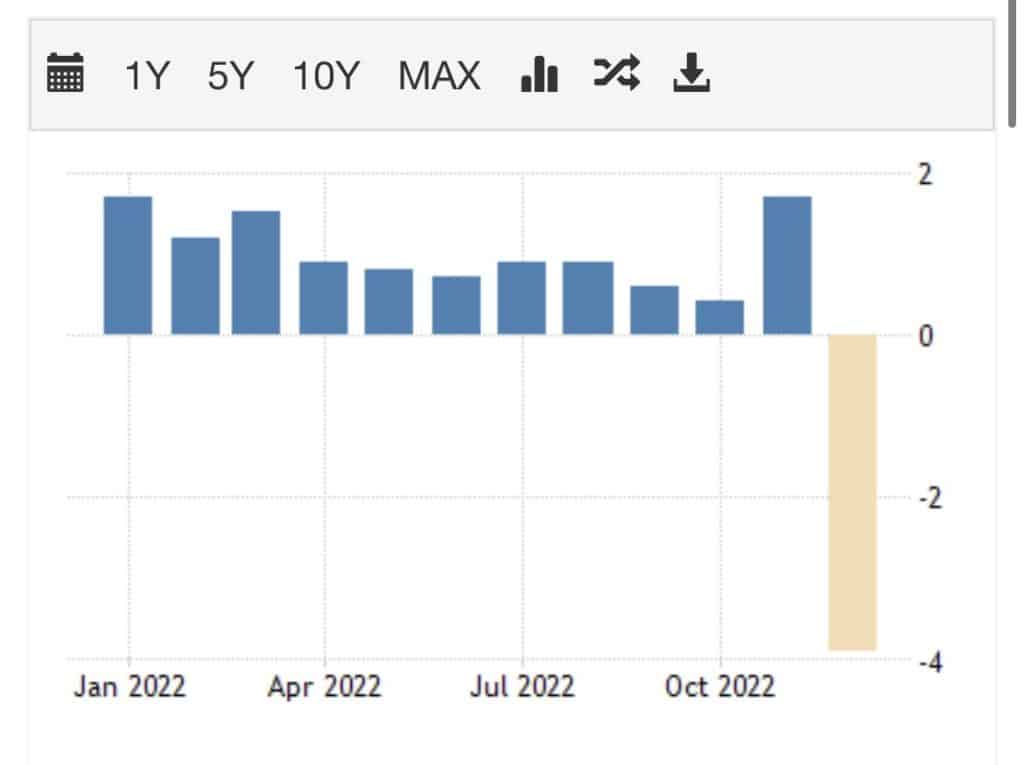

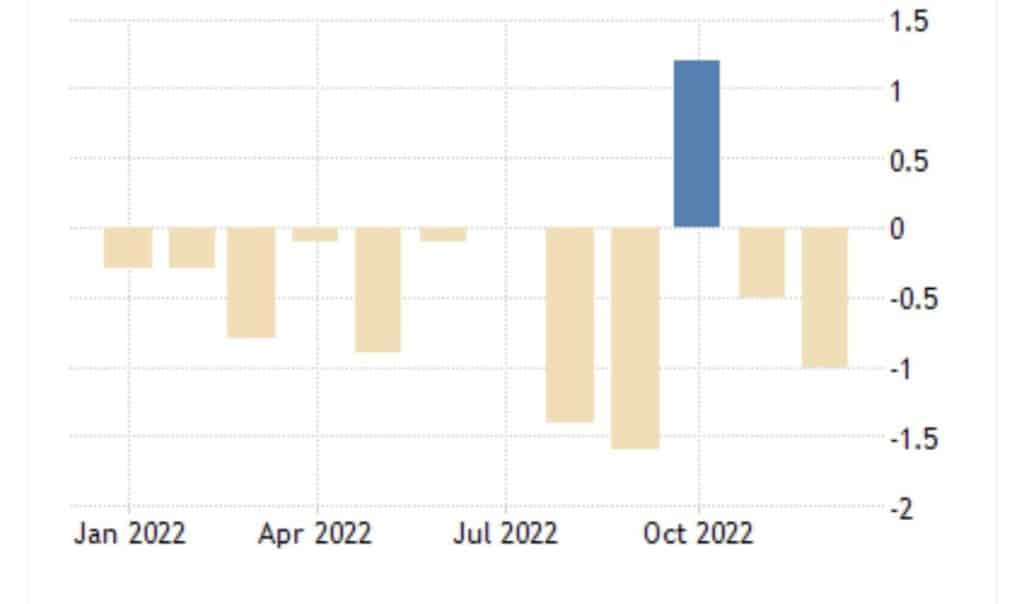

Europe starts to slow down; but is there a “big flip”

EU aggregate retail sales

Pretty weak data out of Europe, which matches what we’ve seen from the UK and Australia. See below.

Australian aggregate retail sales

UK aggregate retail sales

Like we keep saying – there is a dynamic of push/pull between very strong job data and slowing consumer spend. Slowing retail spend suggests that the consumer’s wallet is finally becoming drained, which has been the intent of central banks from the get-go. It suggests that rate hikes by the RBA and European Central Bank are starting to work, even if it’s contradicted by strong payrolls. This puts markets into a “neither here nor there zone” as they react – sometimes quite manically – to discrete pieces of data. One other possibility, which has been given credence by papers from both Goldman Sachs and JP Morgan, is the “big flip” – i.e. markets have absorbed all this data and the possibility of recession will continue to recede (Goldman Sachs cut their “recession chances” in the next twelve months from 35% to 25%). There’s some data to suggest that we might be in for chop without a lot of “landing” in the next twelve months: US home sales have actually increased (+2.3% for Jan), as have applications for loans. The primary impetus behind the “big flip” is the idea of entrenched labour – we’ve seen this a little with tech job cuts having little-to-no-effect on the wider economy. With entrenched labour, goods will inflect higher, which implies no cuts by the Fed in ‘23, a stronger US dollar, and stronger equities (with commodities selling off). It’s worth considering. Its opposition, of course, is that slowing consumer spending we can see in the charts above. It’s very much a “wait and see” moment.

The week ahead

All eyes are on US Jobless Claims on Thursday – if they continue to remain flat it’s a sign that the “entrenched employment” crowd’s thesis may have water. The under-activist-pressure Disney (DIS) reports earnings: we’re looking to Disney+ and Hulu streaming figures, as the company continues to endeavor to put its streaming business into the green. We’ll also get more of an idea of how the company intends on responding to Trian Partner’s Nelson Peltz – will new directors be appointed? Will more content be licensed to rivals, as rivals like David Zaslav at WarnerBrothersDiscovery have done? We recommend owning a ‘basket’ of media stocks, with preference given to Disney and less weighting given to WarnerBrothersDiscovery. We remain neutral on Netflix.

What Markets will be Watching this Week (UTC +13)

Tuesday

RBA interest Rate Decision

Wednesday

US Balance of Trade Data

UK House Price Inflation

Disney Earnings

Uber Earnings

Thursday

US Weekly Jobless Claims

Paypal Earnings

PepsiCo Earnings

Warner Music Group Earnings

Friday

AUS Monetary Policy Statement

Inflation Data from China

NZ PMI data