Top Dividend Picks in a Low Rate World

10 July 2020

We would like to provide this opportunity to identify our top dividend paying companies. Given central

banks both locally and around the globe have indicated interest rates are likely to remain at record lows for

some time, more and more investors are looking for income from equities. With interest rates at record

lows we think a benchmark for what could be considered an attractive dividend is around 4-6%. The

companies considered are relatively low risk, defensive companies, with healthy balance sheets able to

withstand the current economic uncertainty and generate relatively stable revenue and earnings.

Given the impacts of covid-19, some of the stocks have reduced their dividend payment for the next year

or two but we anticipate a very low probability for them to announce a further cut from here on out. Hence

being low risk and stable is another requirement for this list.

Our top dividend stock list is:

▪ Spark

▪ Telstra

▪ Genesis

▪ BHP Billiton

▪ Argosy Property

▪ Coca-Cola Amatil

▪ Kiwi Property Group

It is important to note that we have avoided some companies which may pay a higher dividend but there is less certainty and reliance on a sharp/or faster rebound in the economy, as well a solid growth companies which might have elevated valuations but now offer a low dividend yield.

Spark (SPK:NZX / SPK:ASX)

Spark remains one of our top income stock picks, largely due to its defensive nature as a utility provider. Its revenue and earnings underpinned by mobile, broadband and cloud security services which are likely to remain stable earnings though covid-19, as well as any economic slowdown. Its earnings in the recent past have been solid despite the headwind facing its fixed line business which has been offset by cost cutting and growth in mobile, as well as add value through its digital businesses.

Spark’s share price has gradually increased as interest rates drop due to the attractiveness of dividend, and it currently pays a 5.4% dividend yield – which is still attractive while offering some growth potential from its digital services.

KEY METRICS

Stability/Security

Share Price

$4.62

Growth

Price to Earnings Ratio

18x

Dividend Yield

5.4%

Risk

Last 12 Month Return

+16%

Market Cap

$8.5 Bn

Low

High

Telstra Corp (TLS:ASX / TLS:NZX)

Unlike Spark, Australian Telco provider Telstra’s shares have been hit hard as it struggled with the loss of its fixed line business and nBn rollout which has eroded its fixed line network business. We believe most of the negativity surrounded these headwinds is now priced in and the share price is now more fairly valued to represent it core (mobile) business.

Competition for mobile sector is likely to be more subdued given the TPG and Vodafone merger is going

ahead meaning there are three major competitors in the market as opposed to four. Telstra are a step

ahead with 5G investment compared to peers (which are encumbered with Huawei technology), which is

expected to provide the next leg of growth for the sector.

Also, given heavy capital investment in the past, Telstra’s capital expenditure guidance suggests there is

adequate cashflow and a robust balance sheet to sustain their current dividend, with the possibility of

growth once nbn headwinds have been taken into account. Telstra is now trading at a 4.7% dividend yield which is attractive in a very low interest rate environment (especially on the Australian market), and as other companies cut dividends.

The defensive nature of its core mobile earnings should support and help weather economic uncertainty, and provide growth opportunity from its extensive 5G rollout.

KEY METRICS

Stability/Security

Share Price

$3.52

Price to Earnings Ratio

19.5x

Growth

Dividend Yield

4.7%

Last 12 Month Return

-10%

Risk

Market Cap

$41.8 Bn

Low

High

Genesis (GNE:NZX)

The NZ power generator sector has been recently been hit after Rio Tinto and Sumitomo Chemical

Company – gave Meridian notice to terminate the Southland smelter’s power contract when it expires at

the end of August next year. The smelter uses almost 14% of NZ’s power generation, and the miner had

been reviewing the business for the past nine months to weigh up its viability as the cost of energy

squeezed margins amid weak aluminium prices. This will impact overall demand and pricing for electricity

in New Zealand.

We believe Genesis will be the least affected by the Tiwai Point decision. Being predominately a North

Island generator – it said the closure was an opportunity to accelerate electrification of industry and it

would reassess its generation portfolio.

We believe Genesis will take a relatively minor impact on earnings and dividend pay-out over the medium

term with the impact largely priced in. Taking this into account, the majority of GNE’s revenue and earnings

are still largely intact and defensive – especially amidst economic uncertainty in a slightly weaker ‘post-

covid economy”. Genesis should be able to comfortably support a healthy dividend yield of ~5.6%

(adjusting for the Tiwai point exit) which is still attractive at in our opinion, but also provides greater

income security with the trade-off being having the least amount of growth potential.

Stability/Security

KEY METRICS

Growth

Share Price

$2.88

Forward Price to Earnings Ratio

48x

Dividend Yield

5.6%

Risk

Last 12 Month Return

-19%

Market Cap

$2.96 Bn

Low

High

BHP Billiton (BHP:ASX)

BHP shares have recovered since the covid-19 sell off as China keeps ramping up activity and supply

disruptions in Brazil have seen demand and the price of iron ore rebound. The sector could continue to

perform well underpinned by continual demand from China, whilst BHP’s solid balance sheet can handle

near-term risks such as weak demand and commodity pricing shocks.

Given the diversified and crucial nature of their commodities and being an efficient low-cost operator, BHP should continue to deliver strong cash flow within this challenging environment. BHP is prone to some risk if the global economy slows down for a long period and commodity prices remain weak.

We believe earnings should remain relatively stable and BHP are fairly priced (representing stable demand

for and pricing for iron ore) to pay an reasonable dividend yield of 4.8% assuming no major shock to the

global economy, with some upside possible from a recovery in oil consumption and prices.

Stability/Security

KEY METRICS

Growth

Share Price (NZD)

$36.41

Forward Price to Earnings Ratio

13.2x

Risk

Dividend Yield

4.8%

Last 12 Month Return

-7%

Low

High

Market Cap

$184 Bn

Argosy Property Limited (ARG:NZX)

Argosy shares have pulled back due to covid-19 and the property company guided it anticipates to pay a

lower dividend for the 2021 financial year. Given most of its portfolio is largely consistent of industrial

property (45%) – with the sector set to perform well, and office (40%), with a lower exposure to retail. We

believe Argosy should be able to comfortable pay a reliable dividend over the medium with limited risk of

being cut further.

The recently guided (reduced) dividend of 6.35 cents per share is still attractive based on Argosy current

share price representing a 5.2% dividend yield, with potential to grow should the economy improve over

the medium-term and the completion of a major office development in Wellington by August 2021 increases

rental income and earnings over the medium-term.

KEY METRICS

Stability/Security

Share Price

$1.21

Forward Price to Earnings Ratio

15.5x

Growth

Dividend Yield

5.2%

Last 12 Month Return

-17%

Risk

Market Cap

$984m

Low

High

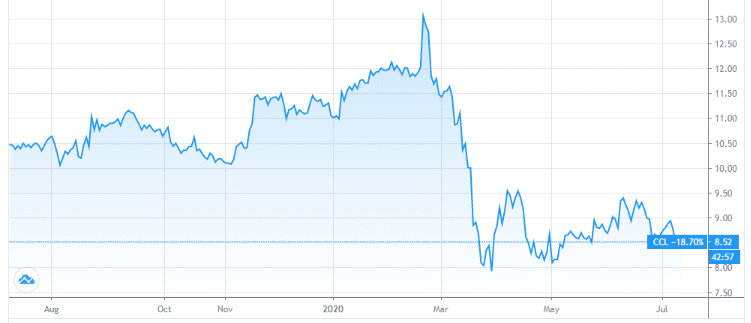

Coca-Cola Amatil (CCL:ASX)

Coca-Cola Amatil (CCL) shares have been hit heavily due to covid-19 and remain quite cheap (trading near record lows) after it delivered a weak trading update, as sales for high margin ‘on the go’ products were impacted due to lockdown, but early data suggests things have improved since then. With Melbourne in another 6-week lockdown, CCL shares slipped again with the state likely to experience a similar drop off in sales.

CCL is expected to have a challenging 2020 financial year with the market pricing that in. However taking a medium-term view, patient income investors would be able to benefit from a more attractive dividend yield of ~5% for the 2021 financial year. Given the nature of their products are consumer staple it should be relatively immune to a weaker economy, while being able to benefit from the recently completed cost out program. CCL also have a stable balance sheet to drive earnings and dividend growth if they were to acquire other beverages, expanding their portfolio, as done so recently to not only focus on just carbonated beverages.

KEY METRICS

Stability/Security

Share Price

$8.52

Forward Price to Earnings Ratio

18x

Growth

Dividend Yield

4.1%

Last 12 Month Return

-18%

Risk

Market Cap

$6.2 Bn

Low

High

Kiwi Property Group (KPG:NZX)

Kiwi property group shares were hit hard due to covid-19 and unlike Argosy did not rebound as well given its portfolio is more concentrated to retail and mixed used (which is predominantly retail), viewed as the higher risk property sector.

Accordingly, Kiwi property did realise a revaluation loss towards its property portfolio due to covid-19 and cancelled its final divided for the 2020 financial year. Post lockdown foot traffic has returned and its malls performed better than anticipated. Hence KPG announced it will recommence paying a dividend (sooner than anticipated) – while likely to be lower than the recent years to take into account rental abatement offered to tenants to support their businesses. KPG shares are now priced at an attractive yield, with strong growth potential from 2022 onwards (should the economy stage a moderate recovery) with the completion of near-term projects which could be quite attractive for patient income investors (dividend yield of 6-7%) combined with potential long-term upside from their Drury development.

Keep in mind KPG is the higher risk option on the list (but is still low risk with compared to other stocks in

the general market) due to economic uncertainty and the potential impact on the retail sector- but we

believe most of this is priced-in at the moment.

Stability/Security

KEY METRICS

Growth

Share Price

$1.03

Price to Earnings Ratio

17x

Risk

Dividend Yield

4.6%

Last 12 Month Return

-35%

Low

High

Market Cap

$1.61 Bn