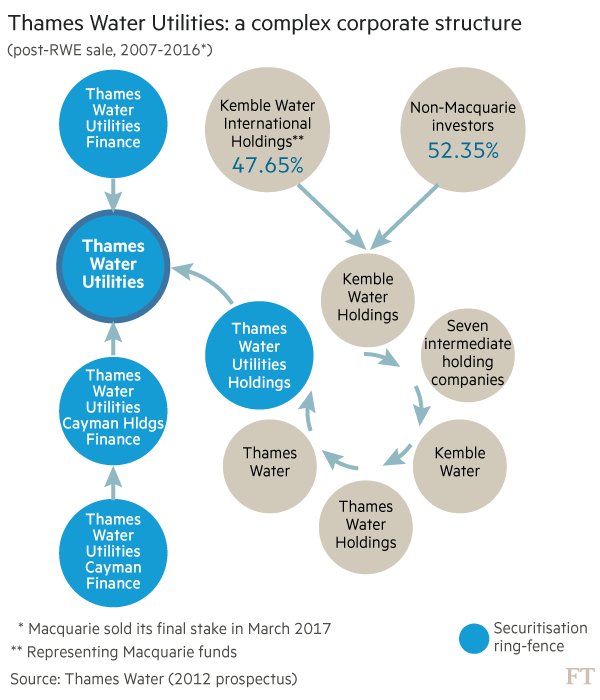

I think I’ve talked to you about Thames Water before — it is a case study for where closed-end private equity funds go wrong (particularly prevalent in infrastructure). Macquarie and other actors purchased a controlling stake in Thames Water and then promptly took out more cash than the company actually generated in dividends by taking out loans which were of course, attributable to Thames Water itself (not Macquarie — crucial point). The catch phrase you are looking for is “other people’s money” (the opiate of bankers everywhere). How do you set up a structure like that? You might ask. Maybe you’d do it like this:

Note that Macquarie got out while the going was good — from 2006 they paid out around 2.6bn quid of dividends (to uh, mostly Macquarie) and tripled debt to 11bn quid. Now Thames Water — after being milked dry — is a piece of crumbling infrastructure. It has 18.3bn in debt (in quid — my iPad keyboard doesn’t do the pound symbol, so please imagine it — sorry, Windsors). It is not owned by Macquarie now; now it is mostly owned by a bunch of pension funds (the biggest holder is the Ontario Municipal Employees Retirement System — might as well be the Retired Janitors of Idaho).

There’s a lot going on here: there are interest payments due, and there is not enough money because — and this may come as a shock — but it turns out when you issue debt to pay dividends you have to pay back the money at some point. I know — scandalous. Doesn’t the money printer, like, just go brr?

Thames Water is in a pickle. It’s erstwhile shareholders do not want to give it more money (in spite of the UK govt — the ineffective Tories — begging them to please help). Instead it is proposing to have its customers pay 56% more by 2030.

Ah, the customers. We forgot to talk about them. Thames Water is a utility provider — it provides water to London and the greater region. If you are the pension fund owners of Thames Water you probably don’t think much about the customers. They are merely a source of cash flows from which to leverage. This works until it doesn’t and eventually the whole house of cards collapses because water, unfortunately, needs plumbing and pipes and treatment plants and so on. It turns out infrastructure isn’t a magic money printing machine. Damn.

I think this points to a greater malaise within capitalism — asset manager capitalism has become a formula of i) buy an asset ii) leverage up, baby and iii) sell it on to the next asset manager and iv) rinse and repeat.

It’s not the first time this has happened. It happened here, in ‘clean’ ‘green’ NZ, when Fay Richewhite bought NZ Rail for a song from the govt and then did no maintenance on the network and then sold it back to govt after having made a small fortune in the process. I can’t believe I’m invoking Winston Peters here, but here’s an excellent speech he gave about 20 years ago (link) — what Faye Richewhite did was morally wrong. Sometimes Winnie makes a good point. Of course, National revised its “sell the silverware’ policy to a mixed ownership model, which injected the moribund NZX with companies about as exciting as a 90 year old falling asleep during bingo. But early Faye Richewhite is a model for how Macquarie and co have gone about stripping assets and then calling in the govt to clean up the resulting mess.

To my mind this is a perversion of actual capitalism, where capital is thrown at things to create something new (i.e. railroads, telecoms, the internet, PCs, etc…). It’s also, I think, indicative of the sitting “worm” that sits inside a lot of this asset manager capitalism1 — there is an end point, and it ends up costing society with no net benefit. Just look at Thames Water. There are a lot of catalysts which could lead to a market correction — this is one2. Other catalysts are obvious — i) the yield curve inversion ii) an overheated US market on a historical basis iii) higher interest rates, etc.

Fashun

Good piece here in the FT on the decline of selling luxury fashion online. There’s talk of the failure of Matches, Browns, Farfetch, etc. Net-a-Porter/Yoox is also on death row, but is supported through the magnanimity of its owner, Richemont.

What happened, Charlie Brown? Tl;dr is that direct retail wins. The margins are razor thin selling luxury as a third party. The market is fractured. There’s the flushing out of inventory — how do you boost sales after a bad quarter? Get rid of it quick on channels you don’t normally use. What ‘value add’ (vom) does a website selling the same stuff as everyone else have?

Richemont buying Yoox/NAP was a massive mistake — the “synergies” (ew, hate that word) between the owner of Cartier and selling online fashion are nil. The likely buyer for the asset is probably Bain Capital, who has a $4bn special situ fund for said purpose. I’m not saying rehab is impossible for the struggling online retailer — I’m just saying whoever buys it is still entering into a fractured market, with Ssense selling to the younger set and a bunch of other retailers (Cettire in Aus) selling the same stuff. Good luck.

On the other hand, Chinese ultra fast fashion retailer Shein just declared a $2bn net profit on the back of $45bn in sales. Those numbers are fairly astounding — former king of fast fashion ASOS posted about 3.8bn GBP in its best year (2022). Who is buying this polyester rubbish? (Clearly a lot of people). It turns out selling poorly made goods for $4 a dress makes money (so much for the turn against fast fashion a couple of years ago — people are greedy and hypocrites. How many anti-fast fashion people shop for $2 knock-offs from Temu?). It’s a good time to be a fast fashion retailer.

Briefly noted — good piece by Marissa Meltzer about Hermes’ head of leather goods. Link. We continue to love Hermes…noting the recent lawsuit in the US has no legs…Hermes SA’s get 0% commission to sell a Birkin — in effect, they have no financial incentive selling those bags to the wives of hedge fund managers and so on.

ASOS used to be big (‘you used to be cool man’) — at one point, yours truly was selling t-shirts on there to British hipsters in 2009. I made a lot of money doing that! The 00s were a more innocent time. I was even less cynical then.

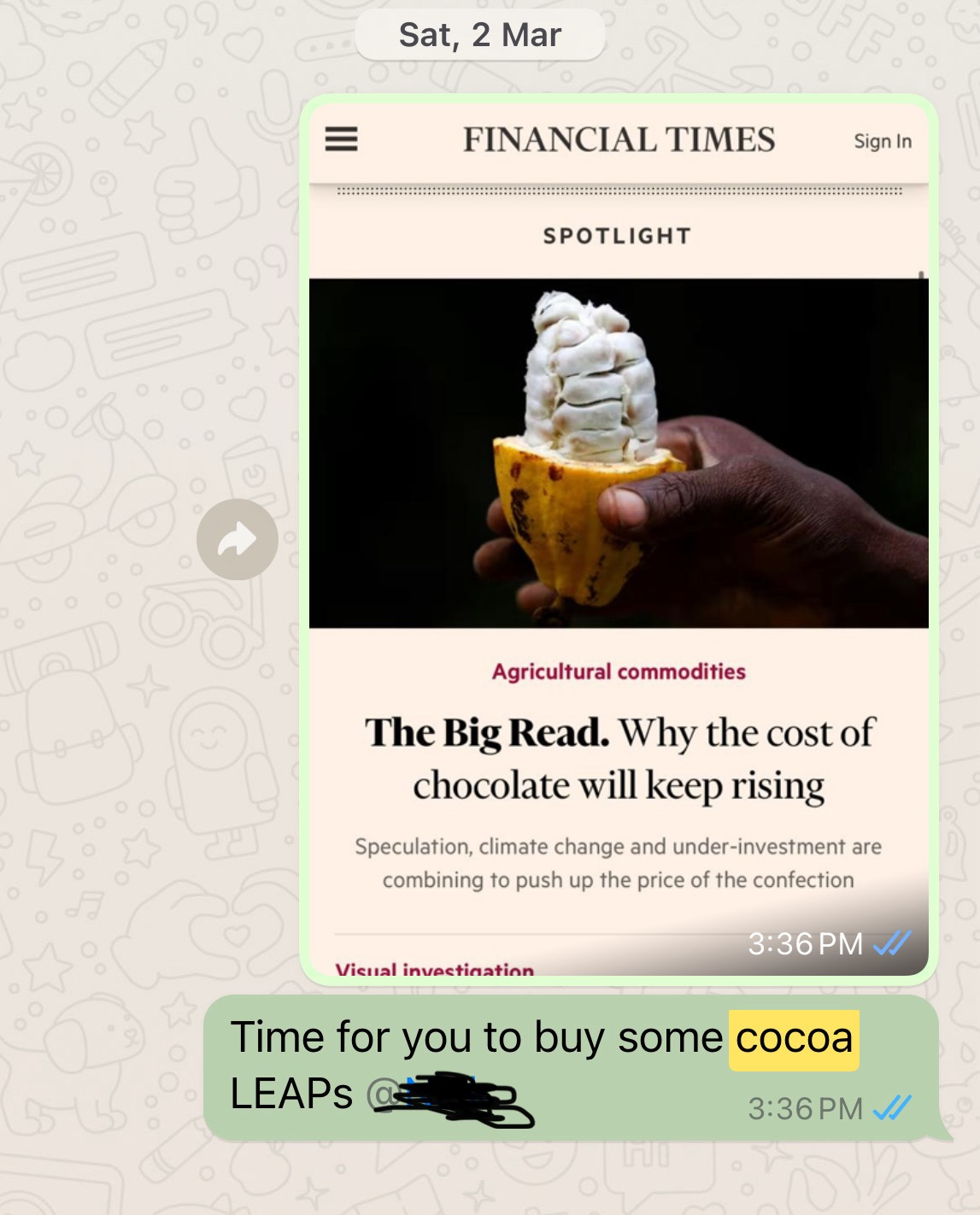

Cocoa-chella

Everyone is going crazy about cocoa, which makes me laugh — I jokingly posted that a friend should go long cocoa in a group chat, on March 2. Evidence —

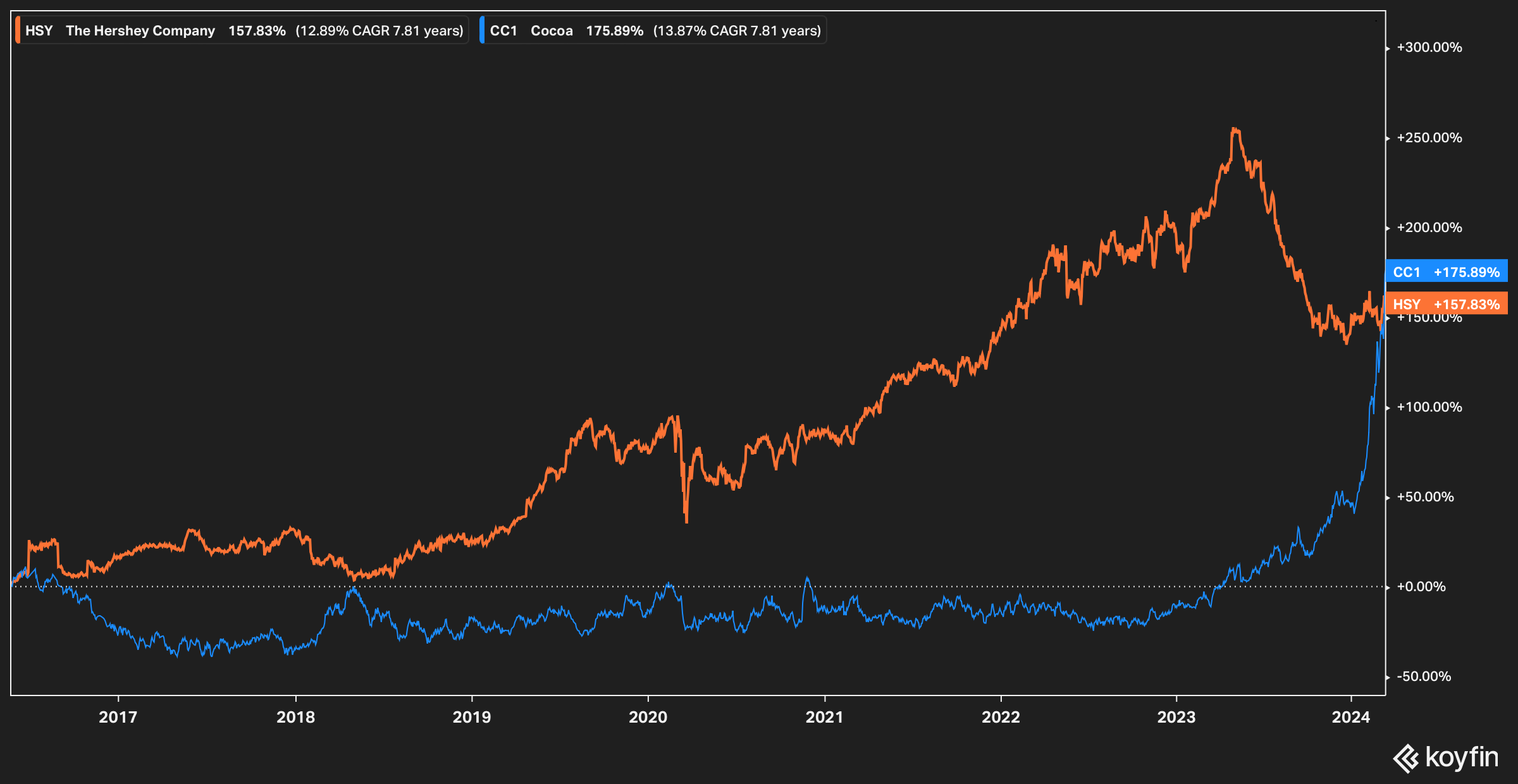

Well, I wish I did — that’s a 50% jump since then! (And exponentially more on a longer basis). It’s hard to imagine the price will continue to rise — it’s already more expensive than copper. I guess a fun trade might be: short cocoa, long chocolate companies (a company like Hershey has historically high ROIC — 22%). This is not investment advice. Hershey, by the way, is trading at the lower end of its 52 week range (the dude who writes The Bear Cave wrote perhaps one of the most unintentionally hilarious short cases this year when he proposed that readers should short Hershey on the basis that YouTuber-and-likely-Illuminati-member Mr. Beast has some kind of chocolate brand now and “the kids” will buy it. I cannot stand “Mr. Beast” and his hollow smile; it was a poor thesis). The other chocolate company, of course, is Lindt which only has a mere 12% ROIC. Like champagne producer Laurent Perrier it’s one of those stocks you keep in your personal portfolio for fun and not for gain. It’s fun to say you own. The chart has done nada, though. Boo hoo.

I’m borrowing the term “asset manager capitalism” from Brett Christophers, who wrote the very good “Our Lives in Their Portfolios”.

I can’t help but noting that NZ capitalism is uniquely without many benefits — most wealth creation in the country has come from the revaluation of property, the export of goods, or the associated tasks that come with either of those two things. Compare this to the US — iPhones, Singer Sewing machines, the Kodak empire…our record of innovation is slight. It doesn’t help that the capital markets don’t tend to support that: why bother, when you can just buy a gentailer?