Global markets recovered overnight (S&P 500 index +1.6%) after the worst week since November, as investors focussed on the hope for economic recovery.

Last week’s losses in equity benchmarks were widely attributed to deleveraging amongst hedge funds and other leveraged investors, some of which incurred large losses from the surge in GameStop and other unloved stocks. But there are signs that the deleveraging is already well advanced, with Bloomberg reporting that short interest in GameStop had been slashed, to 40-50% of the amount of stock on issue, compared to more than 100% in mid-January. Some investors may be nervous that the wild trading could trigger a systemic event or further selling, but we do not think this is a material risk for markets.

For the week ahead we think market attention is starting to refocus on other themes, including US fiscal stimulus, vaccine roll-out and corporate earnings. The mega-cap tech stocks, including Amazon and Alphabet rallied overnight and are due to report quarterly earnings on Tuesday – 113 S&P 500 companies reporting including: Amazon, Alphabet, Alibaba, PayPal, Pfizer, Merck, Exxon Mobil, Unilever, Royal Dutch, UPS, Siemens AG, Philip Morris, Glaxo, Gilead and BP PLC.

it was probably easy to lose sight of the positive vaccine developments that took place over the past week. Over the weekend, the UK announced a huge day of vaccinations with 598k done in one day, almost 1% of the population (1 in every 87 adults in one day). With nearly eight million people, or 11.7% of the population, having already gotten their first shot, Britain’s pace of vaccination is the fastest of any large nation in the world. Only Israel and the UAE are moving faster.

Z Energy (ZEL:NZX / ZEL:ASX)

As we touch on below, the NZ Climate Change Commission draft report has set out its recommendations on how NZ can meet its 2050 climate change obligations. It is of little surprise that the report promotes EVs and that banning fossil fuel light vehicle imports from as early as 2030 is the headline recommendation. This is a goal and there will likely be speedbumps along the way, and the value implications for Z Energy are limited due to the fact earnings implications are still several years away. In addition, the proposed mandating of biofuels should benefit Z Energy as it currently has NZ's only manufacturing plant.

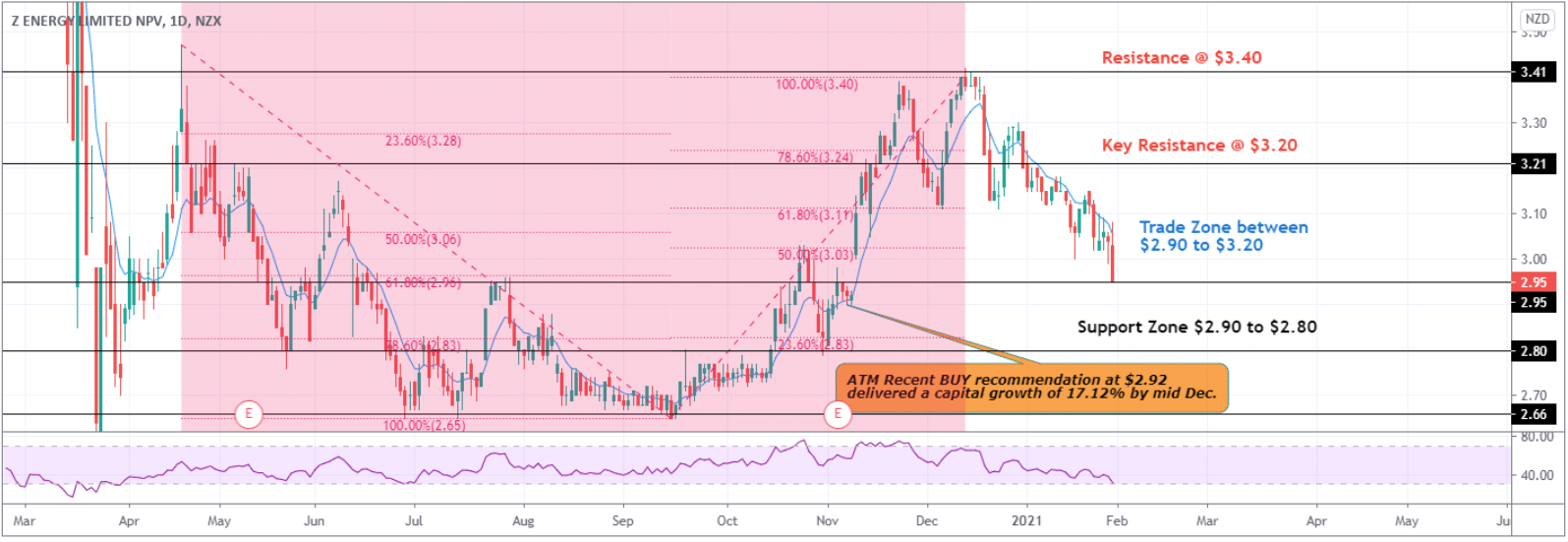

Looking more near term, ZEL's share price has come down to $2.95 given the increased risk of a possible lockdown in Auckland and closed borders between Aussie & NZ sighting risk of the UK strains of Coronavirus spreading in NZ. AIR and AIA stocks have also declined recently on the back of new COVID cases emerging in Auckland.

ZEL’s December volumes were ahead of expectations following a soft November 2020. The volumes were not enough to offset a decline in retail margins. November and December saw crude oil prices rise sharply, to NZ$78/barrel, with crude oil price movements impacting import margins. ZEL's Third Quarter 2021 retail volumes increased +2% and commercial diesel volumes increased +7%. It is to be noted that these categories are the most important for the profitability of ZEL. The other stand out feature of this quarter was the weekly store sales of +6%. These positive features were offset by very weak December MBIE importer margins but ZEL has indicated its retail margins have not fallen by the amount the MBIE margins imply. In the December month operating data update ZEL has reiterated its Financial year 2021 guidance range of NZ$235m to NZ$265m, indicating ZEL is confident that even if retail margins do not improve from current levels its 2021 result should still be within the guidance range.

We have a BUY (High-Risk) rating on ZEL.

Australia & New Zealand Market Movers

The Australian market was higher yesterday (ASX 200 index +0.8%) as the major miners found solid support. Fortescue Metals leapt +2.2% and Newcrest Mining jumped +2.1%, while BHP climbed +1.3% and Rio Tinto gained +0.9%. The financials sector was buoyed by a broker report highlighting the continued fall in loan deferrals.

In terms of stock news, Resmed released a solid result as it still appears to be taking market share in sleep apnea, helped by a strong portfolio of products. Coca-Cola European Partners received FIRB approval for its proposed acquisition of Coca-Cola Amatil, although shareholders continue to push for an increase to the current offer price of $12.75/share.

The New Zealand market fell on Monday (NZX 50 index -0.2%) but turnover was light as a third of the country was off work for Auckland Anniversary Day.

In stock news, Restaurant Brands noted 2020 underlying revenue growth of +2.1% (ex-California acquisition) despite COVID restrictions in all three core markets, with Australia and Hawaii offsetting softer sales in NZ. EROAD reported a soft 3rd quarter update, with negative US additions constraining growth.

The Climate Change Commission released draft report setting out its recommendations on how NZ can meet its 2050 climate change obligations. While still only a draft this would also need the Government to implement policy around it does highlight one theme which will remain in focus especially under current Labour Government:

The winner is the electricity sector with the report highlighting the central role of electricity in decarbonising the economy. The move to replace thermal fuel in the home is an additional boost to electricity demand.

The loser is the oil & gas sector. Whilst this is no surprise, the recommendation to ban fossil fuelled light vehicle imports in the early 2030s will have a modest negative impact on our view of ZEL long-term value. The short and medium-term implications to 2030 are relatively small.

3 Things Markets will be Watching this Week

- It is the second biggest week of earnings with 113 S&P 500 companies reporting including: Amazon, Alphabet, Alibaba, PayPal, Pfizer, Merck, Exxon Mobil, Unilever, Royal Dutch, UPS, Siemens AG, Philip Morris, Glaxo, Gilead and BP PLC.

- The RBA makes a Cash rate decision on Tuesday

- US employment (Nonfarm payrolls) data is released at the end of the week.

Team