Global markets were higher on Friday (S&P 500 index +0.7%) with US markets at fresh highs and the dollar weakened to a 2-year low as the Federal Reserve’s new inflation approach was digested by global markets.

Local reporting season across Australasia has now wrapped up, and as usual we will provide full updates for stocks under our research coverage in our weekly report.

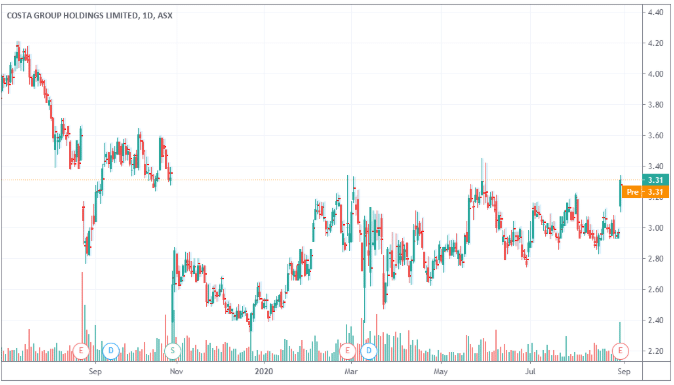

Costa Group (CGC:ASX)

Shares in Costa Group (CGC) jumped +12% on Friday as the fresh fruit & vegetables producer released its 1st half results. Costa reported 1st half operating earnings of $94m, up 14%. International rose 98%, while Australian Produce fell 41%. The numbers were a touch below market consensus.

However, the outlook is positive given better pricing and growing conditions domestically and CGC said a number of weather/operational factors called out by the company that won’t impact operations in the 2nd half. Post the drought conditions, pricing is now much stronger, while recent capital spend is coming on stream and some transitory headwinds will also pass.

We continue to believe CGC is cheap & appears to be through the worst of things – and as such we remain BUY rated.

Australia & New Zealand Market Movers

The Australian market slipped on Friday (ASX 200 Index -0.9%) as tech, telco and mining stocks continued to lead the falls.

In stock news, data centre operator Next DC continue to climb higher after delivering a solid result for the 2020 financial year which came in at the top end of guidance. Revenue for the year came in at $205.2m, and underlying operating earnings (EBITDA) of $104.6m, both up +24% and 23% respectively, driven by strong demand for capacity at its data centres.

Shares in building products & construction company Boral were 2% higher as it reported a $1.14 billion loss for the past financial year, which was not as bad as the market expected. The company took a $1.3 billion impairment charge, mostly against the value of its North American business. Boral was also hit by lower sales and production volumes in the second half of the year, as the pandemic hurt demand and stock availability.

Meanwhile, shares in Harvey Norman were -1.6% lower, reversing early gains, after the retailer reported a 19% rise in net profit. Full-year profit came in at $480.5 million, up from $402.3 million the previous year, as sales across the group rose by 7.6%. The retailer said there had been a strong start to the current financial year, with comparable sales across its Australian franchises up 38% so far, compared to the same period last year.

The New Zealand market added to gains on Friday (NZX50 Index +0.3%) even as a string of cyber-attacks left the local market open for just five hours in the past two sessions. NZX Ltd dropped -3% after a week of cyber-attacks rocked investor confidence in the company,

A2 Milk fell -4%, posting the biggest loss of the day as investors reacted negatively to executives selling down their holdings. We would not read too much into the selloff.

Shares in Delegat Group jumped to all-time highs as it released another solid result and forecasts sales volumes over the next three years are forecast to grow at a ~5.5% per annum, with key drivers being the US market and the Pinot Gris variety.

Medicinal Cannabis company Cannasouth's operating loss widened in the six months to June 30 but the company said its result was in line with its business plan. Waikato-based Cannasouth said its loss came to $1.45m, up from $821,175 in the previous corresponding period. There were wild swings in the share price, which we see as pure speculation for a company which is not even generating revenue.

3 Things Markets Will be Watching this Week

- COVID-19 related news-flow remains key, with second wave and lockdown headlines, while US Congress debate what an extension of stimulus will look like.

- With reporting season all but over, focus in the week ahead returns to macro data including monthly employment figures (nonfarm payrolls) and ISM manufacturing data in the US

- The RBA also meets on Tuesday.