Happy New Year to our faithful readers, offered just within the statute of limitations for seasonal goodwill.

By now, most of you will have made your way back to the office. While we took a well-deserved break, the market, and certainly Donald J. Trump, did not. Here are a handful of stories to get you back up to speed in the new year.

Markets are facing an unusually crowded news cycle, cutting across geopolitics, U.S. policy, central banking, and fast-moving technological change. We’ll begin with geopolitics, starting in the U.S.

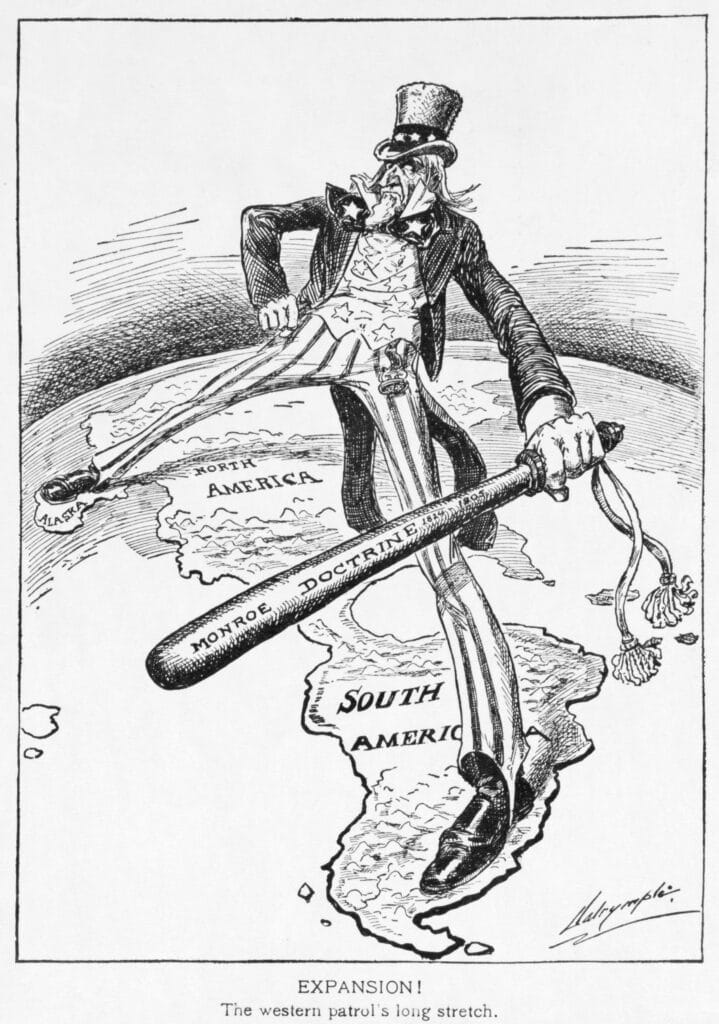

Trump has been invoking the so-called “Donroe Doctrine” – a renaming of the 1823 Monroe Doctrine. What was once a warning to outsiders is now framed as America actively reclaiming its hemisphere. Some traditions, like creative licence, never die.

The result was a midnight visit from Uncle Sam to Venezuela’s president and his wife, achieving in 35 minutes what Putin has failed to accomplish in Ukraine over 35 months. Unlike George W. Bush, who dressed the invasion of Iraq in the language of weapons of mass destruction, Trump was disarmingly direct, mentioning “oil” more than 20 times in his Venezuela press conference, with a few dutiful nods to the alleged drug trade thrown in for balance.

I only recently learned that Venezuela has the largest oil deposits in the world. Sexy. What is not sexy, however, is the supply-demand dynamic of oil. We currently have more supply than demand, which is helping keep prices suppressed. Claudio Galimberti points out it would cost over $70 a barrel to extract oil that can only be sold for around $58 a barrel, due to the heavy crude nature of Venezuelan oil. So why do it? A flex of America’s military prowess?

As a NATO member, this is a far harder proposition. Rather than work the bureaucracy, Trump appears to have set it aside entirely. Opting instead to publicly circulate text messages from foreign governments.

Domestically, U.S. policy uncertainty is becoming more pronounced. The ongoing public targeting of Jerome Powell, the only Fed Chair in history to have markets genuinely feel sorry for him, has reopened questions around central bank independence. It also raises the very real issue of who might replace him as Chair of the Federal Reserve. This is unfolding alongside potential legal challenges, including a looming Supreme Court ruling on the legality of tariffs and a separate hearing on whether the firing of Fed Governor Lisa Cook would even be lawful. Together, these developments introduce legal and institutional risk into what is normally considered one of the market’s most stable and predictable pillars.

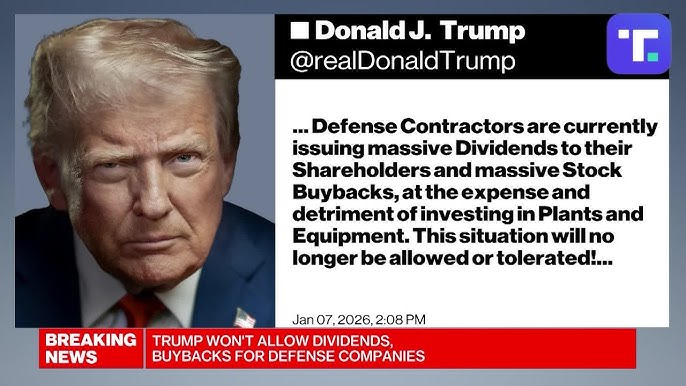

Further complicating the policy backdrop are proposals that blur the distinction between economic support and direct intervention. Caps on credit card interest rates are intended to relieve household pressure, but risk constraining credit availability at the margin. Separately, proposals for the U.S. government to purchase $200 billion of mortgage-backed securities, aimed at pushing mortgage rates lower, would represent a meaningful re-entry into housing market support. At the same time, efforts to limit dividends and executive pay at defence companies, alongside signalling materially higher U.S. military spending, send mixed messages on capital allocation incentives.

Technology remains a source of disruption, though it feels less overheated than it has over the past 18 months. The latest AI release from Anthropic has reignited debate around the long-term economics of software businesses. As AI capabilities accelerate, investors are questioning pricing power, margin durability, and the permanence of traditional software moats.

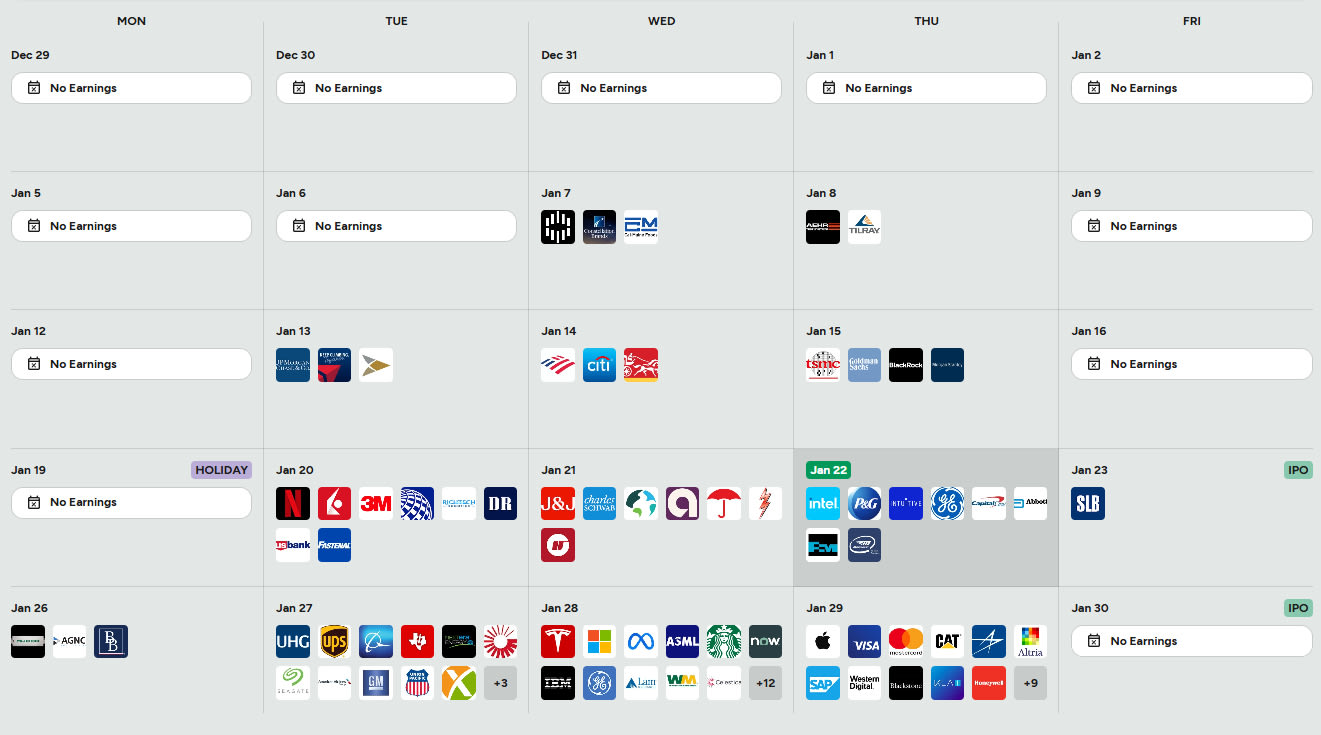

All of this is playing out against the steady drumbeat of quarterly earnings reports, which are offering valuable bottom-up insight into how companies are coping with higher rates, shifting demand, and rising costs. Earnings season typically provides an anchor for markets, but its stabilising influence is being challenged by the volume of macroeconomic noise.

Finally, attention is turning offshore. The Bank of Japan meets later this week against a fragile backdrop of rising JGB yields and pressure on the yen. Any hint of policy normalisation, or delay, risks spilling over into global bond and currency markets. With Japan now a meaningful buyer of U.S. Treasuries, domestic policy shifts may increasingly be reflected in U.S. rates.

This is a market driven by a collision of many narratives. The investor’s task remains unchanged: separate signal from noise, distinguish real shifts in risk from headline friction, and stay disciplined as markets tug in multiple directions. Familiar work; only with louder distractions.

Source post: Blackbull Research - Substack